How long does it take to save a 20% deposit?

In the March 2026 quarter, Australia's mean dwelling price reached $1,111,100, up from $677,475 in 2017. A 20% deposit on the national mean home is now $222,220.

At the March 2026 household saving ratio of 6.2%, the average annual saving estimate is about $6,933. With no starting savings and no investment return included, it would take approximately 32 years to reach a 20% deposit.

Income has increased over the period, but not as quickly as the deposit required. Average annual income rose from $85,441 in 2017 to $111,815 on the latest November 2025 earnings data, an increase of around 31%. The deposit needed for a mean-priced home rose by 64% over the same period, from $135,495 to $222,220.

That gap shows why the time needed to save a deposit has increased, even as wages have continued to rise.

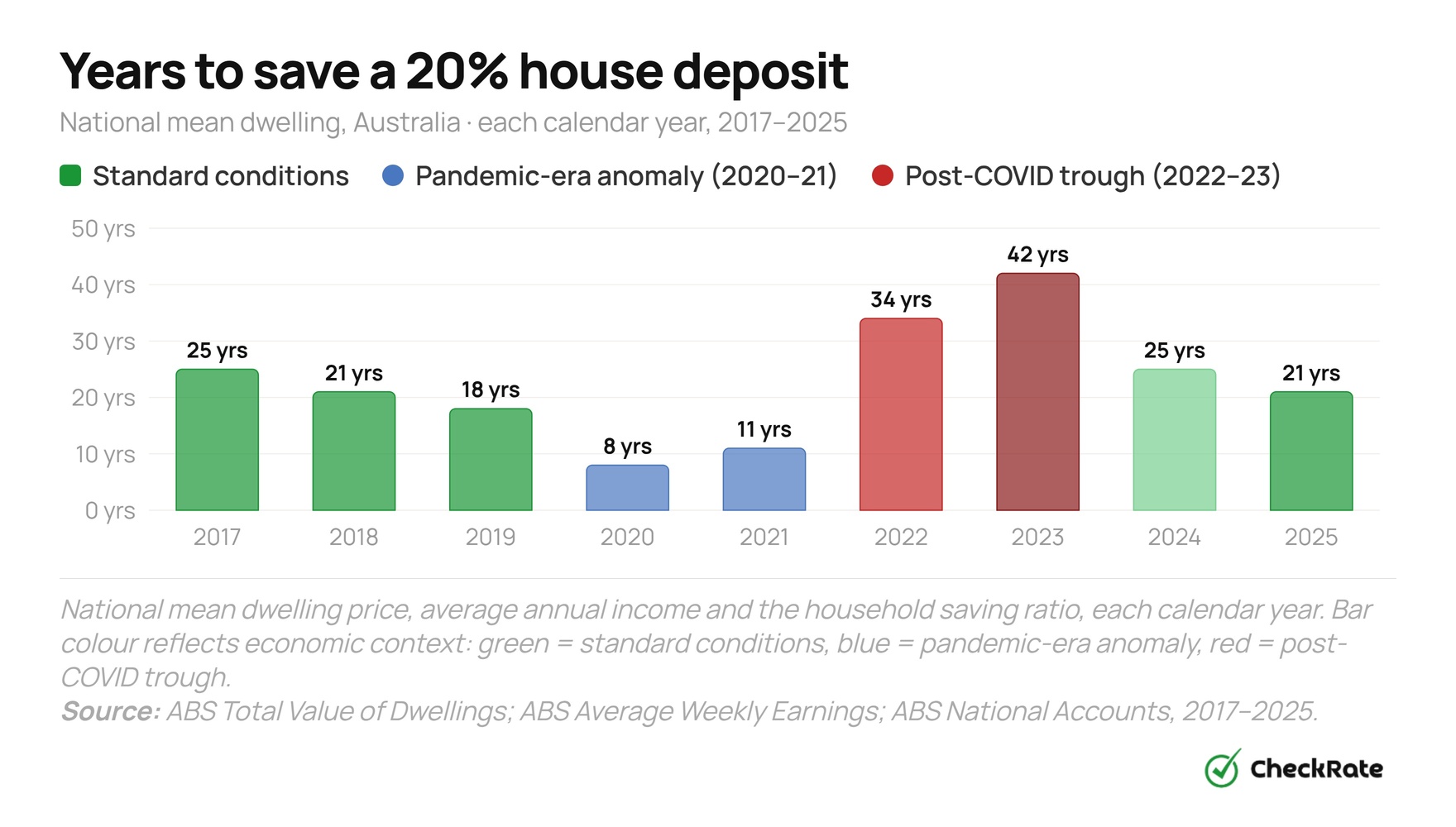

The 2023 result shows how quickly the deposit timeline can change when the saving rate falls. The deposit itself rose by about 1% in 2023, from $181,665 in 2022 to $184,020 in 2023. The larger change was the saving rate, which reduced estimated annual savings from $4,077 to $3,472.

By 2025, the household saving ratio had recovered to 6.1%, bringing the deposit timeline back to 31 years, close to the 31-year timeline recorded in 2017, even though the deposit required was higher in dollar terms. On the latest March 2026 data, the ratio edged up slightly to 6.2% over the quarter and mean prices rose further, extending the national timeline to 32 years.

How saving rates affect deposit timelines

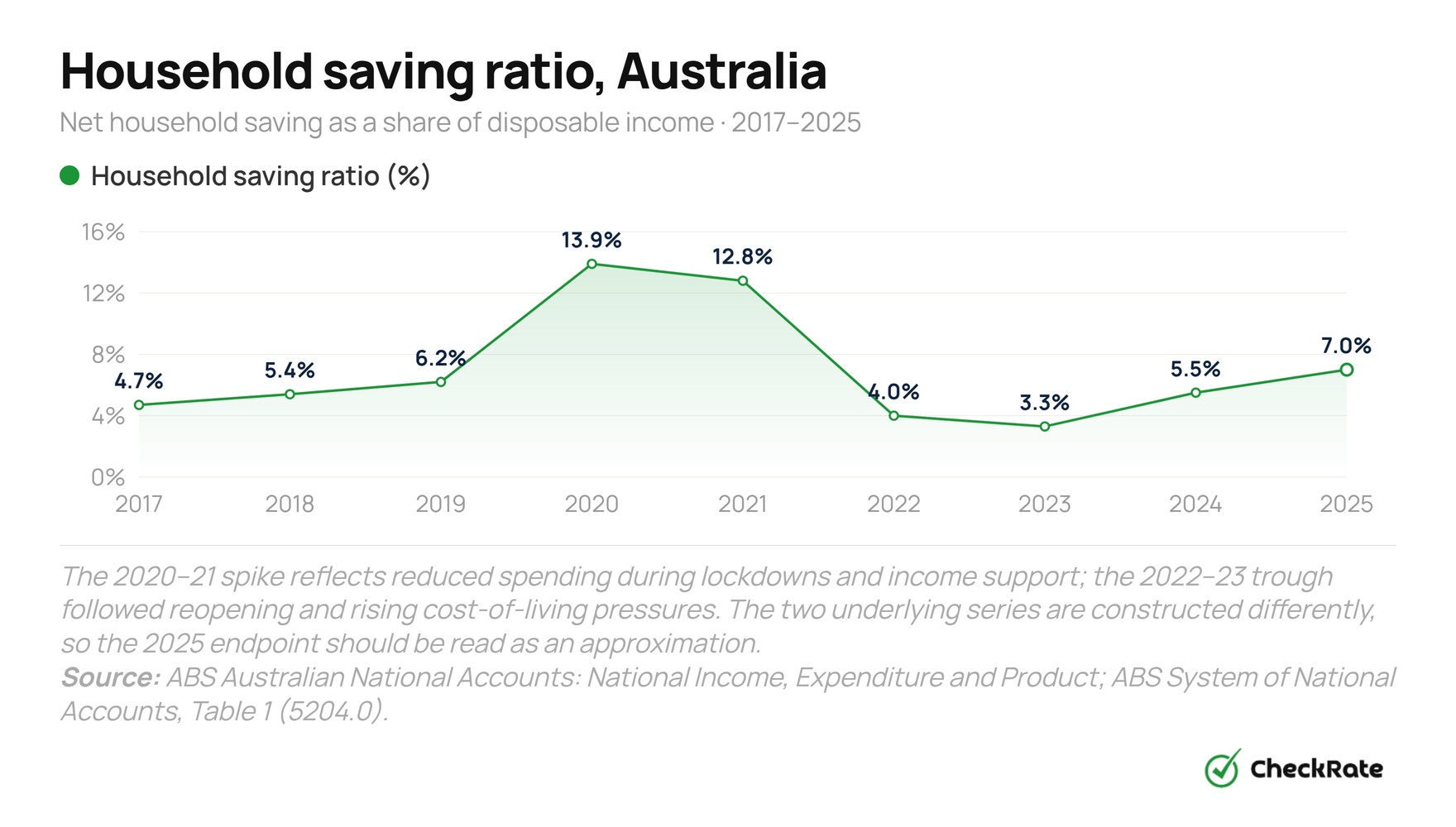

The household saving ratio is a primary input in how long it takes to save a deposit. Between 2017 and 2025, it ranged from 3.3% to 13.9%, a span of more than four times. Across those years the estimated deposit-saving timeline moved between 11 years and 53 years, though that range reflects changes in dwelling prices as well as the saving rate.

By 2025, the saving ratio had recovered to 6.1%, but it remained below the levels recorded during the COVID saving period. On the latest March 2026 data, it read 6.2% on a quarterly basis. That kept the national deposit-saving timeline well above the 11-year and 13-year estimates recorded in 2020 and 2021.

Where you buy determines how long it takes to save

The national estimate of 32 years covers a wide range across the states. On the latest March 2026 figures, the deposit-saving timeline runs from 18 years in the Northern Territory to 38 years in New South Wales, a 20-year gap driven mostly by dwelling prices. The calculation applies the same national saving rate across all states and territories.

New South Wales has the longest estimate, while the Northern Territory has the shortest. Queensland is the only other state above the national 32-year estimate. Most other states and territories sit below the national figure because their mean dwelling prices, deposit thresholds or average earnings produce shorter timelines under the same calculation.

House deposit saving time by state and territory

Deposit-saving times vary widely across Australia because mean dwelling prices and average earnings differ by state and territory. On the latest March 2026 figures, the estimated timeline ranges from 18 years in the Northern Territory to 38 years in New South Wales.

New South Wales and Queensland sit above the 32-year national estimate, while South Australia and Western Australia sit just below it at 30 years. Every other state and territory has a shorter estimated timeline under the same March 2026 saving-rate method.

| State / territory | Mean price | 20% deposit | Annual saving | Years to save |

|---|---|---|---|---|

|

Rest of NT

NT · Regional

|

$460,000 | $92,000 | $7,462/yr |

|

|

Rest of SA

SA · Regional

|

$595,000 | $119,000 | $7,311/yr |

|

|

Rest of WA

WA · Regional

|

$661,000 | $132,200 | $8,372/yr |

|

|

Rest of Vic

VIC · Regional

|

$625,000 | $125,000 | $7,570/yr |

|

|

Rest of Tas

TAS · Regional

|

$620,000 | $124,000 | $6,872/yr |

|

|

Darwin

NT · Capital city

|

$750,000 | $150,000 | $7,462/yr |

|

|

Rest of NSW

NSW · Regional

|

$825,000 | $165,000 | $7,827/yr |

|

|

Rest of Qld

QLD · Regional

|

$815,000 | $163,000 | $7,609/yr |

|

|

Melbourne

VIC · Capital city

|

$850,000 | $170,000 | $7,570/yr |

|

|

Hobart

TAS · Capital city

|

$740,000 | $148,000 | $6,872/yr |

|

|

Perth

WA · Capital city

|

$1,000,000 | $200,000 | $8,372/yr |

|

|

Canberra

ACT · Capital city

|

$1,071,300 | $214,260 | $8,311/yr |

|

|

Adelaide

SA · Capital city

|

$980,000 | $196,000 | $7,311/yr |

|

|

Brisbane

QLD · Capital city

|

$1,150,000 | $230,000 | $7,609/yr |

|

|

Sydney

NSW · Capital city

|

$1,485,000 | $297,000 | $7,827/yr |

|

|

Australia

National average

|

$824,627 | $164,925 | $7,827/yr |

|

How the current timeline compares with the previous quarter

The figures above use the latest March 2026 data. A quarter earlier, in the December 2025 quarter, the household saving ratio was higher at 7.0%, compared with 6.2% in March 2026, and mean dwelling prices were lower. Both changes lengthened the deposit-saving timeline: nationally from 28 years in the December 2025 quarter to 32 years on the current figures, with every state and territory extending.

In the December 2025 quarter, at the higher 7.0% saving ratio, the estimated NSW annual saving amount was approximately $7,827 per year, against $6,932 at the current 6.2% rate. Combined with a lower mean price in that quarter, that produced a New South Wales timeline of 34 years, four years shorter than the current 38-year figure.

Between the December 2025 quarter and the current March 2026 figures, every state and territory extends by two to five years. Queensland and Western Australia recorded the largest increases, both rising by five years, while the Northern Territory recorded the smallest increase, rising by two years. The table below shows the December 2025 quarter starting figures for each market.

| State / territory | Mean price | 20% deposit | Annual saving | Years to save |

|---|---|---|---|---|

|

Rest of NT

NT · Regional

|

$460,000 | $92,000 | $6,609/yr |

|

|

Rest of SA

SA · Regional

|

$595,000 | $119,000 | $6,476/yr |

|

|

Rest of WA

WA · Regional

|

$661,000 | $132,200 | $7,415/yr |

|

|

Rest of Vic

VIC · Regional

|

$625,000 | $125,000 | $6,705/yr |

|

|

Rest of Tas

TAS · Regional

|

$620,000 | $124,000 | $6,087/yr |

|

|

Darwin

NT · Capital city

|

$750,000 | $150,000 | $6,609/yr |

|

|

Rest of NSW

NSW · Regional

|

$825,000 | $165,000 | $6,932/yr |

|

|

Rest of Qld

QLD · Regional

|

$815,000 | $163,000 | $6,739/yr |

|

|

Hobart

TAS · Capital city

|

$740,000 | $148,000 | $6,087/yr |

|

|

Melbourne

VIC · Capital city

|

$850,000 | $170,000 | $6,705/yr |

|

|

Perth

WA · Capital city

|

$1,000,000 | $200,000 | $7,415/yr |

|

|

Canberra

ACT · Capital city

|

$1,071,300 | $214,260 | $7,361/yr |

|

|

Adelaide

SA · Capital city

|

$980,000 | $196,000 | $6,476/yr |

|

|

Brisbane

QLD · Capital city

|

$1,150,000 | $230,000 | $6,739/yr |

|

|

Sydney

NSW · Capital city

|

$1,485,000 | $297,000 | $6,932/yr |

|

The gap between the most and least affordable markets widens slightly under the lower saving rate. New South Wales at 38 years and the Northern Territory at 18 years are now 20 years apart, up from 18 years in the revised December 2025 quarter estimate. The widening is driven by both higher mean dwelling prices in the March quarter and the reduced saving capacity that applies across every state.

Policy pathways for first-home buyers

Government schemes can reduce the upfront deposit needed to buy a home or make it more tax-effective to save one. For eligible first-home buyers, this can shorten the time needed to reach a deposit.

The two main federal pathways are the First Home Guarantee Scheme, which allows eligible buyers to purchase with a minimum 5% deposit, and the First Home Super Saver Scheme, which lets buyers use eligible voluntary super contributions toward a deposit. Both schemes have eligibility rules, property requirements and contribution limits that can change over time, so they may not apply to every buyer.

What changes the deposit-saving timeline?

The deposit-saving timeline changes when one of the inputs changes: the annual saving amount, the deposit size or the dwelling price used in the calculation. The examples below show how sensitive the estimate is to those inputs.

Note: The national figures used throughout this article are a baseline only. Individual saving capacity varies by income, household size, location and living costs.

- ABS: Total Value of Dwellings, March quarter 2026, dwelling values, mean dwelling prices and residential property data.

- ABS: Average Weekly Earnings, Australia, November 2025, average weekly earnings and wage data.

- ABS: Australian National Accounts: National Income, Expenditure and Product, March quarter 2026, household income and national accounts data.

- Housing Australia: Australian Government 5% Deposit Scheme, Australian Government 5% Deposit Scheme details and 2025 expansion.

- Deposit target = ABS mean dwelling price × 20%

- Prices use the ABS mean price of residential dwellings by state and nationally. The ABS publishes this mean at the state and national level, while median dwelling prices are released separately by capital city. Because a mean can be pulled upward by higher-value properties, the timelines are best read as relative comparisons rather than typical buyer estimates.

- Annual saving = average full-time state income × national household saving ratio (6.2% for the March 2026 quarter; 7.0% for the December 2025 quarter comparison)

- Years to save = deposit ÷ annual saving, rounded to the nearest year

- No starting savings are assumed and no investment return on accumulated funds is modelled

- The national saving ratio is applied uniformly across all states and territories

- All figures are nominal and not adjusted for inflation or future price growth

Data Snapshots