Australian housing affordability has tightened to the point where a median-income household now needs almost half its income for repayments on a new mortgage. In 2025, that household needed to put 45.9% of its income toward repayments, while saving a 20% deposit took 11.2 years. In 2024–25, only 15% of home sales were affordable for a median-income household.

Key statistics, 2025–2026

45.9%

Share of median household income needed for repayments on a new mortgage in 2025, down from 50% in 2024 (NHSAC)

11.2 yrs

To save a 20% deposit at median household income in 2025; up from 10.6 years in 2024 (NHSAC)

$1.11m

National mean dwelling price in the March quarter of 2026, up 11.9% year-on-year (ABS)

5.92%

New owner-occupier P&I rate in April 2026. With APRA’s 3pp buffer, lenders assess at 8.92% (RBA, APRA)

Section 01Property price

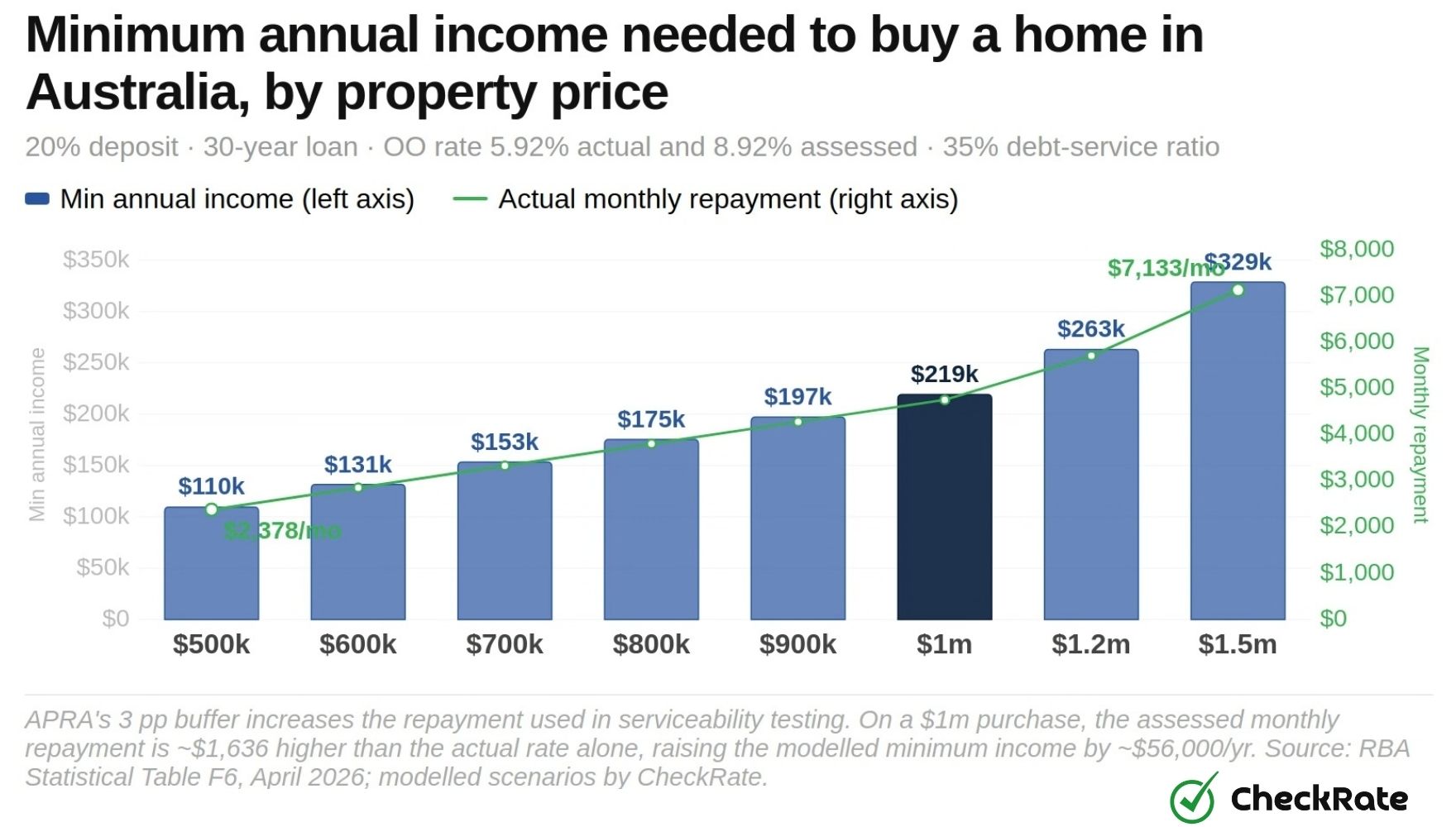

How much income is needed to buy a home in Australia by property price?

Property price has the biggest effect on the income needed to buy a home, because a higher purchase price increases both the loan size and the assessed repayment.

At the national mean dwelling price of $1,111,100 in March 2026, a single borrower would need an estimated minimum gross income of about $243,500 a year under this model, based on a 20% deposit. That is 2.5 times the national median full-time earnings of $98,124 and 2.3 times the mean full-time earnings of $106,657.

Even at a property price of $500,000, the estimated qualifying income is $109,600, which is above the national median full-time salary.

The figures are calculated scenarios using official inputs, including the RBA new owner-occupier P&I rate of 5.92% in April 2026, APRA’s 3 percentage point serviceability buffer, a 30-year loan term and a 20% deposit. The serviceability buffer gives an assessment rate of 8.92% for owner-occupier loans.

Minimum income is calculated as the gross annual salary at which assessed repayments equal 35% of gross income. These figures are modelled estimates, not official income thresholds or lender approval amounts.

About the data: All calculated figures in this article use the RBA new owner-occupier P&I rate of 5.92% in April 2026 and the new investor P&I rate of 6.09% in April 2026. APRA’s confirmed 3 percentage point serviceability buffer gives assessment rates of 8.92% for owner-occupier loans and 9.09% for investor loans. The modelling assumes a 30-year P&I loan term, a 20% deposit and a debt-service ratio of 35% of gross income. These are calculated scenarios, not published official income thresholds.

Minimum income and repayments by property price

20% deposit, 30-year P&I loan, OO rate 5.92% actual / 8.92% assessed, 35% debt-service ratio, April 2026

| Property price |

Loan (20% dep) |

Actual monthly |

Assessed monthly |

Min annual income |

| $500,000 |

$400,000 |

$2,378 |

$3,195 |

$109,600 |

| $600,000 |

$480,000 |

$2,853 |

$3,835 |

$131,500 |

| $700,000 |

$560,000 |

$3,329 |

$4,474 |

$153,400 |

| $800,000 |

$640,000 |

$3,804 |

$5,113 |

$175,300 |

| $900,000 |

$720,000 |

$4,280 |

$5,752 |

$197,200 |

| $1,000,000 |

$800,000 |

$4,755 |

$6,391 |

$219,100 |

| $1,200,000 |

$960,000 |

$5,706 |

$7,669 |

$263,000 |

| $1,500,000 |

$1,200,000 |

$7,133 |

$9,586 |

$328,700 |

Calculated scenarios. 20% deposit, 30-year P&I loan, RBA new OO rate 5.92% (April 2026), APRA buffer 3pp (assessment rate 8.92%), 35% debt-service ratio. Figures rounded to the nearest $100.

Source: RBA Statistical Table F6, April 2026; APRA macroprudential settings update, May 2026.

Minimum annual income needed to buy a home in Australia, by property price

20% deposit, 30-year loan, OO rate 5.92% actual and 8.92% assessed, 35% debt-service ratio

- Min annual income

- Actual monthly repayment

APRA’s 3 percentage point buffer increases the repayment amount used in serviceability testing. On a $1 million purchase, the assessed monthly repayment is about $1,636 higher than the repayment calculated at the actual rate alone, raising the modelled minimum income by about $56,000 a year.

Source: Calculated scenarios using RBA Statistical Table F6, April 2026, and APRA’s 3 percentage point serviceability buffer.

These figures are modelled income estimates, not a guarantee of loan approval. Lenders also assess living expenses, existing debt, credit history, income stability and other borrower circumstances. A borrower with large credit card limits or personal loan debt may have lower borrowing capacity than the modelled figure suggests.

Why is the assessed rate higher than the actual rate?

APRA requires lenders to test mortgage serviceability at the loan’s interest rate plus 3 percentage points. At an actual rate of 5.92%, that means lenders assess a borrower’s ability to repay at 8.92%. APRA confirmed in May 2026 that this buffer would remain in place. The buffer reduces how much borrowing power can be supported by a given income, because repayments are tested at a higher rate than the actual loan rate. It applies whether interest rates are rising, falling or stable.

Section 02By city and state

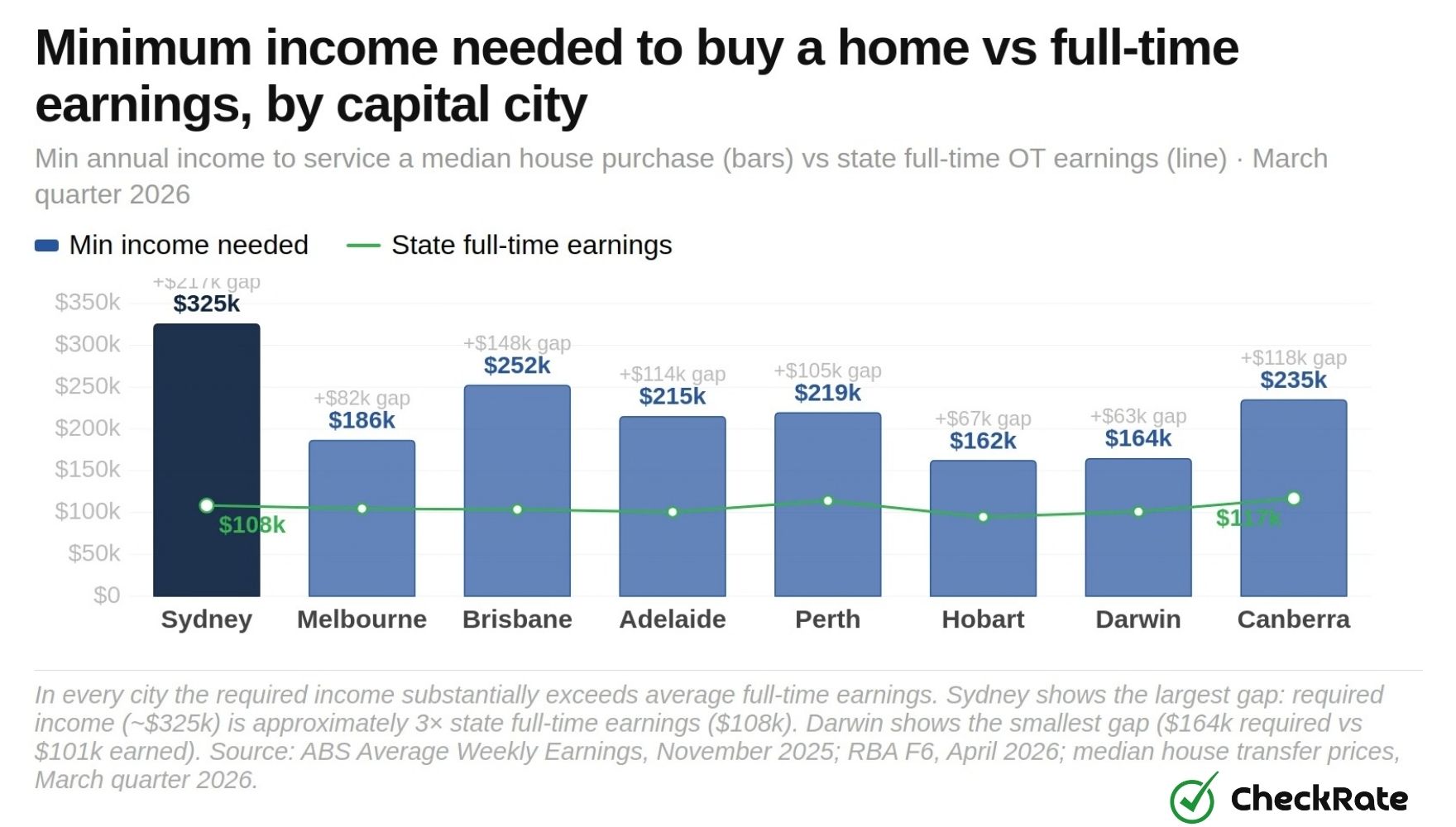

How much income is needed to buy a home in Australian capital cities?

Sydney’s median established house transfer price was $1,485,000 in the March quarter of 2026. This was 75% higher than Melbourne’s median of $850,000 and more than double Hobart’s median of $740,000.

Under this model, that price difference creates a wide gap in estimated income requirements. A single borrower would need an estimated minimum annual income of about $325,400 to service a median established house purchase in Sydney, compared with $162,100 in Hobart and $164,300 in Darwin.

Min annual income to service a median house, by capital city (2026)

Sydney

$325,400

median $1,485,000

Melbourne

$186,300

median $850,000

Brisbane

$252,000

median $1,150,000

Adelaide

$214,700

median $980,000

Perth

$219,100

median $1,000,000

Hobart

$162,100

median $740,000

Darwin

$164,300

median $750,000

Canberra

$234,700

median $1,071,300

Minimum income vs full-time earnings, by Australian capital city

Minimum annual income to service a median house purchase (bars) vs state full-time OT earnings (line), March quarter 2026

- Min income needed

- State FT earnings

Darwin shows the smallest gap between required income ($164,300) and state full-time earnings ($101,000). Sydney shows the largest: required income is approximately three times the state’s full-time earnings. In every city, the required income substantially exceeds what a single full-time worker on state average earnings receives.

Source: ABS Total Value of Dwellings, Table 2, March quarter 2026; ABS Average Weekly Earnings, November 2025.

At the state level, the gap between mean dwelling prices and full-time earnings is widest in New South Wales. Under this model, the minimum income needed to service the state’s mean dwelling price is $290,300, equal to 2.7 times the New South Wales full-time ordinary-time earnings figure of $108,368.

The Northern Territory has the narrowest gap, with a modelled minimum income of $130,900 compared with full-time ordinary-time earnings of $100,999.

The state-level figures use mean dwelling prices and cover all dwelling types, including houses, units and townhouses. This differs from the capital-city comparison above, which uses median established house transfer prices.

Minimum income by state and territory

Mean dwelling price vs full-time earnings and modelled minimum qualifying income, 20% deposit, March quarter 2026

| State / territory |

Mean dwelling price |

FT adult OT earnings (annual) |

Min income (20% dep) |

| NSW |

$1,324,800 |

$108,368 |

$290,300 |

| Vic |

$947,100 |

$104,712 |

$207,600 |

| Qld |

$1,123,700 |

$103,714 |

$246,200 |

| SA |

$973,100 |

$100,625 |

$213,200 |

| WA |

$1,103,500 |

$114,046 |

$241,800 |

| Tas |

$750,300 |

$94,702 |

$164,400 |

| NT |

$597,300 |

$100,999 |

$130,900 |

| ACT |

$1,018,000 |

$116,917 |

$223,100 |

| Australia |

$1,111,100 |

$106,657 |

$243,500 |

State mean prices are ABS all-dwelling mean prices (houses, units, townhouses). Annual earnings = ABS weekly FT adult OT earnings × 52. Min income calculated at 8.92% assessment rate, 30-year loan, 35% DSR, 20% deposit.

Source: ABS Total Value of Dwellings, Table 1, March quarter 2026; ABS Average Weekly Earnings, November 2025.

Why state and capital-city housing affordability figures differ

The state mean dwelling prices in the table above cover all residential dwellings, including houses, units and townhouses. They are mean prices across each state’s residential dwelling stock. The capital-city figures use median established house transfer prices for homes that changed ownership during the quarter. The two series come from the same ABS release, but they measure different parts of the housing market and are not directly comparable. Victoria recorded the only quarterly state price decline in March 2026, at 0.3%, while Western Australia recorded the strongest quarterly rise, at 7.2%.

Section 03Single income vs dual income buyers

Can a single-income buyer afford a home in Australia?

A single borrower on the national median full-time income of $98,124 a year has modelled borrowing capacity of about $358,000, giving estimated purchasing power of about $448,000 with a 20% deposit. That is below the median established house transfer price in every capital city.

Two borrowers each earning the national median full-time income have combined modelled borrowing capacity of about $716,000, giving estimated purchasing power of about $896,000 with a 20% deposit. That is enough to reach Melbourne’s median established house transfer price, but remains below the median in Brisbane, Adelaide, Perth, Canberra and Sydney.

$448,000

Estimated purchasing power for a single borrower on the national median full-time income of $98,124 a year. Based on a modelled loan of $358,000, 8.92% assessment rate, 35% DSR.

$896,000

Estimated purchasing power for two borrowers each earning the national median full-time income, or $196,248/yr combined. Modelled loan of $716,000; above Melbourne’s median.

$590,000

Additional estimated purchasing power needed for two borrowers on the national median full-time income to reach Sydney’s median established house transfer price of $1,485,000.

Single and dual income buying power vs median house prices, capital cities

Max purchase price with 20% deposit, single or dual median FT income ($98,124/yr each), vs median established house transfer prices, March quarter 2026

Single income buying power of $448,000 falls below the median established house transfer price in all eight capital cities. Dual income buying power of $896,000 reaches Melbourne, but falls short of Brisbane ($1,150,000), Adelaide ($980,000), Perth ($1,000,000), Canberra ($1,071,300) and Sydney ($1,485,000).

Source: ABS Employee Earnings and Hours, May 2025; ABS Total Value of Dwellings, Table 2, March quarter 2026; RBA Table F6, April 2026; APRA, May 2026.

The increase in assessed mortgage rates has reduced modelled borrowing capacity for single-income buyers. When the RBA’s new owner-occupier rate was 2.42% in December 2021, the same single median income would have supported modelled borrowing capacity of about $509,000, giving estimated purchasing power of approximately $636,000 with a 20% deposit. That was enough to reach the median established house transfer prices in Darwin and Hobart, but still below Melbourne’s median. At the April 2026 assessment rate of 8.92%, the same income supports modelled borrowing capacity of about $358,000.

Home ownership among younger Australians has declined over decades

Home ownership among 25- to 34-year-olds fell from 61% in 1981 to 43% in NHSAC’s latest Census-based analysis. The income and borrowing gap facing single-income buyers sits alongside a longer-term decline in younger adult home ownership. First-home buyers remain active in the market. ABS Lending Indicators show 30,241 owner-occupier first-home buyer loan commitments in the March quarter of 2026, up 5.0% year-on-year.

Section 04Deposit size

How does deposit size change the income needed to buy a home?

At median household income, it now takes 11.2 years to save a 20% deposit, up from 10.6 years a year earlier. A smaller deposit increases the loan size, which also increases the income needed to meet the modelled repayment test.

On a $1,000,000 property, moving from a 5% deposit to a 20% deposit reduces the modelled minimum income requirement by about $41,000 a year. However, the larger deposit also requires an additional $150,000 upfront.

For deposits below 20%, Lenders Mortgage Insurance may also apply, depending on the lender, loan type and borrower circumstances.

Impact of deposit size on required income

$1,000,000 property — minimum qualifying income and repayments by deposit percentage, April 2026

| Deposit |

Deposit amount |

Loan |

Actual monthly |

Min annual income |

LMI |

| 5% |

$50,000 |

$950,000 |

$5,647 |

$260,200 |

Typically required |

| 10% |

$100,000 |

$900,000 |

$5,350 |

$246,500 |

Typically required |

| 15% |

$150,000 |

$850,000 |

$5,053 |

$232,800 |

Typically required |

| 20% |

$200,000 |

$800,000 |

$4,755 |

$219,100 |

Not required |

$1,000,000 property, 30-year P&I loan, OO rate 5.92% (April 2026), assessment rate 8.92%, 35% DSR. LMI is typically required for deposits below 20%; premiums vary by lender, LVR and insurer.

Source: RBA Statistical Table F6, April 2026; APRA macroprudential settings update, May 2026.

Lower rates reduce repayments but do not reduce the deposit hurdle

The mortgage servicing ratio fell from 50% to 45.9% between 2024 and 2025 as rates eased. Over the same period, the time needed to save a 20% deposit increased from 10.6 years to 11.2 years. Lower interest rates reduce modelled monthly repayments, but they do not reduce the property price used to calculate the deposit. This means deposit-saving time can increase even when repayment affordability improves.

Section 05How income requirements have changed

How interest rates and dwelling prices changed income requirements

Between December 2011 and December 2025, the national mean dwelling price rose from $486,900 to $1,088,800, an increase of 123.6%. Full-time adult ordinary-time earnings rose from $69,165 to $106,657 a year over the same period, an increase of 54.2%. This means national mean dwelling prices grew at about 2.3 times the pace of full-time earnings over those 14 years.

+123.6%

Growth in the national mean dwelling price between December 2011 and December 2025, from $486,900 to $1,088,800.

+54.2%

Growth in full-time adult ordinary-time earnings over the same period, from $69,165 to $106,657 a year.

2.3×

Rate at which national mean dwelling prices grew relative to full-time earnings between December 2011 and December 2025.

Australian dwelling price growth vs earnings growth, indexed to 2011

National mean dwelling prices and full-time adult OT earnings, indexed to 100 at December 2011

- Dwelling prices (indexed)

- Full-time earnings (indexed)

The dashed vertical line marks December 2021, when the RBA’s new OO P&I rate reached its cycle low of 2.42%. By December 2025, the price index stood at 224 against an earnings index of 154, a gap of 70 index points.

Source: ABS Total Value of Dwellings, Table 1; ABS Average Weekly Earnings time series.

The increase in mortgage rates added a second layer to the affordability gap. New owner-occupier P&I rates rose from 2.42% in December 2021 to 6.18% in December 2023, before easing to 5.42% by December 2025. After cash rate increases before April 2026, the RBA’s new owner-occupier P&I rate rose to 5.92% in April 2026.

Dec 2019

3.18%

Pre-pandemic

Dec 2023

6.18%

Cycle peak

Source: RBA Statistical Table F6, Lenders’ Interest Rates. New owner-occupier P&I loan rates. Selected months only.

New owner-occupier and investor P&I rates in Australia, 2019 to April 2026

Year-end readings plus April 2026 latest available rate point, RBA Statistical Table F6

- Owner-occupier P&I

- Investor P&I

Investor rates have consistently sat 15 to 35 basis points above owner-occupier rates. Before the April 2026 lending-rate point, the RBA raised the cash rate to 3.85% in February and 4.10% in March. Total new dwelling loan commitments fell 6.2% by number in the March quarter 2026.

Source: RBA Statistical Table F6, April 2026.

Section 06Beyond income

What do lenders assess beyond income?

For the national average owner-occupier loan of $735,000, APRA’s 3-percentage-point serviceability buffer increases the modelled assessed monthly repayment from $4,369 to $5,872, a difference of $1,503 per month. Income is only one part of mortgage serviceability. Lenders also assess living expenses, existing debt, credit history, income stability and other borrower circumstances. These factors can reduce borrowing capacity below what the income figure alone suggests.

+3pp

Serviceability buffer

Lenders must assess repayments at the loan’s interest rate plus at least 3 percentage points, unless APRA determines otherwise. At 5.92%, that means testing repayments at 8.92%. APRA confirmed in May 2026 that the mortgage serviceability buffer would remain at 3 percentage points.

Verified

Income verification

Lenders typically verify income using documents such as recent payslips, employer or accountant confirmation, tax assessment notices, tax returns and bank statements. Self-employed borrowers generally require more detailed income and cash-flow documentation.

−20%

Non-salary income discount

APRA’s guidance says prudent lenders apply discounts to temporarily high, uncertain or variable income. This can include overtime, bonuses, commissions, rental income and other non-salary income. APRA describes a discount of at least 20% as prudent practice for most types of non-salary income.

HEM

Living expenses benchmark

Living expenses are generally assessed using the greater of the borrower’s declared expenses or an appropriately scaled benchmark, such as the Household Expenditure Measure or Household Expenditure Index. This means declared expenses may not be the only figure used in serviceability testing.

3%/mo

Credit card assessment

APRA’s guidance says lenders may assess credit card or other revolving personal debt using a repayment rate of 3% a month on the total committed limit. A $20,000 credit card limit would count as $600 a month in assessed obligations, even if the balance is lower.

Multiple

Serviceability ratios

Lenders consider several serviceability measures, including income, existing debt commitments, stressed repayments and net income surplus after expenses. No single income figure determines loan approval.

Source: APRA Prudential Practice Guide APG 223, Residential Mortgage Lending; APRA macroprudential settings update, May 2026.

The result is that two borrowers on identical salaries may have different borrowing capacity outcomes. A borrower with $50,000 in credit card limits and a car loan may have lower borrowing capacity than one with no existing debts and a stable base salary, even if their gross income is the same.

What is the serviceability buffer and why does it matter?▾

Lenders must test repayments at the loan rate plus at least 3 percentage points, unless APRA determines otherwise. At 5.92%, that means testing repayments at 8.92%. On the national average owner-occupier loan of $735,000, the buffer adds $1,503 per month to the assessed repayment, reducing the borrowing capacity supported by the same income.

How is rental income assessed when applying for a mortgage?▾

Rental income may be counted toward serviceability, but APRA’s guidance says prudent lenders apply a discount to rental income before counting it. APRA describes a discount of at least 20% as prudent practice for most types of non-salary income. A property expected to generate $40,000 a year in rent would have $32,000 counted under that example. Lenders also account for property-related costs and should not rely on future tax benefits from negative gearing when assessing serviceability.

How are unused credit card limits assessed for mortgage serviceability?▾

APRA guidance says lenders may assess credit cards and revolving debt at 3% of the total committed limit per month, regardless of the current balance. A $20,000 credit card limit would count as $600 per month in assessed obligations, or about $7,200 a year, even if the card has not been used. This can reduce the modelled borrowing capacity supported by the borrower’s income.

Section 07Salary and borrowing examples

How much borrowing power do different salaries provide in Australia?

Even the highest state or territory full-time earnings figure, the ACT at $116,917 a year, gives a single borrower modelled purchasing power of about $534,000. That is below the median established house transfer price in every capital city.

A borrower on the national median full-time income of $98,124 has modelled purchasing power of about $448,000, while two borrowers each earning the national median full-time income have combined modelled purchasing power of about $896,000.

The four profiles below show how salary translates into modelled borrowing capacity under the article’s assumptions, including an 8.92% assessment rate, a 30-year loan term, a 20% deposit and a 35% debt-service ratio.

Median full-time worker

$448,000

Max buying power with 20% deposit

Annual income$98,124

Max loan (35% DSR)$358,000

Actual monthly repayment$2,129

Within reachBelow median in all capitals

Mean full-time adult (AWE)

$487,000

Max buying power with 20% deposit

Annual income$106,657

Max loan (35% DSR)$389,000

Actual monthly repayment$2,315

Within reachBelow median in all capitals

ACT full-time worker (highest)

$534,000

Max buying power with 20% deposit

Annual income$116,917

Max loan (35% DSR)$427,000

Actual monthly repayment$2,537

Within reachBelow median in all capitals

Dual median full-time income couple, combined $196,248/yr

$896,000

Max buying power with 20% deposit. Two borrowers each on ABS median FT income ($98,124/yr)

Max loan$716,000

Monthly repayment$4,259

ReachesMelbourne

Short ofBrisbane, Adelaide, Perth, Canberra, Sydney

About the data and modelling: Income inputs use ABS median full-time weekly earnings of $1,887 from Employee Earnings and Hours, May 2025; ABS mean full-time adult ordinary-time earnings of $2,051.10 a week from Average Weekly Earnings, November 2025; and ACT full-time ordinary-time earnings of $2,248.40 a week from Average Weekly Earnings, November 2025. Borrowing and purchasing-power estimates use an 8.92% assessment rate, a 30-year P&I loan term, a 35% debt-service ratio and a 20% deposit. Actual repayments are calculated at the 5.92% owner-occupier P&I rate.

Borrowing power by income level vs median established house prices, capital cities

Max purchase price with 20% deposit for each income profile vs median established house transfer prices, March quarter 2026

Even the highest-earning jurisdictional average (ACT at $116,917/yr) gives a single borrower buying power of $534,000, below the median house transfer price in every capital city. A dual-income couple on two national medians reaches $896,000, which covers Melbourne but falls short of Brisbane ($1,150,000), Canberra ($1,071,300), Perth ($1,000,000), Adelaide ($980,000) and Sydney ($1,485,000).

Source: ABS Employee Earnings and Hours (May 2025); ABS Average Weekly Earnings (Nov 2025); ABS Total Value of Dwellings Table 2 (Mar Q 2026); RBA Table F6 (Apr 2026); APRA, May 2026.

Section 08Borrowing power reduced

How much has modelled borrowing power changed since 2021?

At the December 2021 rate low of 2.42%, APRA’s 3 percentage point buffer gave an assessment rate of 5.42%. Under this model, a borrower on the national median full-time income had estimated borrowing capacity of about $509,000, giving modelled purchasing power of about $636,000 with a 20% deposit.

At the April 2026 assessment rate of 8.92%, the same income supports estimated borrowing capacity of about $358,000, with modelled purchasing power of about $448,000. That is a reduction of around $188,000 in modelled purchasing power from the same salary over four and a half years.

The table shows how modelled borrowing capacity changed as assessment rates moved over time. The maximum loan amount falls when the assessment rate rises, because serviceability is tested against the assessed repayment rather than the actual repayment. Even when actual rates eased in 2025, the assessment rate remained higher than in 2021, keeping modelled borrowing capacity below the earlier level.

Modelled borrowing power by rate period

National median full-time income ($98,124/yr) — max loan, buying power and repayments at each rate point, 35% DSR, 20% deposit

| Period |

Actual OO rate |

Assessment rate |

Max loan |

Buying power |

Actual monthly |

| Dec 2021 |

2.42% |

5.42% |

$509,000 |

$636,000 |

$1,988 |

| Dec 2022 |

4.95% |

7.95% |

$392,000 |

$490,000 |

$2,092 |

| Dec 2023 |

6.18% |

9.18% |

$350,000 |

$438,000 |

$2,139 |

| Dec 2025 |

5.42% |

8.42% |

$375,000 |

$469,000 |

$2,110 |

| Apr 2026 |

5.92% |

8.92% |

$358,000 |

$448,000 |

$2,129 |

Based on national median FT income of $98,124/yr (ABS Employee Earnings and Hours, May 2025). Max loan calculated at 35% DSR on assessed monthly repayment. Assessment rate = OO P&I rate + APRA 3pp buffer. Buying power assumes 20% deposit.

Source: RBA Statistical Table F6; APRA macroprudential settings update, May 2026; ABS Employee Earnings and Hours, May 2025.

The repayment comparison shows how higher rates changed borrowing capacity. In December 2021, a borrower at the maximum modelled loan capacity had an actual monthly repayment of $1,988. By April 2026, the same income supported a smaller maximum loan, but the actual monthly repayment was higher at $2,129.

Under this model, the April 2026 borrower has lower buying power but a higher monthly repayment. This reflects the effect of higher mortgage rates, which reduce modelled borrowing capacity while increasing repayments on the amount borrowed.

For a borrower on the mean full-time income of $106,657, the modelled buying power decline since 2021 is around $204,000, from approximately $691,000 to $487,000.

Borrowing power reduction for median-income earners, Dec 2021 to Apr 2026

Maximum purchase price with 20% deposit, national median FT income ($98,124/yr), APRA-assessed rate

The buying power reduction from December 2021 to April 2026 is approximately $188,000. The partial recovery in late 2025 as rates eased was reversed after cash rate increases before April 2026. Buying power at December 2023 (rate cycle peak) fell to $438,000, approximately $198,000 below the 2021 high.

Source: Calculated scenarios using ABS Employee Earnings and Hours (May 2025), RBA Table F6, APRA 3pp serviceability buffer.

Dwelling prices rose while modelled buying power fell

The national mean dwelling price rose from $916,800 in December 2021 to $1,111,100 in March 2026, an increase of $194,300. Over the same period, maximum modelled buying power on the median full-time income fell by approximately $188,000. The two measures moved in opposite directions over the period, showing how higher dwelling prices and lower modelled borrowing capacity widened the affordability gap for new buyers.

General information only

This article is for general informational and research purposes. Income thresholds and borrowing examples are calculated scenarios using official data inputs and a standardised methodology. They are not published official figures and do not constitute financial advice. Actual borrowing capacity depends on individual circumstances, including credit history, existing debts, living expenses, employment type and lender-specific policies.

References

- NHSAC, State of the Housing System 2026 (April 2026). Mortgage servicing ratio, deposit savings years, purchase affordability, home ownership rates by age.

- NHSAC, State of the Housing System 2025. Prior year comparators for mortgage servicing and deposit timelines.

- ABS, Total Value of Dwellings, March quarter 2026. National and state mean dwelling prices; capital-city median established house transfer prices.

- ABS, Average Weekly Earnings, November 2025. Full-time adult ordinary time earnings, national and by state/territory.

- ABS, Employee Earnings and Hours, May 2025. Median weekly earnings for full-time persons; income base for calculated scenarios.

- ABS, Lending Indicators, March quarter 2026. Average loan sizes, commitment volumes, investor lending share, first home buyer data.

- ABS, Lending Indicators methodology, March quarter 2026.

- RBA, Statistical Table F6, April 2026. New owner-occupier and investor P&I rates; historical rate series.

- APRA, Prudential Practice Guide APG 223, Residential Mortgage Lending, June 2025. Serviceability assessment criteria, income verification, living expense benchmarks, credit card and rental income treatment.

- APRA, Macroprudential settings update, May 2026. Confirmation of 3 percentage point serviceability buffer.