In FY2025, Australian households saved around 6 cents of every dollar they earned, up from 3 cents the year before. Over the past decade, total household wealth more than doubled, driven by rising property values, higher superannuation balances and stronger household income growth.

10 min read 18 May 2026Updated 02 July 2026 Fact checked

Key findings · FY2024–25

6.1%

Saving rate in FY2025, up from 3.0% the year prior

$274B

Total household saving, up $58B year on year

$17.9T

Total household wealth, more than double the FY2015 level

$4.33T

Superannuation balance, up 93% since FY2015

Section 01National savings

What is Australia's household saving rate?

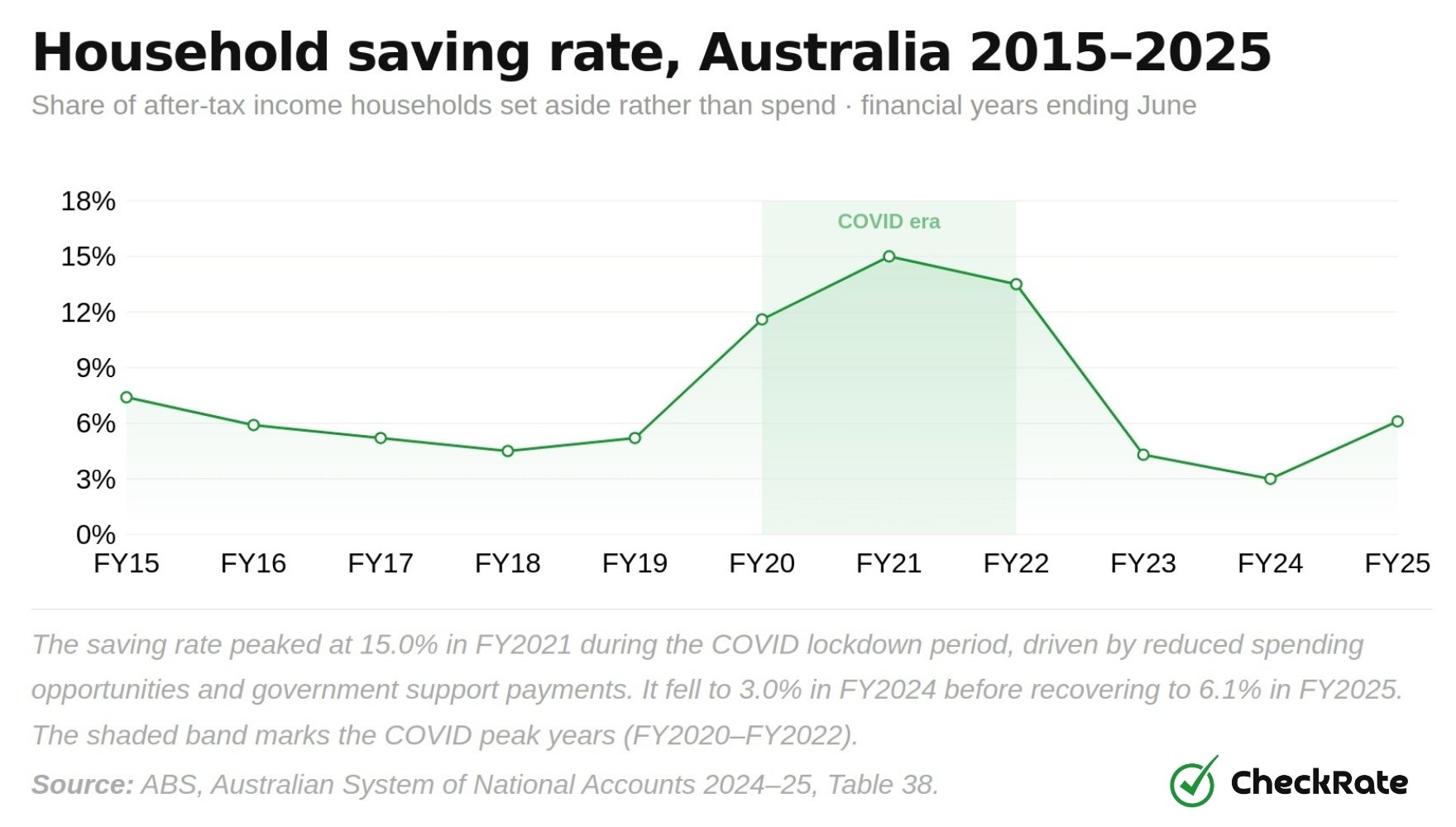

Australia's saving rate shifted over the past decade. Before the pandemic, it sat between 4.5% and 7.4%. When COVID lockdowns limited people's spending, savings increased. By FY2021, the saving rate had reached a peak of 15.0%. As restrictions lifted and spending returned, it fell. Inflation reaching 6.2% in FY2022 and interest rates rising quickly added further pressure. By FY2024, the rate had fallen to 3.0%, the lowest in the decade. The rate returned to 6.1% in FY2025 as income growth outpaced spending.

Saving Rate · FY2025

6.1%

↑ Up from 3.0% in FY2024

Below the FY2021 COVID peak of 15.0%

Total Household Saving · FY2025

$274B

↑ Up $58B year on year

From $176.4B in FY2015

Economy-Wide Saving · FY2025

$114B

↓ Down from $179.9B peak

FY2022 was the decade high

Household saving rate, Australia 2015–2025

Share of after-tax income households set aside rather than spend · financial years ending June

The saving rate peaked at 15.0% in FY2021 during the COVID lockdown period, driven by reduced spending opportunities and government support payments. It fell to 3.0% in FY2024 before recovering to 6.1% in FY2025. The shaded band marks the COVID peak years (FY2020–FY2022).

Source: ABS, Australian System of National Accounts 2024–25, Table 38.

What is the saving rate?

The saving rate shows what share of after-tax income households set aside rather than spend. At 6.1%, for every $100 earned, $6.10 was saved. It is a national average. Individual results differ, particularly for households with large mortgage repayments at current interest rates.

How much do Australians save each year?

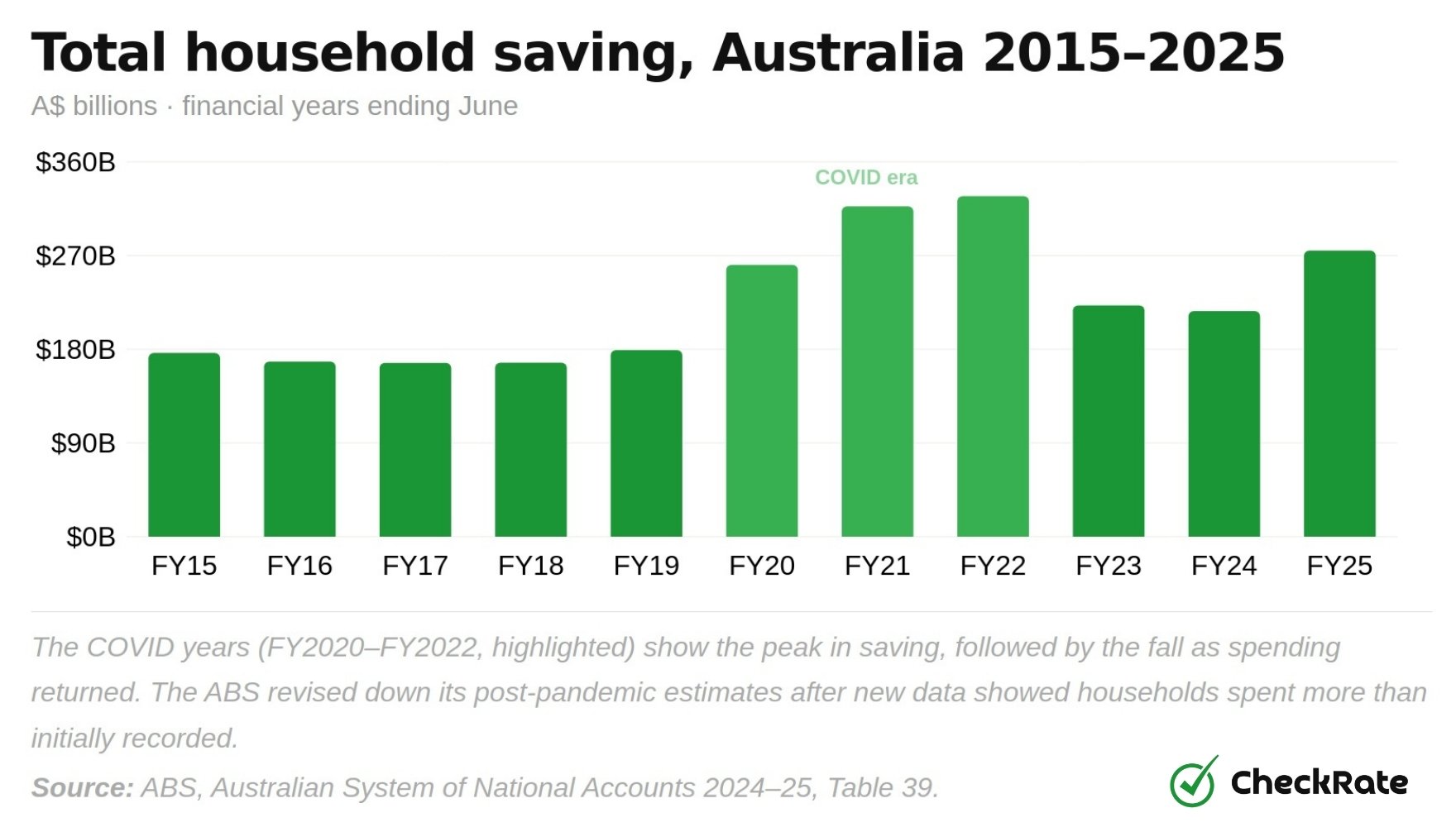

In dollar terms, Australians saved between $166 billion and $179 billion in most years before COVID. During the pandemic years saving rose, reaching a peak of $327.1 billion in FY2022. As spending returned, saving fell. By FY2024, total household saving was down to $216.7 billion. It rose again to $274.7 billion in FY2025, with income growing faster than spending for the first time in several years.

Total household saving, Australia 2015–2025

A$ billions · financial years ending June

The COVID years (FY2020–FY2022, highlighted) show the peak in saving, followed by the fall as spending returned. The ABS revised down its post-pandemic estimates after new data showed households spent more than initially recorded.

Source: ABS, Australian System of National Accounts 2024–25, Table 39.

The RBA attributed the pandemic-era rise to three main factors. These included fewer places to spend money during lockdowns, low interest rates on existing debts, and government support payments, including JobKeeper.

The post-pandemic period reversed all three. Inflation peaked at 6.2% in FY2022, interest rates rose quickly, and real incomes fell. The rate recovered in FY2025 as inflation came back to 2.1% and incomes grew.

Australia's national savings data: 2015–2025

Year

National Saving

Household Saving

Household Income

Household Spending

Saving Rate

Inflation

FY2015

78.9

176.4

1,093.7

917.3

7.4%

1.5%

FY2016

39.3

168.2

1,119.7

951.5

5.9%

1.0%

FY2017

70.1

166.9

1,150.6

983.7

5.2%

1.9%

FY2018

71.8

167.1

1,192.4

1,025.3

4.5%

2.1%

FY2019

92.3

179.2

1,240.7

1,061.5

5.2%

1.5%

FY2020

111.7

261.0

1,304.5

1,043.5

11.6%

−0.3%

FY2021

163.7

317.3

1,382.7

1,065.4

15.0%

3.8%

FY2022

179.9

327.1

1,473.5

1,146.3

13.5%

6.2%

FY2023

167.1

222.0

1,524.0

1,302.0

4.3%

6.0%

FY2024

137.3

216.7

1,595.1

1,378.4

3.0%

3.8%

FY2025

114.2

274.7

1,715.7

1,441.0

6.1%

2.1%

Highlighted rows = COVID saving peak (FY2020–FY2022). All dollar figures current-price A$ billions. HH = Household. Saving rate = saving as a share of after-tax income. Inflation = year-ended CPI to June.

Section 02Where Australians save

Where do Australians put their savings?

Household savings in Australia usually end up in three main places. Some goes into bank deposits, some into superannuation, and much of it is tied up in physical assets such as residential property.

All three have grown over the past decade. Superannuation saw the largest dollar increase, up $2.09 trillion, while property values also rose considerably. Total wealth more than doubled from $8.55 trillion in FY2015 to $17.92 trillion in FY2025, due as much to rising asset values as to new savings each year.

Total Wealth · FY2025

$17.9T

Up from $8.5T in FY2015

Superannuation · FY2025

$4.33T

Up 93% over the decade

Bank Deposits · FY2025

$1.86T

Up from $900.5B in FY2015

Total Debts · FY2025

$3.31T

Debts = 193% of income

How much do Australians have in bank deposits and super?

Bank deposits grew from $900.5 billion in FY2015 to $1.86 trillion in FY2025, up 107%. Superannuation grew faster, from $2.24 trillion to $4.33 trillion over the same period, up 93%. This reflects the compulsory super rate rising from 9.5% to 11.5%, as well as investment returns over the period. The dip in super balances in FY2022 was caused by sharemarket falls that year, not withdrawals.

Bank deposits and superannuation balances, 2015–2025

A$ trillions · end-of-year balances

Bank Deposits

Superannuation

These are balances, not annual contributions. Super grows through employer contributions, personal top-ups and investment returns, so the balance rises even in years when take-home pay is flat. The small dip in FY2022 reflects sharemarket losses, not withdrawals.

Source: ABS, Finance and Wealth, December 2025, Table 35.

Did you know

Australia's superannuation pool is among the largest pension systems in the world relative to the size of its economy. The Superannuation Guarantee rate reached 11.5% in FY2025, up from 9.5% in FY2015. Over the decade, superannuation balances grew by $2.09 trillion in absolute dollar terms, more than twice the $963 billion increase in bank deposits.

What is the average Australian household worth?

Total household wealth, meaning everything households own minus everything they owe, crossed $10 trillion in FY2017 and has more than doubled since FY2015. The largest single-year increase came in FY2021, when property prices rose during the pandemic, and total wealth grew by more than $2.1 trillion. By FY2025, financial holdings alone stood at $8.37 trillion, up from $4.19 trillion a decade earlier. This includes deposits, super, shares and similar assets, but excludes property.

$17.9T

Total household wealth has more than doubled since 2015

Australian household wealth reached $17.92 trillion in FY2025, up from $8.55 trillion in FY2015. That is a gain of more than $9.3 trillion, with the largest increases linked to property and superannuation.

Total household wealth and financial holdings, 2015–2025

A$ trillions · end-of-year balances

Total Wealth

Financial Holdings

The gap between the two lines is mostly housing. Financial holdings include bank deposits, superannuation, shares and similar assets, but not property. As house prices rose through FY2021 and beyond, total wealth grew faster than financial holdings alone.

Source: ABS, Finance and Wealth, December 2025, Table 35.

How much debt do Australians have compared to their income?

Despite rising wealth, Australian households carry among the highest debt loads in the developed world. Total debt as a share of after-tax income has remained above 184% throughout the decade. The ratio peaked at 199.7% in FY2018 and was at 193.1% in FY2025. The average for developed countries is around 120 to 130%. The main reason is mortgages.

Household debt vs income ratio, Australia 2015–2025

Total debts as a share of after-tax income · financial year end

The ratio has changed little over ten years. Debt has grown, but so has income, keeping it high. A falling ratio does not always mean households are paying off debt. It can simply mean incomes grew faster that year.

Source: ABS, Finance and Wealth December 2025, Table 35; Australian System of National Accounts 2024–25, Table 38.

Rising wealth does not erase household debt

Total household wealth has grown while debt levels have stayed high. Much of that wealth is in property that is not easy to convert to cash, while much of the debt is tied to mortgages with monthly repayments. Rate rises in 2022 and 2023 showed the strain. The RBA noted in April 2025 that mortgage arrears had risen in every state and territory from their 2022 lows, even as overall wealth kept growing.

Australian household savings and debts by year: 2015–2025

Year

Bank Deposits

Superannuation

Total Assets

Total Debts

Net Worth

Debt vs Income

FY2015

900.5

2,242.0

4,188.2

2,016.2

8,549.4

184.3%

FY2016

980.7

2,424.0

4,506.3

2,132.1

9,091.2

190.4%

FY2017

1,042.0

2,631.9

4,851.6

2,259.7

10,044.2

196.4%

FY2018

1,088.8

2,815.5

5,172.3

2,381.6

10,433.3

199.7%

FY2019

1,136.2

3,115.2

5,615.7

2,464.1

10,639.4

198.6%

FY2020

1,228.3

3,131.5

5,745.7

2,521.9

11,247.6

193.3%

FY2021

1,340.5

3,519.5

6,413.8

2,625.7

13,348.5

189.9%

FY2022

1,501.5

3,334.7

6,429.3

2,825.0

14,576.3

191.7%

FY2023

1,606.0

3,625.7

6,933.4

2,975.9

15,163.5

195.3%

FY2024

1,710.7

3,928.5

7,565.4

3,138.3

16,585.1

196.7%

FY2025

1,863.0

4,330.9

8,370.1

3,312.5

17,919.9

193.1%

All figures current-price A$ billions. Bank deposits = currency and deposits. Total assets = financial assets only (excludes property). Net worth = total household assets minus total debts. Debt vs income = total liabilities ÷ after-tax income. Highlighted row = FY2022, peak saving year.

The national figures don't show the variation at state and territory level. NSW and WA households saved at a very different rate to Victoria or South Australia, and the pandemic widened those differences.

Section 03State by State

Which state saves the most money in Australia?

In FY2025, New South Wales led the country with $89.1 billion in household saving, followed by Queensland ($60.2 billion) and Western Australia ($47.8 billion). Together, NSW and Queensland accounted for more than half the national total of $274.7 billion. The figures reflect both population size and income levels, so larger states naturally dominate.

Gross household saving by state & territory, FY2025

Current-price A$ billions · financial year ending June 2025

NSW

$89.1B

QLD

$60.2B

WA

$47.8B

VIC

$31.1B

ACT

$23.8B

SA

$9.5B

NT

$6.9B

TAS

$6.2B

Source: ABS, Australian National Accounts: State Accounts 2024–25, Tables 12–20.

NSW · FY2025 vs FY2015

+86%

NSW household savings rose from $47.8B in FY2015 to $89.1B in FY2025, the largest absolute gain of any state over the decade.

Victoria · Biggest saving change

$31.1B

VIC peaked at $69.9B in FY2021, then fell to $20.2B by FY2024, the largest post-COVID reversal of any state or territory.

Victoria had the most variation of any state over the decade. Extended Melbourne lockdowns pushed household savings to $69.9 billion in FY2021, nearly three times its FY2015 level. Once restrictions lifted, spending came back, and savings fell. By FY2024, Victorian savings were down to $20.2 billion, below its FY2015 level of $23.5 billion. It rose to $31.1 billion in FY2025 but remains below its share of national income.

$69.9B

Victoria's pandemic saving peak

Household saving reached $69.9 billion in FY2021, nearly three times the FY2015 level of $23.5 billion. Extended Melbourne lockdowns reduced spending on services, hospitality and travel for longer than in any other state, which pushed savings higher.

Did you know

South Australia is the only state or territory where FY2025 household savings ($9.5 billion) remain below its FY2015 level ($11.0 billion). Every other jurisdiction recorded gains over the decade, though Victoria's recovery is still incomplete.

Saving trends by state: compare all states 2015–2025

The chart below shows NSW as the default. All states follow a similar pattern, remaining stable pre-COVID, rising sharply between FY2020 and FY2022, then falling as spending returned.

Source: ABS, Australian National Accounts: State Accounts 2024–25.

State and territory savings data: 2015–2025

State

FY15

FY16

FY17

FY18

FY19

FY20

FY21

FY22

FY23

FY24

FY25

NSW

47.8

49.1

51.7

50.9

58.4

87.7

101.8

107.3

72.9

78.9

89.1

VIC

23.5

19.2

20.2

17.3

22.1

45.1

69.9

61.5

26.4

20.2

31.1

QLD

32.5

31.1

31.5

34.5

34.4

47.6

53.0

59.7

43.6

42.3

60.2

SA

11.0

9.6

8.9

9.1

9.1

13.9

17.5

17.9

8.7

7.2

9.5

WA

39.7

36.6

30.8

30.8

30.2

37.5

44.0

47.6

40.6

37.2

47.8

TAS

3.4

3.1

3.0

2.7

2.9

4.4

5.9

6.4

4.4

4.3

6.2

NT

5.2

5.2

5.8

6.2

5.7

5.9

6.0

6.6

5.9

5.9

6.9

ACT

13.4

14.4

15.0

15.6

16.4

18.9

19.3

20.2

19.4

20.7

23.8

Australia

176.4

168.2

166.9

167.1

179.2

261.0

317.3

327.1

222.0

216.7

274.7

All figures current-price A$ billions. The ABS does not publish net savings by state. Figures above are total household savings only. State totals may not sum precisely to the Australia total due to ABS rounding and territorial adjustments.

Section 04Key Trends

How have Australian savings changed over the past 10 years?

The decade from FY2015 to FY2025 breaks into four phases, each shaped by a different economic force.

FY15–19

Pre-pandemic: slight decline

Household savings stayed between $166 and $179 billion while the saving rate fell from 7.4% to 5.2%. Inflation was low at 1 to 2%, but debt levels were already high, running between 184% and 200% of income. Spending and income grew at a similar pace.

FY20–22

COVID-era saving rise

Household savings rose from $179.2 billion in FY2019 to $327.1 billion in FY2022. The saving rate reached 15.0% in FY2021. The RBA cited three drivers: fewer places to spend during lockdowns, low interest rates on debt, and government support payments, including JobKeeper and COVID supplements.

FY23–24

Post-pandemic pressure

Saving fell as inflation hit 6.2% and the RBA raised rates from 0.10% to 4.35%. Total saving was down to $216.7 billion by FY2024, and the saving rate fell to 3.0%, the lowest point of the decade. Real household income per person was around 1% below pre-pandemic levels by early 2025.

FY2025

Recovery

Inflation came back to 2.1%, and incomes grew. Saving rose to $274.7 billion, and the saving rate returned to 6.1%. The ABS noted that rising deposits were supported by income growing faster than spending. Super balances reached a record $4.33 trillion.

"Across all regions, households are experiencing financial pressure, although severe stress remains confined to a relatively small share of borrowers." — RBA Financial Stability Review, April 2025

Why did household wealth keep growing even when people saved less?

Total household wealth grew from $13.3 trillion in FY2021 to $17.9 trillion in FY2025, even as the saving rate fell. This happens because wealth is not just what you save each year. It also includes the rise in value of things you already own.

When house prices and sharemarkets go up, household wealth increases even if households save nothing. The ABS separates wealth changes into three sources: annual saving, other transactions, and asset value gains. This is why Australia can record a saving rate of 3 to 6% and still see total wealth double over ten years.

Household pressures vary across Australia

ABS cost-of-living data for the 12 months to December 2025 showed price increases ranging from 2.3% for working households to 4.2% for age pensioner households. Housing, food and recreation were the main contributors. Households on fixed incomes or with high housing costs faced more pressure than the national average suggests.

About the data

FY2025 figures carry a small data gap because detailed breakdown records for that year are still being finalised, and the ABS may revise the numbers in later releases. State saving figures cover total saving only (not net saving), are estimated by working down from national totals, and assume workers live in the same state they work in. Some entries, particularly privately held company shares, have lower data quality than the debt figures, which come directly from banks and financial institutions.

The Australia household debt statistics article covers total household debts, mortgage commitments, personal loans, student debt and credit card balances using the same decade-long ABS data.

General information only

This article is based on publicly available ABS data. It is general information only and does not constitute financial advice. If you are making decisions about saving for a property purchase, consider speaking with a licensed financial adviser.

References

ABS: Australian System of National Accounts 2024–25, Tables 1, 38 & 39 — national saving, saving rate, household income, spending and total household saving.

ABS: Australian National Accounts: State Accounts 2024–25, Tables 12–20 — household saving by state and territory.

ABS: Finance and Wealth, December 2025, Table 35 — bank deposits, superannuation, financial holdings, debts and total wealth.

ABS: Consumer Price Index, Australia, December 2025, Table 17 — year-ended June inflation used in the national savings table.

ABS: Selected Living Cost Indexes, Australia, December 2025 — household-type cost-of-living comparisons.

RBA: Financial Stability Review, April 2022 — COVID-era saving rise and mortgage buffer accumulation.

RBA: Statement on Monetary Policy, Box B, February 2025 — post-pandemic income, spending and saving revisions.

RBA: Financial Stability Review, April 2025 — household financial pressure and mortgage arrears by state.

Methodology note: all years are financial years ending in June. Dollar figures are current-price A$. State figures are total (gross) household savings only. FY2025 national accounts are subject to revision as detailed records for that year are still being finalised.

Data Snapshots

Household saving rate, Australia 2015–2025Total household saving, Australia 2015–2025 (A$ billions)