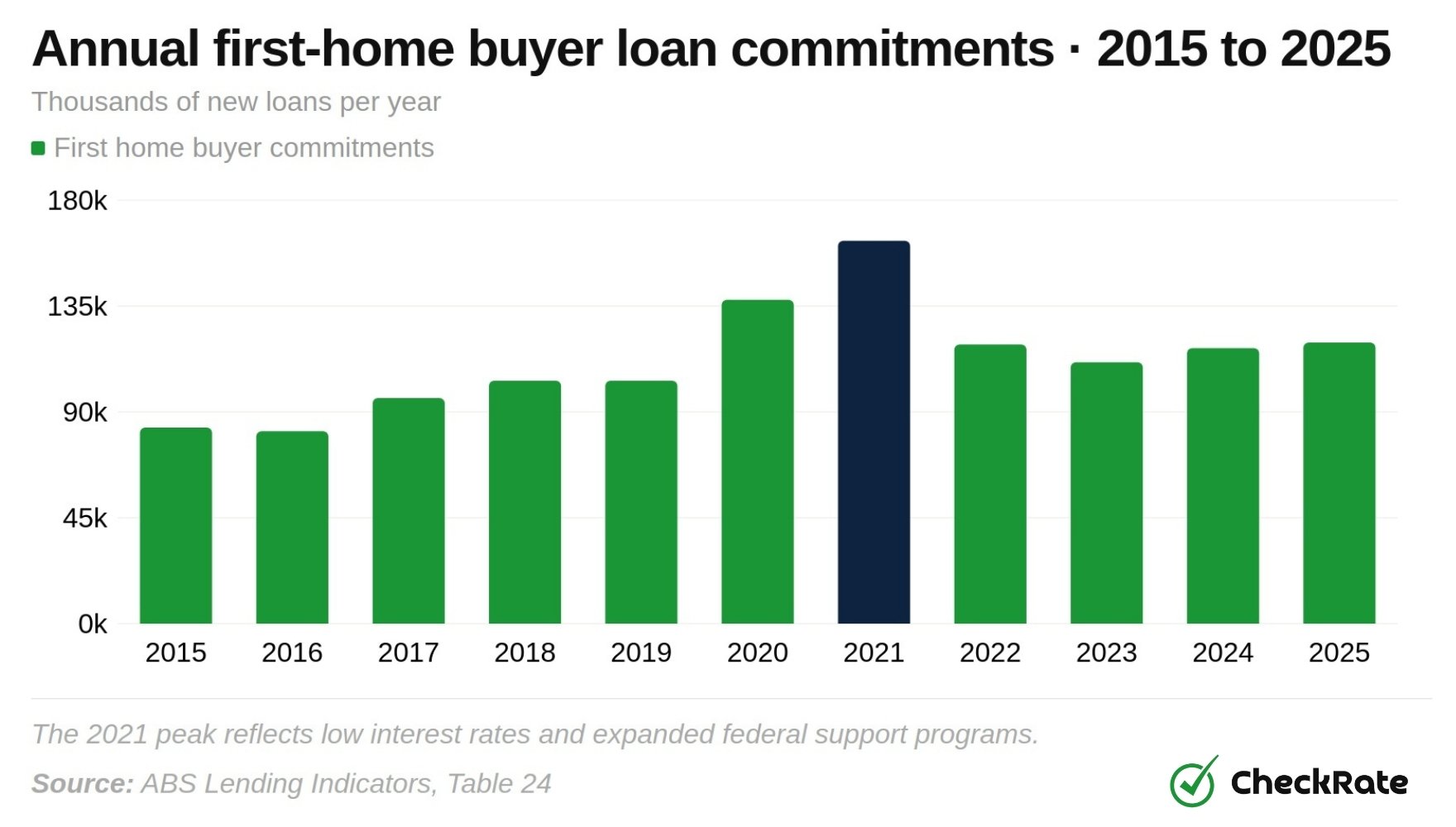

First-home buyer activity rebounds after the 2021 peak

More than 119,000 Australians took out their first home loan in 2025, up from 83,441 a decade earlier. The high point for the decade was 162,808 loans in 2021, when low interest rates and expanded government programs lifted activity to its highest level on record.

Annual first-home buyer loan numbers have moved with interest rates and government support. The Reserve Bank's run of rate rises pulled numbers back to 111,094 in 2023, the lowest point since 2016. Activity has lifted modestly since, reaching 119,464 in 2025.

The December 2025 quarter alone recorded 34,013 new commitments, the highest quarterly total since early 2022. Combined with the October 2025 expansion of the Home Guarantee Scheme, 2026 is likely to keep the recovery going.

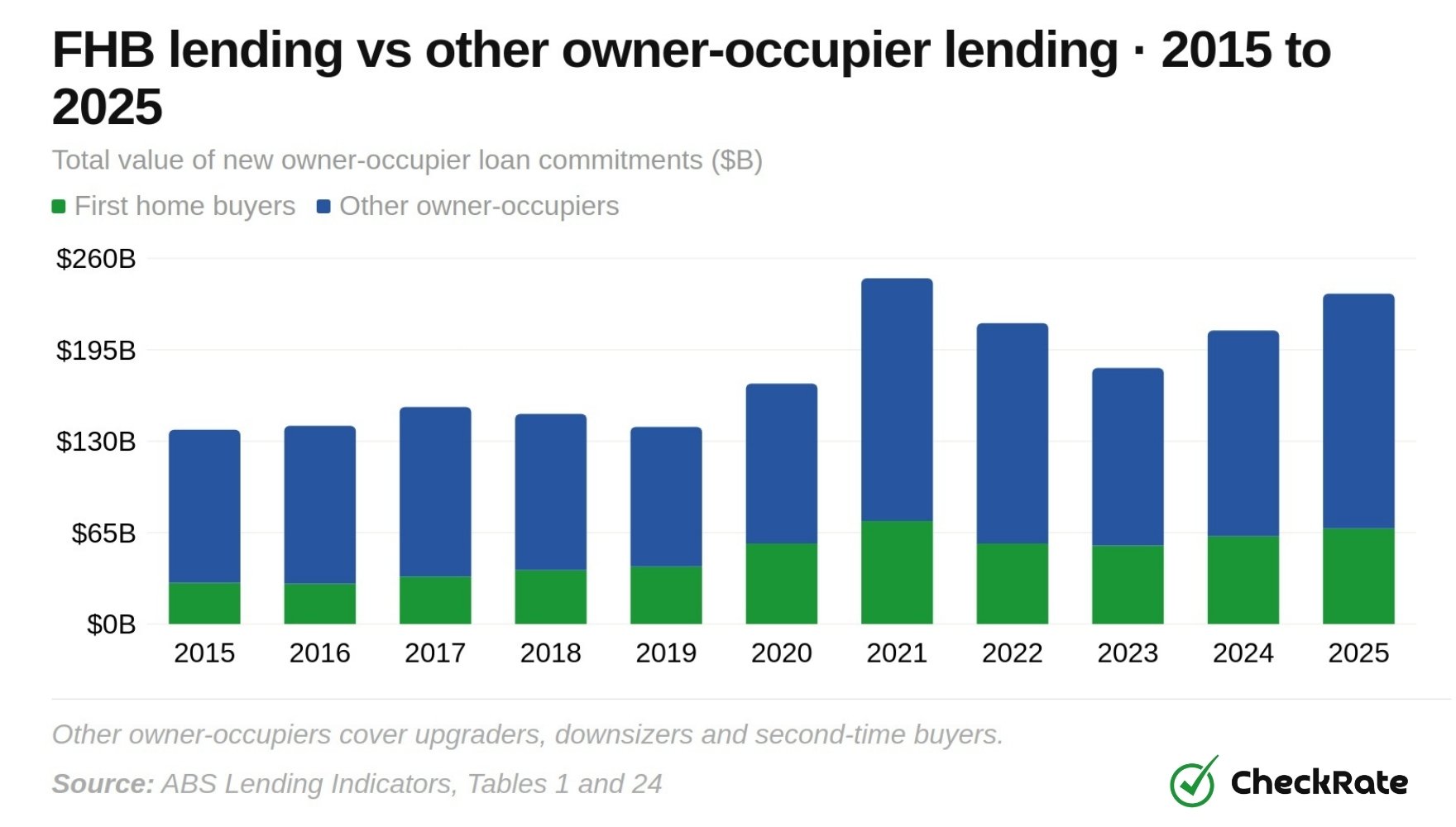

Value of first-home buyer lending over the decade

First-home buyers collectively put $67.9 billion into Australian property in 2025, more than double the $29.3 billion recorded in 2015. The all-time high of $73.3 billion was set in 2021 and has not yet been reclaimed.

The dollar value of first-home buyer lending has grown far faster than the number of buyers. While loan counts rose 43% over the decade, the total value of commitments more than doubled, driven almost entirely by rising property prices pushing loan sizes higher.

First-home buyers now make up one in three home loans

Roughly one in three owner-occupier home loans now goes to a first-home buyer. That share stood at 35.3% by number and 28.9% by value in 2025, both holding steady after peaking during the 2020 government support period.

Both measures peaked in 2020, when first-home buyers took 39.9% of loans by number and 33.5% by value. Both shares have settled in the mid-30s by number and high-20s by value since 2023.

Average first-home buyer loan size: how much are buyers borrowing?

$569,000 is what the average first-home buyer borrowed in 2025, compared to $351,000 ten years earlier. Loan sizes range from around $445,000 in Tasmania to $652,000 in New South Wales.

The average held near $350,000 from 2015 to 2017, rose through the 2018 to 2021 price cycle, and has kept climbing even as the number of loans eased back from the 2021 peak.

State by state: where first-home buyer activity is strongest

Victoria leads the country with 39,617 first-home buyer loans in 2025, ahead of New South Wales (28,340) and Queensland (23,045). These three states account for more than three in four loans nationally, though NSW buyers borrow the most on average at $652,000.

A first-home buyer in NSW borrows an average of $117,000 more than one in Victoria, and around $205,000 more than one in Tasmania.

| State | FHB loans | Total value | Average loan |

|---|---|---|---|

|

NSW

Highest average loan size

|

28,340 | $18.48B | $651,941 |

|

VIC

Highest loan count nationally

|

39,617 | $21.21B | $535,346 |

|

QLD

Second-largest average loan

|

23,045 | $13.20B | $572,945 |

|

WA

Activity up since 2022

|

14,496 | $7.80B | $538,356 |

|

SA

Stamp duty abolished for new builds 2024

|

7,323 | $3.92B | $534,617 |

|

ACT

Income-tested concession model

|

3,320 | $1.83B | $550,904 |

|

TAS

Smallest average loan size

|

2,321 | $1.03B | $445,067 |

|

NT

$50k FHOG — largest grant nationally

|

1,002 | $0.45B | $449,102 |

What government support is available to first-home buyers?

There are five main ways the Australian government supports first-home buyers, including the Home Guarantee Scheme, Help to Buy, the First Home Super Saver Scheme, the First Home Owner Grant, and stamp duty concessions. The Productivity Commission estimates that state duty concession spending alone exceeded $1.6 billion in 2023-24, up 20% from the previous year.

| Mechanism | Administered by | What it does |

|---|---|---|

|

Home Guarantee Scheme

HGS: First Home Guarantee + Family Home Guarantee

|

Federal · Housing Australia | Federal guarantee replaces LMI for deposits as low as 2-5% |

|

Help to Buy

Shared equity — launching late 2025

|

Federal | Government takes up to 40% equity in a new home, 30% existing |

|

First Home Super Saver

Tax-advantaged savings via superannuation

|

Federal · ATO | Up to $50,000 of voluntary contributions at concessional tax rates |

|

First Home Owner Grant

Restricted to new builds in most states

|

State-administered | Cash grant from $10k to $50k depending on state |

|

Stamp duty concessions

Largest form of assistance nationally

|

State-administered | Full or partial exemption from transfer duty to state thresholds |

State transfer duty concessions remain the largest single form of financial help in dollar terms. NSW saved 82,174 first-home buyers a combined $1.7 billion in the twelve months after its July 2023 threshold expansion. Victoria processed 42,208 duty concession payments worth $825.6 million in 2024-25. Queensland lifted its full-exemption threshold from $500,000 to $700,000 in 2024, giving buyers a maximum saving of $17,350.

New builds or existing homes: where are first-home buyers buying?

National ABS data does not separate first-home buyer loans by property type. The clearest signal available is that every mainland state now restricts its First Home Owner Grant to new builds only, pointing to a deliberate policy push toward new construction over existing stock.

Restricting grants to new builds is designed to turn buyer cash into actual construction, targeting what the Productivity Commission identifies as a long-term shortage of homes.

| State / territory | Grant amount | Eligibility |

|---|---|---|

|

Northern Territory

Most generous direct cash grant

|

$50,000 | New builds |

|

Queensland

Temporarily doubled to support construction

|

$30,000 | New builds only |

|

South Australia

Combined with full stamp duty abolition

|

$15,000 | New builds only |

|

NSW, VIC, WA, TAS

Rely more heavily on stamp duty concessions

|

$10,000 | New builds only |

|

ACT

Income-tested concession instead of a grant

|

N/A | Concession only |

How many first-home buyers used a government scheme in 2024-25?

The Home Guarantee Scheme supported 46,022 first-home buyers in 2024-25, filling 92% of available places. A further 18,300 made withdrawals through the First Home Super Saver Scheme, with a total of $364.4 million released that year.

| Year | HGS places available | HGS places taken | Take-up rate | FHSS releases | FHSS paid |

|---|---|---|---|---|---|

| 2018-19 | N/A | N/A | N/A | 4,200 | $50.8M |

| 2019-20 | 10,000 | approx. 10,000 | 100% | N/A | N/A |

| 2020-21 | 20,000 | 19,416 | 97% | 12,100 | $171.5M |

| 2021-22 | 20,000+ | 24,500 | N/A | 12,500 | $170.4M |

| 2022-23 | 50,000 | 32,500 | 65% | 13,300 | $203.8M |

| 2023-24 | 50,000 | 43,800 | 87% | 16,800 | $312.7M |

| 2024-25 | 50,000 | 46,022 | 92% | 18,300 | $364.4M |

The low default rate suggests that for this group of buyers, the main barrier to homeownership was cash to pull a deposit together, not the ability to keep up with ongoing repayments. That finding is central to the government's decision to move the scheme to uncapped operation from October 2025.

First-home buyer stamp duty concessions by state

Victorian stamp duty concession volumes peaked at 53,980 payments in 2020-21 and stood at 42,208 in 2024-25. The total dollar value has kept climbing, reaching $825.6 million in 2024-25, because property prices have continued to rise.

| Year | Metro volume | Regional volume | Total payments | Value of assistance |

|---|---|---|---|---|

| 2013-14 | 18,089 | 4,924 | 23,013 | $133.0M |

| 2017-18 | 26,179 | 9,094 | 35,273 | $551.7M |

| 2020-21 | 38,285 | 15,695 | 53,980 | $885.0M |

| 2022-23 | 27,716 | 8,602 | 36,318 | $665.6M |

| 2023-24 | 32,849 | 8,944 | 41,793 | $798.1M |

| 2024-25 | 32,564 | 9,644 | 42,208 | $825.6M |

Who is buying a first home in Australia?

Today's typical first-home buyer is under 35, relies on two incomes, and is increasingly leaning on a federal guarantee or family help to cover the deposit. In 2024-25, 17% received financial support from their parents, up from 11% in 2022. More than half of Home Guarantee Scheme users say they would have needed at least two extra years to save without it.

Age trends: more buyers under 30 than ever before

In 2022-23, more than 50% of scheme participants were under 30, up from 33% in 2019-20. The 18 to 24 cohort alone climbed from 3% of scheme users to 14% over the same period.

Key workers and single parents using the Home Guarantee Scheme

According to Housing Australia, more than 45,000 key workers have used the HGS since it launched, including 11,300 in 2023-24 alone. Nurses made up 35% of participating key workers, teachers accounted for 34% and emergency services staff made up 11%. The Family Home Guarantee has a clear gender skew, with 82% of participants in 2023-24 being women, reflecting the financial gap that often follows separation.

Australia's housing split: owners, renters and mortgage holders

Australian households are almost evenly split between those paying off a mortgage, those who own outright, and renters. The 2021 Census put those shares at 35%, 31% and 31% respectively, a split that has shifted over decades as outright ownership has fallen from 41% in 1996.

Shared equity arrangements have historically been a very small part of the market, though the federal Help to Buy scheme and existing state programs are set to expand that category from 2026 onwards.

| Tenure | Share of households | Approx. households |

|---|---|---|

|

Mortgaged

Owner-occupier still paying off a home loan

|

approx. 35% | approx. 3.8M |

|

Owned outright

Down from 41% in 1996

|

approx. 31% | approx. 3.4M |

|

Renting

Private and public rental combined

|

approx. 31% | approx. 3.4M |

|

Other / not stated

Includes shared equity, boarding, life tenure

|

approx. 3% | approx. 0.3M |

The long-run decline in outright ownership is arguably the biggest shift in the data. Where previous generations typically paid off a mortgage and entered retirement debt-free, the median outstanding mortgage balance in retirement-age households has roughly tripled in inflation-adjusted terms over the past twenty years.

- ABS Lending Indicators, Table 1: Households, housing finance, new loan commitments by property purpose, values

- ABS Lending Indicators, Table 4: Owner-occupiers, total dwellings excluding refinancing, by state, number and value

- ABS Lending Indicators, Table 24: First-home buyers, owner-occupiers, by state, new loan commitments, number and value

- Housing Australia Annual Report 2024-25: Home Guarantee Scheme places, arrears data, active portfolio and demographic splits

- ATO First Home Super Saver Scheme Data: Release requests, total payments, age and location breakdowns

- State Revenue Office Victoria: First-home buyer stamp duty concession payments, metro and regional volumes

- Revenue NSW: First Home Buyer Assistance Scheme take-up and compliance data

- Queensland Revenue Office: First Home Concession and First Home Owner Grant statistics

- RevenueSA: Stamp duty relief figures for new-build first home buyers

- State Revenue Office, Tasmania: First Home Owner Grant applications and payments

- Productivity Commission: Housing affordability, deposit hurdle analysis and state duty concession expenditure

- ABS Census 2021: Household tenure, housing occupancy and costs

Data Snapshots