Is it cheaper to rent or buy a house in Australia?

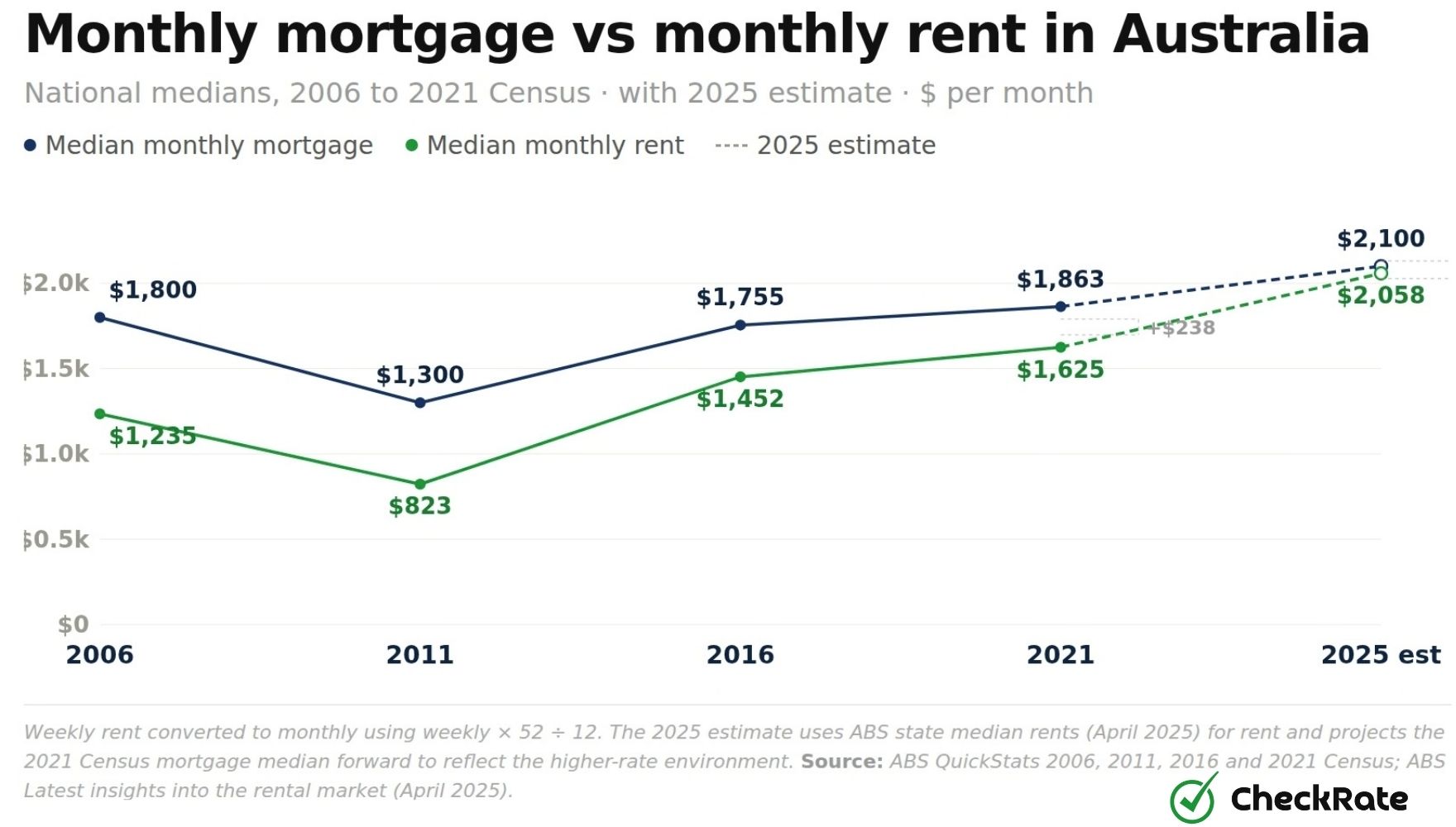

On the latest official national housing-cost data, renting costs $114 a week less than paying a mortgage. In the 2019–20 ABS Housing Occupancy and Costs survey, mortgage households paid an average of $493 a week, compared with $379 a week for renter households.

The cash-flow gap is likely wider for many new buyers in 2026, because mortgage rates and dwelling prices have risen since the latest national survey period. But cash flow is only one part of the rent-vs-buy comparison. Renters do not build equity, do not benefit from property capital growth, and are more likely than mortgage holders to be in housing stress.

- Median monthly mortgage

- Median monthly rent

Since the 2019–20 survey period, higher rates and dwelling prices have increased modelled repayment costs for many new buyers. The average rate on outstanding owner-occupier home loans climbed from 2.83% in 2021 to 6.03% in 2024, before easing to 5.73% by February 2026.

On a $700,000 loan over 30 years, that rate change lifts monthly repayments from around $2,870 to $4,070, an increase of about $1,200 a month before fees. State median weekly rents have also risen, with Western Australia up 75% since June 2018. But for new buyers, higher mortgage rates have added a larger dollar amount to repayments than rent increases in many markets.

Cash flow is not the only measure. Mortgage repayments include some equity build-up through principal repayments, while rent is fully expensed. Mortgage households also tend to earn more than renter households, which is why renting can look cheaper in dollar terms but heavier as a share of income.

At the 2021 Census, 32.2% of renting households paid more than 30% of gross income on rent, equal to 915,317 households. Among mortgage households, the equivalent share was 14.5%. Renters were therefore more than twice as likely to sit above the standard housing-stress threshold.

Two factors are not captured by the cash-flow comparison:

- Capital growth belongs to the property owner, and

- Principal repayments can build equity over time.

The cash-flow test measures short-term payment differences. It does not measure long-term wealth outcomes.

What is the average weekly housing cost for mortgage holders in Australia?+

Mortgage households paid an average of $493 a week nationally in 2019-20. By state and territory:

- NSW: $574

- ACT: $546

- NT: $534

- VIC: $501

- QLD: $447

- WA: $443

- SA: $390

- TAS: $346

Costs include mortgage repayments, council rates, water rates and body corporate fees. As a share of gross household income, mortgage households paid 16% on housing costs nationally, compared to 20% for private renters.

How much more does a mortgage cost than rent in Australia per year?+

Nationally, the annual gap was about $5,928 in 2019–20, based on a $114 weekly difference. City-level figures from the 2021 Census show:

- Greater Darwin: $5,180

- Sydney and Perth: $4,684

- Melbourne: $3,720

- Brisbane: $2,596

- Adelaide: $2,104

- Canberra: $1,560

- Hobart: $4 (essentially at parity)

Why can renting cost less in cash while buying builds equity?+

Cash flow and long-term wealth are different measures. Mortgage repayments can include both interest and principal, with the principal portion building equity over time. Rent payments do not create property equity. Owners may also benefit from capital growth, although this depends on the property, market conditions and holding period.

Rent vs mortgage gap by Australian capital city

In the 2021 Census, Perth and Darwin had the highest mortgage-to-rent ratios among Australian capitals, at 1.26 times annualised rent. That means median mortgage repayments were about 26% higher than median rent on the cash-flow measure.

In every capital city, annualised median rent was lower than median mortgage repayments, although the size of the gap varied:

- Sydney: 1.19 times

- Melbourne: 1.18 times

- Brisbane and Adelaide: 1.13 times

- Canberra: 1.07 times

- Hobart: at parity, with rent and mortgage figures within a few dollars

In dollar terms, Greater Sydney's median mortgage repayment was $2,427 a month, compared with median rent of $470 a week. Annualised, that left a $4,684 gap in favour of renting.

- Annualised mortgage

- Annualised rent

Using the December 2025 Sydney mean dwelling price of $1,301,100, a 20% deposit, the February 2026 average new owner-occupier rate of 5.72%, and a 30-year P&I loan, the modelled monthly repayment is $6,051 — around 2.5× the 2021 Census Sydney median of $2,427.

How the rent-vs-mortgage gap has changed since 2011

The mortgage-to-rent gap narrowed in every Australian capital across the last three Censuses. The average capital-city mortgage-to-rent ratio fell from 1.40 in 2011 to 1.22 in 2016, then to 1.15 in 2021.

Greater Hobart recorded the largest shift, falling from 1.40 in 2011 to 1.00 in 2021. Sydney's annual gap fell by 40%, from $7,752 in 2011 to $4,684 in 2021.

- Sydney

- Melbourne

- Brisbane

- Adelaide

- Perth

- Hobart

- Darwin

- Canberra

Why did the rent-vs-mortgage gap narrow?

The gap narrowed because median rents increased faster than median mortgage repayments between the 2011 and 2021 Censuses. Across the decade: Hobart rent +49% vs mortgage +6%; Adelaide rent +28% vs mortgage +1%; Sydney rent +34% vs mortgage +12%. In Brisbane, Perth, Darwin and Canberra, median mortgage repayments fell slightly while rents continued to rise.

- Rent growth

- Mortgage growth

Which Australian capital is the most balanced for rent vs buy?+

Greater Hobart was the most balanced capital city in the 2021 Census. Median annualised mortgage repayments were $18,204 against $18,200 in annualised median rent — a ratio of 1.00. Every other capital still favoured renting on cash flow.

Are 2021 Census mortgage figures still relevant in 2026?+

The 2021 Census mortgage figures are useful as a historical benchmark, but they are not a current new-buyer repayment estimate. Census medians cover all existing borrowers, including households with older loans taken out at lower rates. A 2026 buyer at Sydney's mean dwelling price faces a modelled monthly repayment of around $6,051 — about 2.5 times the 2021 Census Sydney median.

How have interest rates changed the rent-vs-buy comparison?

Average mortgage rates more than doubled in three years, climbing from 2.83% on outstanding owner-occupier loans in 2021 to a peak of 6.03% in 2024. Rates have since eased to 5.62% across the first two months of 2026, but they remain well above pre-2022 levels.

New borrowing tells a similar story. Owner-occupiers taking out new loans in Feb 2026 paid an average of 5.72%, well above the 2.78% annual average paid by buyers across 2021. On a $700,000 loan over 30 years, that gap adds roughly $1,200 a month in repayments before fees.

- Outstanding loans

- New loans funded

Rate moves of that scale coincided with a sharp fall in lending activity. Total new home loan commitments hit a record 628,520 in 2021, dropped to 465,432 by 2023, and recovered to 556,092 in 2025 — still 12% below the 2021 peak. First-home buyer commitments finished 2025 at 119,464, against the 2020 stimulus peak of 137,720.

The takeaway: the cash gap measured in 2019–20 is likely wider for many new buyers in 2026. Even with rates pulling back from the 2024 peak, owner-occupier servicing costs in 2026 still sit well above the levels in the latest official like-for-like comparison.

How much have rate rises added to mortgage repayments since 2021?+

On a $700,000 loan over 30 years, the move from a 2.83% rate in 2021 to 5.73% in Feb 2026 lifted monthly repayments from around $2,879 to $4,076, a $1,197 increase, or about $14,400 per year. On a $1 million loan, the equivalent rate move adds around $1,710 a month.

Have mortgage rates fallen from their 2024 peak?+

Yes. Owner-occupier outstanding rates eased from a peak of around 6.11% in mid-2024 to 5.73% in Feb 2026. The annual average across the first two months of 2026 was 5.62%.

How much cash is needed upfront to buy a house in Australia?

A 20% deposit purchase in NSW requires an estimated $316,570 in cash to settle. That breaks down as a $260,220 deposit, around $53,600 in transfer duty, and about $2,750 in registration, conveyancing and inspection fees. The deposit becomes equity, while transfer duty and purchase fees are upfront transaction costs.

By state, the estimated transfer-duty cost on the mean dwelling looks like this:

- ACT: around $57,500 on a $973,800 mean dwelling, the steepest non-FHB load relative to price

- NSW: around $53,600, second on raw duty dollars

- VIC: around $51,100

- TAS and NT have the lowest duty load, around $27,000 and $29,000 respectively

Note: Stamp duty figures use standard non-first-home-buyer transfer-duty schedules applied to the ABS state mean dwelling price. They exclude first-home buyer concessions, pensioner concessions, lenders mortgage insurance, and property-specific costs. Fees are estimated at $2,750. Monthly repayment uses the February 2026 average new owner-occupier rate of 5.72% over a 30-year P&I term.

A 5% deposit cuts the deposit cash, but it does not cut the duty. A NSW buyer using a 5% deposit still needs around $121,400 in cash to settle, plus lenders mortgage insurance on top. A renter in the same scenario can typically move in with a four-week bond and one or two weeks of rent in advance.

How much deposit do you need to buy a house in Australia?+

A standard 20% deposit on the Dec 2025 mean dwelling price ranges from $116,000 in the Northern Territory to $260,220 in NSW. The national mean dwelling was $1,074,700, which means a $214,940 deposit at 20%.

How much is stamp duty in Australia by state?+

- ACT: around $57,500 (highest)

- NSW: around $53,600

- VIC: around $51,100

- SA: around $45,400

- WA: around $43,350

- QLD: around $41,800

- NT: around $28,700

- TAS: around $26,900 (lowest)

How much have rents increased in Australia since 2018?

Annual rent inflation peaked at 7.8% in Aug 2023 and eased to 3.8% by Feb 2026, less than half the peak rate. Renting has lower cash-flow costs than buying, but rent is not a fixed cost. Dollar levels sit well above the 2018 baseline in every state.

State median weekly rents grew between June 2018 and April 2025 as follows: WA +75% ($350→$613), TAS +59%, SA +55%, QLD +47%, VIC +39%, NSW +33%, NT +24%.

- Rent growth

Why have rents risen so much in Western Australia?+

Western Australia has had the largest rent rise of any state, with 75% growth from June 2018 to April 2025. The state median climbed from $350 to $613 a week. Perth-driven housing inflation also showed the highest annual reading among capital cities in early 2026, at 14.8% in Feb 2026. WA's rapid rent growth may reflect strong population inflows and tight rental supply.

Are renters or mortgage holders under more housing stress?

32.2% of renting households were in housing stress against just 14.5% of mortgage households at the 2021 Census, making renters more than twice as likely to spend over 30% of gross household income on housing. In total, 915,317 renter households nationally sat above this threshold.

- Mortgage stress

- Rent stress

The difference reflects the different income profiles of renter and mortgage households. Mortgage holders paid 16% of gross income on housing costs in 2019–20, while renters paid 20%. Among lower-income renters, 58% of private-renter households in the bottom income bracket were already spending more than 30% of gross income on rent in 2019–20.

On the cash-flow measures used in this article, renting costs less than mortgage holding. But the income-share comparison points in the other direction. Renters pay less in dollars, but more as a share of income — and rent payments do not build property equity.

Are renters or mortgage holders under more housing-cost pressure in Australia?+

- On dollar costs: mortgage holders pay more, with a $114-a-week gap (2019-20).

- On affordability share: renters paid a higher share of income, at 20% vs 16% for mortgage households.

- On housing stress: the gap was wider, with 32.2% of renters in stress vs 14.5% of mortgage households at the 2021 Census.

How many Australian renters are in housing stress?+

At the 2021 Census, 915,317 renting households (32.2%) paid more than 30% of gross income on rent. By state, the share ranged from 16.3% in the Northern Territory to 35.5% in NSW.

Rent vs buy calculator: compare cash costs by state, deposit and holding period

On the default settings (NSW, 20% deposit, seven-year holding period and 5.72% mortgage rate), buying costs around $580,000 more in cash than renting over seven years. Most of the gap comes from upfront deposit, duty and fee costs that do not apply to renting. On running cash flow alone, renters pay about $37,772 less a year.

- Cumulative cash to buy

- Cumulative cash to rent

References

- ABS Housing Occupancy and Costs, 2019-20 financial year: Mean weekly housing costs and housing-cost-to-income ratios by state, tenure and landlord type, released 25 May 2022.

- ABS 2021 Census of Population and Housing, All persons QuickStats: Median monthly mortgage repayments and median weekly rent by Greater Capital City Statistical Areas and nationally; MAID and RAID indicators.

- ABS Total Value of Dwellings, December Quarter 2025: Mean dwelling price by state and territory, released 10 March 2026.

- RBA Lenders' Interest Rates (Table F6): Average outstanding and new owner-occupier housing loan rates, February 2026 monthly series.

- ABS Lending Indicators: December Quarter 2025: Number and value of new home loan commitments, annual totals 2005 to 2025.

- ABS Consumer Price Index, Australia, February 2026: Rents component, monthly and annual movement, released 25 March 2026.

- ABS Latest insights into the rental market: Median weekly rent by state and territory, June 2018 to April 2025, released 28 May 2025.

- State and territory revenue offices (transfer duty schedules): Standard non-FHB transfer-duty schedules in force during 2025 to 2026.

- Methodology: Stamp duty figures are applied to ABS state mean dwelling prices (Dec qtr 2025). Estimated cash to settle adds standard fees of $2,750. Calculator monthly repayments use a 30-year P&I loan at the user-set rate. Annual rent uses the estimated Feb 2026 state median (April 2025 ABS median uplifted by national CPI rents to Feb 2026).

Data Snapshots