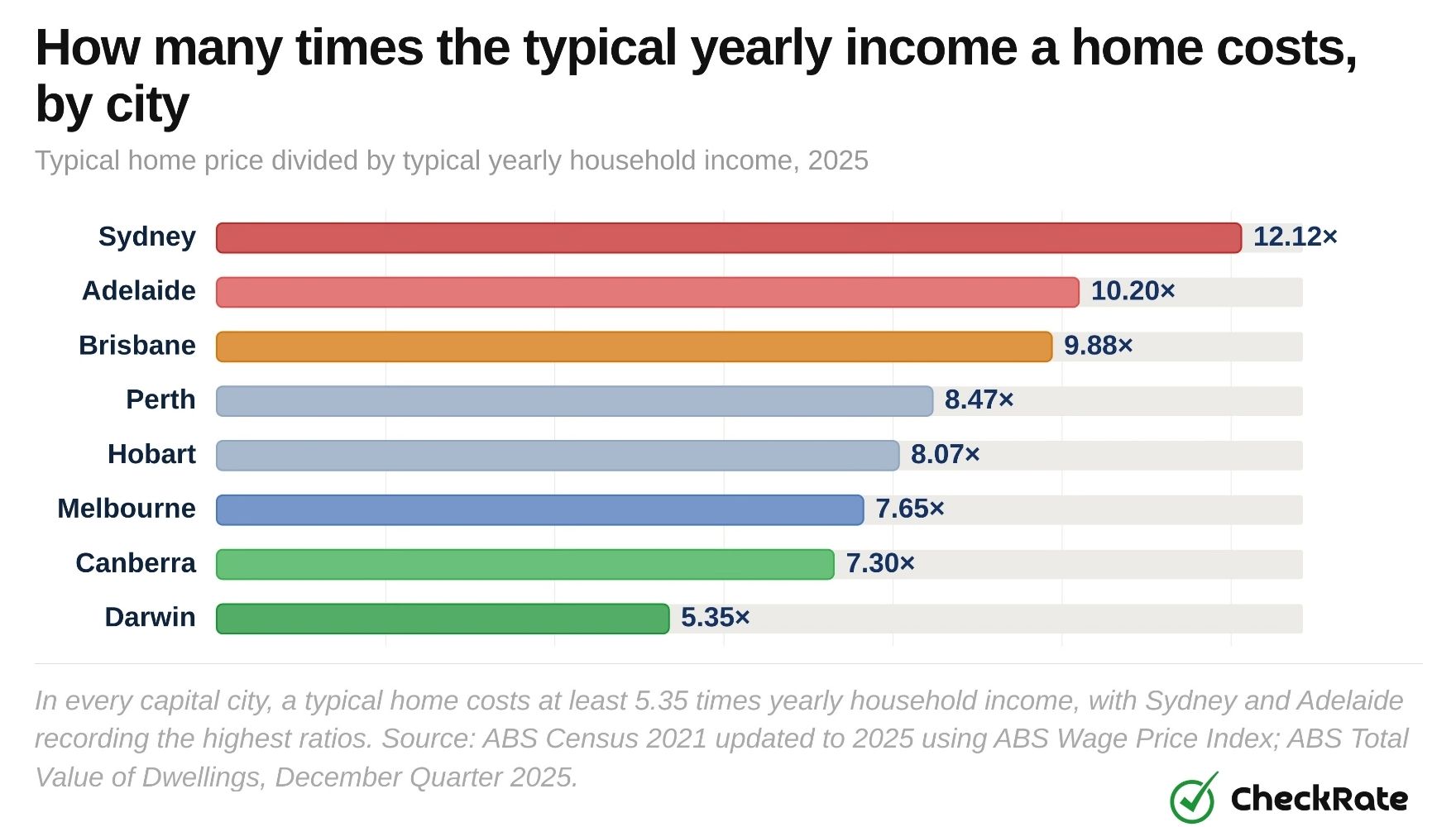

How do home prices compare with income by capital city?

Housing affordability can be compared by looking at what homes cost relative to what local households earn. Dividing the typical home price by typical yearly household income gives a simple measure of how home prices compare across capital cities.

- In Sydney, a typical home costs 12.12 times yearly household income, the highest figure of any capital city.

- Darwin is the most affordable on this measure. A typical home there costs 5.35 times yearly household income, supported by lower home prices and higher local wages.

- Adelaide has the second-highest ratio at 10.20 times yearly household income, followed by Brisbane at 9.88, Perth at 8.47, Hobart at 8.07, Melbourne at 7.65 and Canberra at 7.30.

- Adelaide and Perth have almost the same home prices, at $950,000 and $951,000 respectively, but Adelaide households earn about $19,000 less per year. That income gap gives Adelaide a higher home price-to-income ratio.

- Canberra has the highest average household income of any capital at $142,842 a year, while its typical home price keeps the city at 7.30 times yearly household income.

| City | Typical home price | Typical annual household income | Years of income |

|---|---|---|---|

| Sydney | $1,515,000 | $125,024 | 12.12 |

| Adelaide | $950,000 | $93,181 | 10.20 |

| Brisbane | $1,100,000 | $111,300 | 9.88 |

| Perth | $951,000 | $112,263 | 8.47 |

| Hobart | $749,500 | $92,820 | 8.07 |

| Melbourne | $875,000 | $114,430 | 7.65 |

| Canberra | $1,042,500 | $142,842 | 7.30 |

| Darwin | $711,000 | $132,970 | 5.35 |

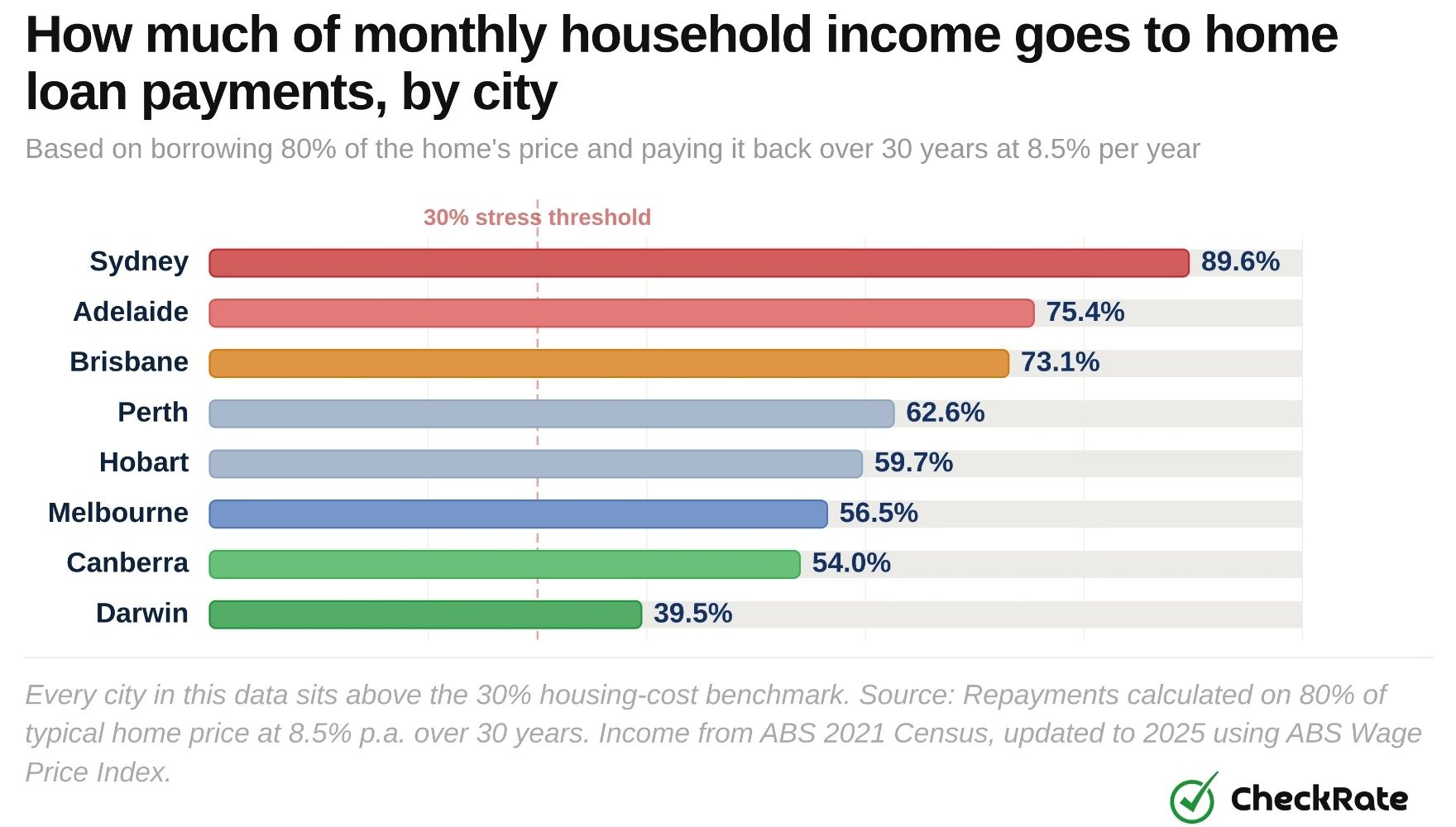

How much of income goes to home loan payments by capital city?

In every Australian capital city, estimated home loan payments take up more than 30% of typical monthly household income, based on the repayment assumptions used in this article. In Australia, spending more than 30% of income on housing costs is widely used as a benchmark for housing financial strain. In Sydney, estimated repayments reach nearly 90% of typical monthly household income. Darwin sits at the other end of the scale at 39.5%, mainly because typical home prices are lower.

| City | Amount borrowed | Monthly payment | Monthly pay | Share of pay | Above 30% benchmark? |

|---|---|---|---|---|---|

| Sydney | $1,212,000 | $9,336 | $10,419 | 89.6% | Yes |

| Adelaide | $760,000 | $5,855 | $7,765 | 75.4% | Yes |

| Brisbane | $880,000 | $6,779 | $9,275 | 73.1% | Yes |

| Perth | $760,800 | $5,861 | $9,355 | 62.6% | Yes |

| Hobart | $599,600 | $4,619 | $7,735 | 59.7% | Yes |

| Melbourne | $700,000 | $5,392 | $9,536 | 56.5% | Yes |

| Canberra | $834,000 | $6,425 | $11,903 | 54.0% | Yes |

| Darwin | $568,800 | $4,382 | $11,081 | 39.5% | Yes |

How long does it take to save a 20% deposit by city?

A 20% deposit takes 16 years to save in Sydney and 7 years in Darwin, based on a saving rate of 15% of typical yearly household income. The timeline varies significantly across Australia's capital cities, mainly because home prices and household incomes differ by location.

- In Sydney, a 20% deposit comes to $303,000, the largest of any capital. At a saving rate of 15% of typical yearly household income, the timeline is 16.2 years.

- In Darwin, the same deposit is $142,200, less than half of Sydney's figure, and it takes only 7.1 years to save.

- Adelaide (13.6 years) and Brisbane (13.2 years) take the second and third longest of any capital, despite having similar or lower home prices than cities with shorter timelines.

- Canberra has the highest typical household income of any capital city, which brings its timeline down to 9.7 years, even though the deposit there is $208,500.

- Melbourne, Hobart, and Perth sit close together, all between 10.2 and 11.3 years.

| City | 20% deposit needed | Saved per year (15% of income) | Years to save |

|---|---|---|---|

| Sydney | $303,000 | $18,754 | 16.2 years |

| Adelaide | $190,000 | $13,977 | 13.6 years |

| Brisbane | $220,000 | $16,695 | 13.2 years |

| Perth | $190,200 | $16,839 | 11.3 years |

| Hobart | $149,900 | $13,923 | 10.8 years |

| Melbourne | $175,000 | $17,164 | 10.2 years |

| Canberra | $208,500 | $21,426 | 9.7 years |

| Darwin | $142,200 | $19,945 | 7.1 years |

Darwin has the lowest typical home price of any capital city

Darwin is the only capital city where all three affordability measures rank lowest: home price-to-income ratio, estimated mortgage repayments as a share of income, and time to save a 20% deposit.

Canberra and Melbourne follow on most measures. Hobart's loan payments look low in dollar terms, but lower local household income means repayments still take up a relatively large share of income.

Which Australian capital city is least affordable?

Sydney is least affordable on all three measures: home price-to-income ratio, estimated repayments as a share of income, and time to save a 20% deposit. Adelaide is second least affordable on all three measures, even though its typical home price is almost identical to Perth's. In this comparison, the difference is mainly driven by household income.

Capital city affordability measures compared

The table below shows all three affordability measures for every capital city. Cities are ordered from least to most affordable by deposit saving timeline. Red shading indicates the three hardest cities to buy into; green indicates the two most affordable.

| City | Home price | 20% deposit | Annual saving | Years to save | Home/income | Monthly pay |

|---|---|---|---|---|---|---|

| Sydney | $1,515,000 | $303,000 | $18,754/yr | 16.2 yrs | 12.12× | 89.6% |

| Adelaide | $950,000 | $190,000 | $13,977/yr | 13.6 yrs | 10.20× | 75.4% |

| Brisbane | $1,100,000 | $220,000 | $16,695/yr | 13.2 yrs | 9.88× | 73.1% |

| Perth | $951,000 | $190,200 | $16,839/yr | 11.3 yrs | 8.47× | 62.6% |

| Hobart | $749,500 | $149,900 | $13,923/yr | 10.8 yrs | 8.07× | 59.7% |

| Melbourne | $875,000 | $175,000 | $17,164/yr | 10.2 yrs | 7.65× | 56.5% |

| Canberra | $1,042,500 | $208,500 | $21,426/yr | 9.7 yrs | 7.30× | 54.0% |

| Darwin | $711,000 | $142,200 | $19,945/yr | 7.1 yrs | 5.35× | 39.5% |

Why do affordability gaps differ between capital cities?

Adelaide and Perth show how income can change the affordability picture. Both cities have almost identical typical home prices, at $950,000 and $951,000 respectively. However, Perth has a lower home price-to-income ratio because typical household income is higher. Perth households earn about $19,000 more per year than Adelaide households, which lowers Perth's ratio on this measure.

Darwin also ranks most affordably because it combines the lowest typical home price of any capital city with higher typical household income than several larger capitals. Sydney sits at the other end of the table, with a typical home price equal to 12.12 times yearly household income.

Are regional areas more affordable than capital cities?

Regional areas can look more affordable than capital cities on price alone, but a lower price tag does not always tell the full story.

- Capital city home prices in this data range from $711,000 in Darwin to $1,515,000 in Sydney. Many regional towns sit well below this range, although prices vary widely by location.

- Regional areas often have lower wages, fewer jobs, and less access to services like hospitals, schools, and public transport. These trade-offs do not show up in a price-only comparison.

- Some regional areas, particularly those close to a capital city or in a mining area, also saw significant price rises between 2020 and 2025 and may not be as affordable as they appear.

- A broader affordability comparison includes both typical local home prices and typical local income. This gives a clearer measure than home prices alone.

Methodology

All figures are estimates based on publicly available data. They are designed to compare housing affordability across Australian capital cities and are not a prediction of what any individual buyer may experience.

- Household income: Typical household income for each capital city is based on the 2021 Census and updated to 2025 using ABS Wage Price Index data.

- Home prices: Typical capital city home prices are based on ABS Total Value of Dwellings, December Quarter 2025, Table 2: Median price and number of transfers, capital city and rest of state. Figures use December quarter 2025 median established house transfer prices for each capital city.

- Loan payments: Repayment estimates are based on borrowing 80% of the typical home price and repaying it over 30 years at 8.5% per year. The 8.5% rate is a research assumption and does not represent a live loan quote.

- Saving a deposit: Deposit-saving timelines are based on a 20% deposit and assume 15% of household income is saved each year, starting from zero, with no interest earned on savings.

- Housing-cost benchmark: The article uses the common 30% housing-cost benchmark to compare estimated repayments with household income. This benchmark does not assess individual borrowing capacity or personal financial circumstances.

References

- 1.Australian Bureau of Statistics (ABS), Income and work Census 2021: Typical weekly household income by capital city, used as the basis for 2025 income estimates.

- 2.ABS Wage Price Index Australia, Dec 2025: Official measure of wage growth. A factor of 1.1576 was applied to 2021 income figures to bring them up to 2025 levels.

- 3.ABS Total Value of Dwellings, Dec Quarter 2025: Table 2: Median price and number of transfers, capital city and rest of state. Used for December quarter 2025 median established house transfer prices by capital city.

- 4.Australian Institute of Health and Welfare (AIHW): Oct 2025: Definition of housing financial strain — spending more than 30% of income on housing costs.

Data Snapshots