How much do Australians spend on bills each month?

Australian households had an estimated average of $674 per month in essential bills in 2025, excluding mortgage repayments. For owner-occupiers with an average new mortgage, total monthly outgoings reached about $4,911.

12 min read 08 June 2026Updated 08 June 2026 Fact checked

Key figures, 2025

$674

per month on essential household bills, excluding mortgage. Up from $447 in 2015

$244

per month for home and contents insurance, the fastest-rising bill category over 10 years

$4,237

per month estimated repayment on the average new owner-occupier loan. Up from $2,416 in 2021

−4.4%

real wage growth in 2022 — the biggest annual fall in Australians' purchasing power on record

Section 01Monthly bills

Average household bills in Australia: what families pay each month

The average Australian household spent $674 a month on essential bills in 2025, covering electricity and gas, water, phone and internet, and home and contents insurance. That was 51% higher than in 2015, when the same bills cost $447 per month. For owner-occupiers with an average new mortgage, monthly repayments of about $4,237 lifted the combined monthly cost to about $4,911.

What Australians spend on bills each month

2025 national averages across five categories · 2015 and 2020 shown for context

Electricity and gas

$195

per month, 2025

+54% since 2015

2015

$127

2020

$138

2025

$195

Water

$110

per month, 2025

+57% since 2015

2015

$70

2020

$90

2025

$110

Phone and internet

$125

per month, 2025

−4% since 2015

2015

$130

2020

$125

2025

$125

Home and contents insurance

$244

per month, 2025

+103% since 2015

2015

$120

2020

$161

2025

$244

Total essential bills (excl. mortgage)

$674

per month, 2025 · up from $447 in 2015

2015 $447→2020 $514→2025 $674

Mortgage repayments owner-occupiers only

$4,237

per month, 2025

+90% since 2015

2015 $2,233→2021 $2,416→2025 $4,237

Source and methodology: Modelled national monthly averages based on ABS CPI sub-indices and cross-checked against AER, ABS Water Account, ACMA and Finity data. Mortgage repayments are calculated from ABS average new owner-occupier loan sizes, assuming a 30-year principal-and-interest loan at the RBA average standard variable owner-occupier rate.

What bills are included in the $674 monthly average?+

The $674 figure covers four categories: home and contents insurance ($244), electricity and gas ($195), phone and internet ($125), and water ($110). Mortgage repayments are excluded because they only apply to homeowners with a home loan. When estimated repayments of about $4,237 are added, the combined monthly total for mortgaged owner-occupiers reaches about $4,911.

Do these averages apply equally to renters and homeowners?+

Energy, water, and phone and internet averages apply broadly to both renters and homeowners. The home and contents insurance figure reflects what property owners pay; renters with contents-only policies typically pay less. Mortgage repayments apply only to homeowners with an active home loan. Renters' largest housing cost is rent, which is not included in these figures.

Section 02Electricity and gas bills

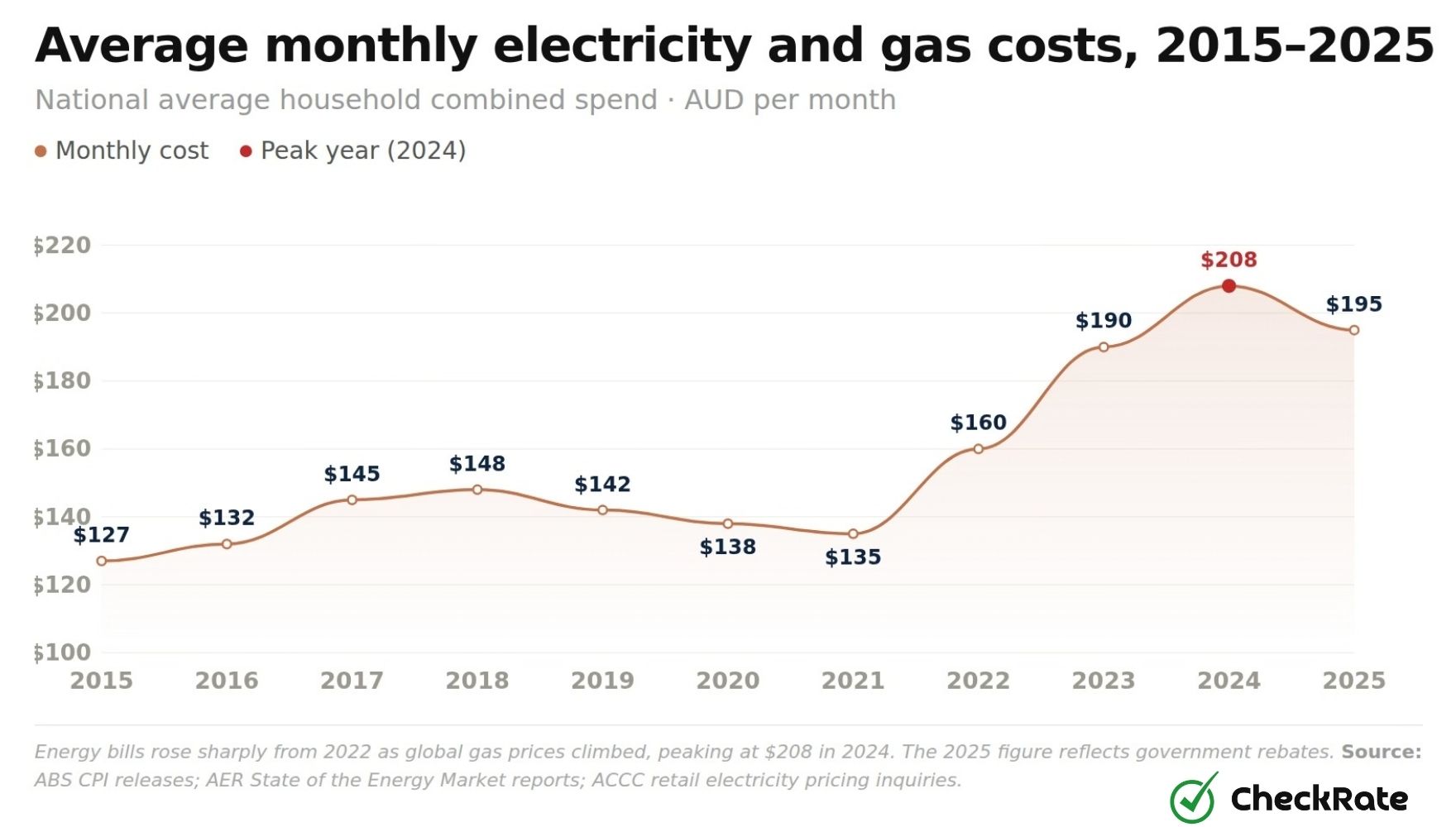

Average energy bills fell to $195 a month in 2025

The average Australian household spent $195 per month on electricity and gas in 2025, down from a peak of $208 in 2024. The reduction partly reflected Commonwealth and state energy rebates, which reduced reported household electricity costs for eligible households.

Electricity prices later rose as earlier rebate effects were unwound or used up. ABS data showed electricity prices rising by 25.4% in the year to March 2026, but this figure reflected the changing effect of rebates as well as underlying retail prices.

Average monthly electricity and gas costs, 2015–2025

National average household combined spend, AUD

Energy bills held relatively steady from 2019 to 2021, then rose from 2022 as global gas prices climbed. The 2024 and 2025 figures reflect government rebates that reduced what households paid.

Source: ABS CPI releases; AER State of the Energy Market reports; ACCC retail electricity pricing inquiries.

Bills climbed from $127 a month in 2015 to $145 in 2017, partly following the closure of the Hazelwood coal-fired power station in Victoria. By 2021, average monthly costs had fallen to $135, helped by the 2019 introduction of the Default Market Offer. Average monthly energy bills then rose to $190 by 2023 and reached $208 in 2024 alongside higher global gas prices following Russia's invasion of Ukraine. Government rebate programmes contributed to the reported fall in household bills to $195 in 2025.

Bills vary noticeably between states. Queensland recorded the highest average quarterly electricity bills in 2024 and 2025, ranging from $432 to $499, partly reflecting high summer air-conditioning demand. Victoria's quarterly bills were generally lower, averaging around $368.

Monthly cost, 2025

$195

Combined electricity and gas

Down from $208 in 2024

Peak monthly cost

$208

Recorded in 2024, before rebates

+54% since 2015

Reported electricity price rise

+25.4%

Year to March 2026

ABS estimate

DMO introduced

2019

Price safety net capping standing-offer rates

Regulatory milestone

How rooftop solar affects these averages

Rooftop solar panels are now common across Australia, with total installed capacity exceeding 20 gigawatts by 2025. These monthly averages cover all households, regardless of whether they have solar panels, so individual costs can vary considerably based on system size and household usage.

What caused the energy price spike in 2022 and 2023?+

The main cause was rising global gas prices after Russia invaded Ukraine in February 2022. Australia's east coast gas prices are linked to international markets. Gas-fired power plants are used heavily during peak demand periods, so higher gas costs also pushed electricity prices up. Bills climbed from $135 a month in 2021 to $208 by 2024 before government rebates reduced the reported cost.

Why did the reported energy bill fall in 2025 if wholesale prices are still high?+

The fall from $208 in 2024 to $195 in 2025 reflects government rebates rather than lower underlying retail prices. The federal Energy Bill Relief Fund committed $3.5 billion for 2024 to 2025, providing eligible households with rebates of up to $300, supplemented by state schemes. Reported electricity prices later rose 25.4% in the year to March 2026, partly reflecting the unwinding of earlier rebate effects.

Section 03Water bills

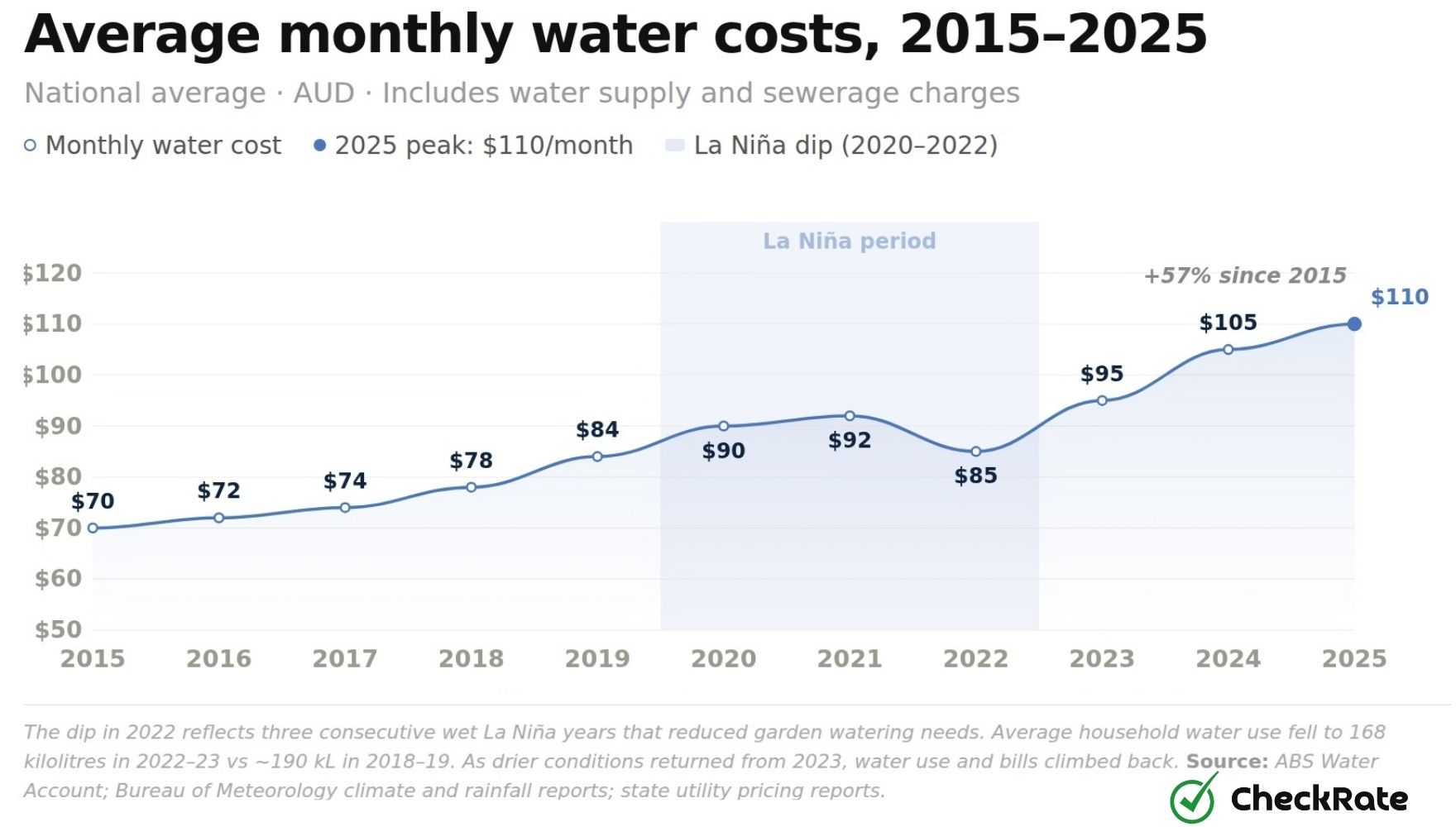

Average water bill fixed service fees shape monthly costs

Average monthly water costs reached $110 in 2025, up 57% from $70 in 2015. Fixed service fees account for a large share of each quarterly invoice, which means lower household water use may not reduce the total bill by the same proportion.

Average monthly water costs, 2015–2025

National average, AUD · Includes water supply and sewerage charges

The dip in 2022 reflects three consecutive wet years that reduced garden watering needs. Average household water use fell to 168 kilolitres in 2022 to 2023, compared to roughly 190 kilolitres in 2018 to 2019.

Source: ABS Water Account; Bureau of Meteorology climate and rainfall reports; state utility pricing reports.

Bills rose fastest in 2018 and 2019, climbing from $78 to $84 a month, during a period of severe drought when dam storage fell and reliance on more expensive desalination plants increased. Average monthly water bills dipped to $85 in 2022 following three consecutive La Niña wet years. As drier conditions returned in 2023 and 2024, household water use climbed back to 174 kilolitres per household and average bills reached $105 a month in 2024 and $110 in 2025.

$326

Average quarterly bill · South East QLD

South East Queensland records among Australia's highest water bills

Brisbane and surrounding areas record some of the highest average quarterly water bills in the country. Fixed sewerage and access charges account for a large share of the total. Western Australia has historically recorded lower average household water costs than many other states.

Why do water bills vary between states?+

Water pricing is set by state governments, regulators and water utilities, so bills vary across the country. South East Queensland records some of the highest average bills nationally, with fixed sewerage and access charges accounting for a large share. Western Australia has historically recorded lower average household water costs than many other states. Desalination infrastructure can also affect costs where it is used.

How much of a water bill is affected by usage?+

Only the usage-based portion of a water bill changes with household consumption. A large share of many water bills is made up of fixed service fees, which apply regardless of usage. Garden watering can affect the usage-based portion, which helps explain why average bills dipped in 2022 during a period of heavy rainfall.

Section 04Phone and internet bills

Average phone and internet bill remained stable

Phone and internet costs averaged $125 a month in 2025, compared with $130 in 2015. This makes phone and internet the only major household bill in this article to record a lower nominal monthly cost over the decade. After accounting for general price inflation, the real cost was lower than in 2015.

In the 12 months to March 2026, phone and internet prices rose by 1.4%, compared with headline inflation of 4.6%. While monthly costs have stayed close to their 2015 level, the service being purchased has changed. Internet speeds, mobile data allowances and overall data use have increased substantially. National data use reached approximately 13.9 million terabytes in the final three months of 2023.

Average monthly phone and internet costs vs. annual inflation rate, 2015–2025

Average monthly cost (left) vs. headline CPI growth (right)

CPI

Phone & internet

Phone and internet prices rose by 1.4% in the year to March 2026, below headline inflation of 4.6%.

Source: ABS CPI historical index; Australian Communications and Media Authority (ACMA) trends reports.

The relatively stable price trend may reflect competition across the telecommunications market. Smaller providers that rent network access from major carriers have added price pressure, particularly in mobile plans. Costs edged up between 2015 and 2017 as the NBN rollout moved more households onto faster, higher-tier plans. Some price rises returned in 2024 and 2025 as major carriers increased rates on home internet and mobile plans, partly linked to 5G network investment.

Why did phone and internet costs fall while every other bill rose?+

Phone and internet costs fell from $130 a month in 2015 to $125 in 2025, a 4% decline over a decade when general prices rose by roughly 30%. One factor is the low marginal cost of carrying additional data once network infrastructure is in place. Smaller providers that rent network access from major carriers have added price competition. By comparison, energy, water and insurance are more directly linked to physical input costs, many of which increased over the same period.

Section 05Insurance premiums

Average home insurance bill reaches $244 a month

Home and contents insurance recorded the largest proportionate increase of any bill category over the decade. The average annual home and contents insurance premium reached $2,938 in 2025, equivalent to about $244 per month. This was 103% higher than in 2015 and 51% higher than in 2020, making insurance the fastest-rising bill category in this comparison.

Average monthly home and contents insurance premium, 2015–2025

National average annual premium divided by 12, AUD

The largest increases occurred from 2020 onwards, following the Black Summer bushfires and the 2022 East Coast floods. Rising claims risk and higher building costs contributed to higher premiums.

Premiums rose from $120 a month in 2015 to $161 by 2020, a 34% increase over five years. Major flooding across northern New South Wales and South East Queensland in 2021 and 2022 coincided with another rise, with the average monthly premium increasing from $175 to $190. International reinsurers, which provide financial backing to insurance companies, also raised rates or reduced exposure in some higher-risk areas.

Regional pricing gaps are significant

In flood-exposed western suburbs of Brisbane, average annual premiums reached $8,396 in 2025. Cyclone-exposed areas of northern Western Australia averaged $4,395 per year, and Darwin recorded capital city averages above $4,000. In contrast, lower-risk urban areas of South Australia and Victoria averaged closer to $2,000 annually. The national average of $2,938 masks wide variation by location and risk profile.

Average annual home and contents insurance premium by region, 2025

Selected regions · Annual premium, AUD · National average shown for reference

The Brisbane flood-suburb figure reflects postcode-level risk pricing following repeated flood events. Higher-risk zones can record substantially higher premiums than lower-risk areas.

The average monthly premium reached $210 in 2023 and $233 in 2024, partly driven by rising building costs. Material and labour shortages during and after the COVID-19 pandemic made rebuilding homes more expensive. Because home insurance covers the full cost of rebuilding, higher construction costs flow directly into higher premiums. Rising premiums have also been linked to underinsurance: some households reduce their level of cover or cancel policies when premiums become less affordable.

Why is insurance so much more expensive in Queensland and northern Australia?+

These regions face a much higher risk of floods and cyclones than most other parts of Australia, which makes them more expensive to insure. The 2019 to 2020 bushfires and 2022 East Coast floods prompted global insurers to reassess Australian risk and raise their rates. For high-risk postcodes, that repricing was steep.

What has driven the national average premium up by 103% since 2015?+

Three main factors drove the rise from $120 a month in 2015 to $244 in 2025: major weather disasters lifted reinsurance costs; building costs rose rapidly from 2020 to 2023; and some insurers reduced or withdrew coverage from high-risk areas, leaving fewer providers and less competitive pricing.

Section 06Debt repayments

Average new mortgage repayment increased after 2021

Estimated monthly repayments on the average new owner-occupier loan reached about $4,237 in 2025, up about 75% from $2,416 in 2021 and about 90% above the 2015 figure of $2,233. This figure applies only to owner-occupiers with a home loan and is separate from the $674 monthly average for other household bills.

Average monthly mortgage repayment, 2015–2025

Based on average new home loan size · 30-year term · Average standard variable rate

Monthly repayment

RBA cash rate

Monthly repayments stayed relatively stable from 2015 to 2021 even as loan sizes grew, because interest rate cuts kept monthly costs down. When interest rates rose from 2022 to 2024, repayments increased from $2,416 a month in 2021 to $4,613 in 2024.

Monthly repayments started at $2,233 in 2015, reached $2,580 in 2018, then fell to $2,416 in 2021. This occurred even as average loan sizes grew from $389,000 to $600,000. The cash rate, the key interest rate set by the Reserve Bank of Australia, rose from 0.10% to 3.10% during 2022, then reached 4.35% in late 2023. Home loan rates followed, reaching around 6.42% by 2024.

On an average loan of around $700,000, higher rates were associated with a sharp rise in monthly repayments. Average repayments increased from $2,416 in 2021 to $4,200 in 2023 and $4,613 in 2024. Rate cuts in 2025 brought the cash rate down to 4.10%, and average monthly repayments fell to $4,237 — still higher than any figure recorded before 2022.

Average new owner-occupier loan size by state, 2025

Monthly repayment calculated on a 30-year term at the 2025 average variable rate of 5.62%

State

Average loan size

Monthly repayment (est.)

New South Wales

$873,000

$5,030

Victoria

$680,000

$3,920

Queensland

$680,000

$3,920

Western Australia

$600,000

$3,457

South Australia

$570,000

$3,284

Tasmania

$504,000

$2,904

National average

$736,000

$4,237

Repayment estimates are rounded and based on a 30-year principal-and-interest loan using the 2025 average variable rate of 5.62%. NSW and Tasmania figures are sourced directly from lending data; other state figures are estimates. Source: ABS Lending Indicators; RBA, 2025.

Average loan size does not equal average property value

The average new loan in 2025 was $736,000. With a 10% deposit, that implies a property value of roughly $818,000. The loan figure reflects the amount borrowed, not the total purchase price. Loan sizes have increased partly because property prices have risen, and partly because lower interest rates in 2020 and 2021 increased borrowing capacity.

How are the average mortgage repayment figures calculated?+

Each figure is based on the average new home loan for that year, repaid over 30 years at the prevailing average variable interest rate. Actual repayments vary depending on the interest rate, loan term, and whether extra repayments have been made.

Why did mortgage repayments nearly double between 2021 and 2024?+

Monthly repayments climbed from $2,416 in 2021 to $4,613 in 2024, a 91% increase in three years. The Reserve Bank raised the cash rate from a record low of 0.10% to a peak of 4.35% between 2022 and late 2023. At the same time, average loan sizes had already grown to around $600,000 to $694,000 during the low-rate period.

Section 07Wages vs bill inflation, 2015–2025

Real wages fell as inflation outpaced pay growth

Real wages, which measure wage growth after inflation, fell by 4.4% in 2022. This was the largest annual fall in the available series. Prices rose by 7.8% that year, while wages grew by 3.4%. This means the same level of income bought less than it did a year earlier.

Wage growth vs. price growth, 2015–2025

Annual growth rates · Real wage growth = wage growth minus price growth

Wage Price Index

Consumer Price Index

From 2015 to 2020, wages and prices grew at a similar pace. In 2021 and 2022, prices rose faster than wages. Small real wage gains returned from 2023 to 2025, but did not offset the earlier losses.

Source: ABS Wage Price Index and Consumer Price Index historical time series; RBA inflation measures.

Wage growth vs. price growth, 2015–2025

Annual growth rates and real wage growth (wage growth minus price growth)

Year

WPI growth

CPI growth

Real wage growth

2015

2.2%

1.7%

+0.5%

2016

1.9%

1.5%

+0.4%

2017

2.1%

1.9%

+0.2%

2018

2.3%

1.8%

+0.5%

2019

2.2%

1.8%

+0.4%

2020

1.3%

0.9%

+0.4%

2021

2.4%

3.5%

−1.1%

2022

3.4%

7.8%

−4.4%

2023

4.2%

4.1%

+0.1%

2024

4%

3.6%

+0.4%

2025

3.4%

3.2%

+0.2%

Source: ABS Wage Price Index and Consumer Price Index historical time series; RBA inflation measures.

Wages grew by 2.4% in 2021 as prices began to rise, and by 3.4% in 2022 when prices rose by 7.8%. Australian wages are set through a mix of enterprise agreements, individual arrangements and annual wage decisions. These processes can respond more slowly than sudden price increases, which means wage growth may lag inflation during periods of rapid price change.

Wages grew by 4.2% in 2023, slightly above price growth of 4.1%. Real wage growth then remained positive but small, at +0.1% in 2023, +0.4% in 2024 and +0.2% in 2025. These gains did not fully reverse the earlier decline. Essential bills reached $674 a month in 2025, compared with $447 in 2015, meaning essential costs accounted for a larger share of household income than earlier in the decade.

Wages are now growing slightly faster than prices, but essential bills remain well above pre-surge levels. A larger share of household income now goes toward essential costs than a decade ago.

What does "real wage growth" mean for household budgets?+

In 2022, prices rose 7.8% while wages grew just 3.4%, producing a real wage fall of 4.4%. That means the average Australian worker's income bought less than the year before. When wages grow faster than prices, people can afford more with the same income.

Are wages now keeping up with the cost of household bills?+

Marginally. Wages returned to growing slightly faster than prices in 2023 (+0.1%), 2024 (+0.4%) and 2025 (+0.2%). However, essential bills remain well above their level before the 2021 to 2023 price surge. The 51% increase in non-mortgage bills since 2015 has not been reversed.

InteractiveExplore the data

Bills at a glance

Three views of the same data: year explorer, 2025 breakdown, and bill estimator.

2025 national averages · Total essential bills excluding mortgage

$674

per month

Home and contents insurance

$24436%

Electricity and gas

$19529%

Phone and internet

$12519%

Water

$11016%

Insurance is now the largest single essential bill category, accounting for 36% of the non-mortgage total. It represented only 27% of the same basket in 2015.

Source: ABS CPI; AER; Finity. 2025 national averages.

General information only

This article presents general information about household expenses in Australia, based on publicly available government and industry data. It is intended for research and reference only and does not constitute financial advice. Figures are national averages and may not reflect individual household circumstances.

References

1.ABS Consumer Price Index: Quarterly CPI releases 2015–2025; December 2025 released 28 Jan 2026; March 2026 released 29 Apr 2026.

2.ABS Lending Indicators: Monthly and quarterly lending series 2015–2025; December quarter 2025 released 11 Feb 2026.

3.ABS Wage Price Index: Quarterly wage growth series 2015–2025; December quarter 2025 released 18 Feb 2026.

4.ABS Water Account: Household water use data; 2023–24 financial year released 11 Dec 2025.

Methodology: Monthly bill estimates are modelled national averages. Baseline dollar amounts were adjusted using relevant ABS CPI sub-indices for each bill category and cross-checked against regulator, utility and industry data. Figures should be read as broad national estimates rather than direct household survey results. Mortgage repayments are modelled separately using average new owner-occupier loan sizes, a 30-year principal-and-interest term and average standard variable owner-occupier lending rates.

Data Snapshots

Average Monthly Water CostsAverage Monthly Electricity and Gas Costs