What upfront costs apply when buying a house?

Using a 5% allowance for non-deposit upfront costs, the national median house price of $745,000 would add around $37,250 to the cash required at settlement. On the national mean dwelling price of $1,074,700, the same allowance equals around $53,700. The exact amount depends on the state, property type, purchase price, and whether first-home buyer concessions apply.

Buying costs fall into two categories. The deposit is the buyer's equity contribution toward the property: it reduces the loan amount and builds ownership. Most other upfront costs are transactional costs paid at or before settlement. These can include stamp duty, conveyancing, registration charges and settlement adjustments, as well as building, pest and strata inspection costs and moving costs in some transactions. Unlike lenders mortgage insurance, many of these costs generally cannot be added to a standard mortgage.

How much deposit is needed to buy a house?

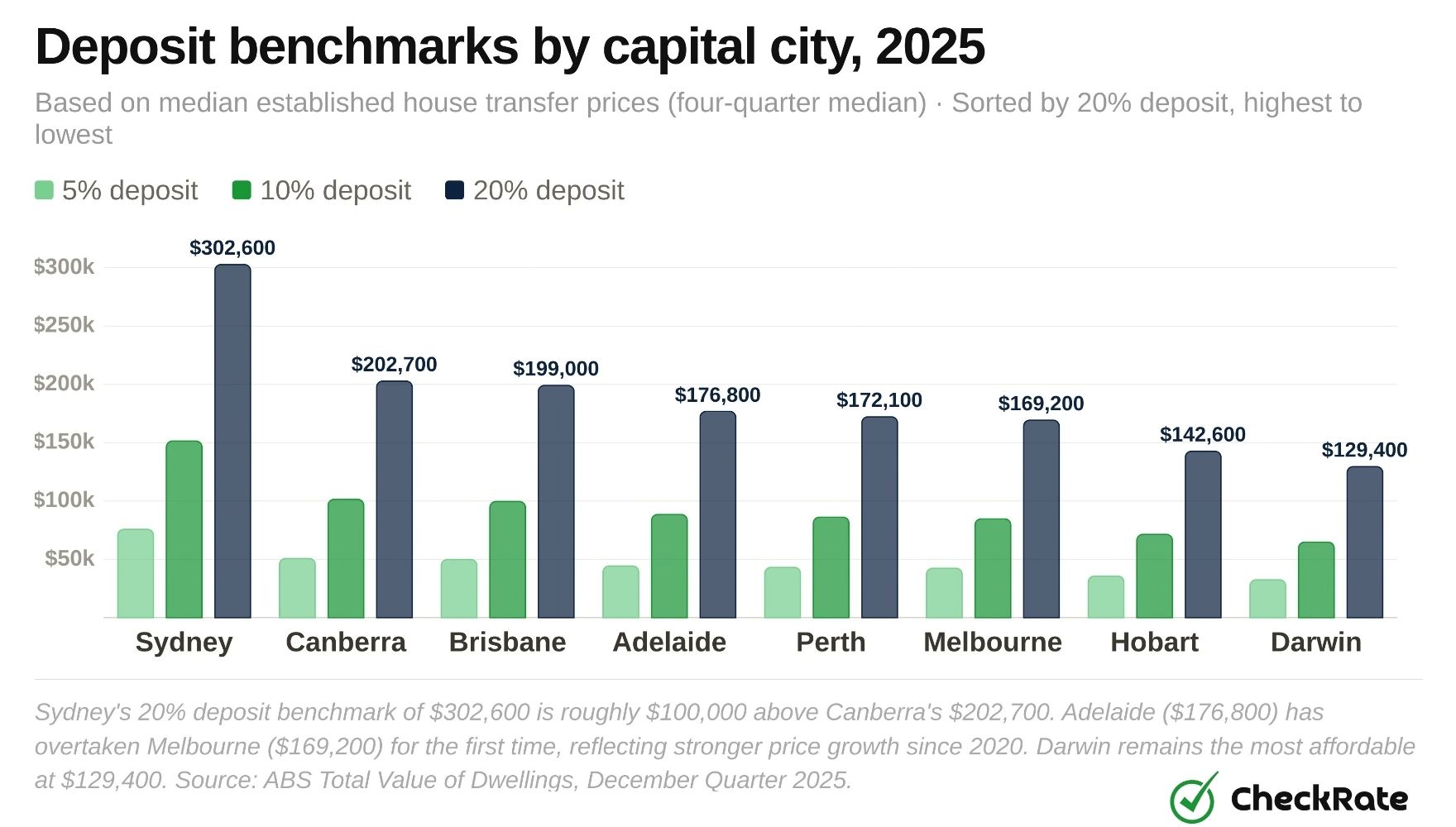

The 20% deposit benchmark ranges from $129,400 in Darwin to $302,600 in Sydney, a difference of more than $173,000 based on 2025 median prices.

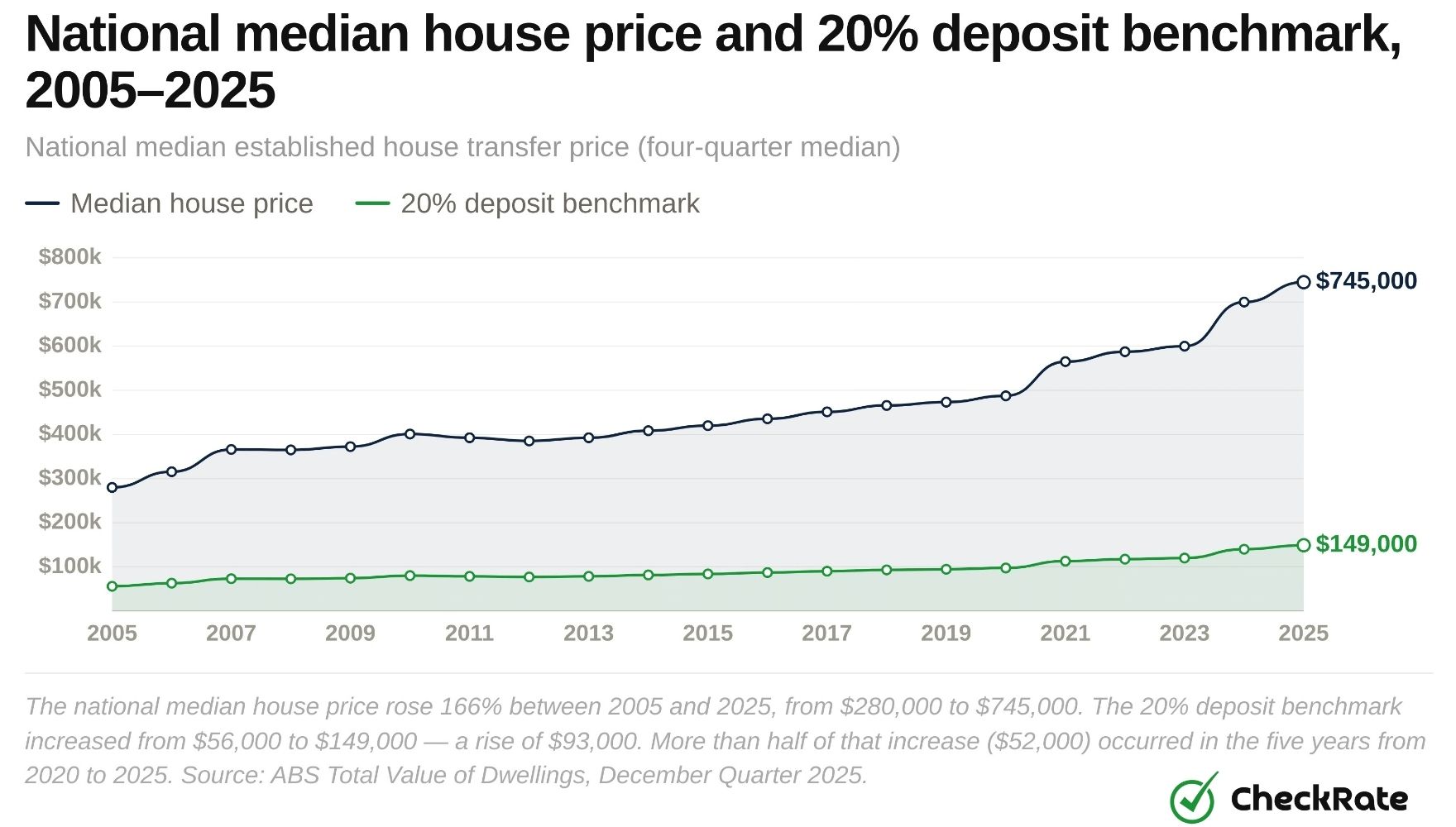

At the national median of $745,000, a 5% deposit is $37,250, a 10% deposit is $74,500, and a 20% deposit is $149,000. Sydney's 20% benchmark is more than double the national figure and more than double Darwin's $129,400.

Adelaide's 2025 median house price of $884,000 exceeded Melbourne's $845,900, giving Adelaide a higher 20% deposit benchmark than Melbourne. That reflects stronger price growth in Adelaide since 2020 and a shift in the usual capital-city ranking. Brisbane's median house price of $995,000 is also approaching $1 million.

How much does lenders mortgage insurance cost in Australia?

On an $800,000 property, LMI at 95% LVR costs an estimated $34,000 to $35,500. At 90% LVR, the same property attracts around $17,000. Reducing a deposit from 10% to 5% lowers the upfront deposit by $40,000, but roughly doubles the insurance cost. Most lenders allow the premium to be added to the loan, meaning interest can accrue on the premium over the life of the mortgage.

Despite being paid by the borrower, LMI protects the lender rather than the borrower. If the property is sold after a default and the sale price falls short of the outstanding loan, the insurer covers the lender's loss and can then seek to recover that amount from the borrower. State governments also charge stamp duty on the LMI premium itself: 9% in New South Wales and Queensland, 10% in Victoria, Western Australia, the Northern Territory and Tasmania, and 11% in South Australia.

| Deposit size | LVR | Cash deposit ($800k) | Estimated LMI premium | LMI required? |

|---|---|---|---|---|

| 20% | 80% | $160,000 | None | No LMI |

| 15% | 85% | $120,000 | $6,500–$9,000 | LMI applies |

| 10% | 90% | $80,000 | $16,500–$17,500 | LMI applies |

| 5% | 95% | $40,000 | $34,000–$35,500 | LMI applies |

Which state has the highest stamp duty in Australia?

Stamp duty, also called transfer duty, ranges from $26,909 in Tasmania to $53,572 in New South Wales at each state's mean dwelling price. The $26,663 gap reflects both NSW's higher mean dwelling price and its steeper upper-bracket rates. Victoria ranks second at $51,056, despite having a mean dwelling price $368,000 lower than NSW's.

Stamp duty is charged by state and territory governments using progressive rate structures. As property prices rise, more homes move into higher duty brackets. This has increased the effective duty cost on ordinary homes in several major markets.

| State/territory | Mean dwelling price | Standard stamp duty | FHB full exemption cap | FHB saving |

|---|---|---|---|---|

| New South Wales | $1,301,100 | $53,572.50 | $800,000 | $0 (above threshold) |

| Victoria | $933,100 | $51,056.00 | $600,000 | $0 (above threshold) |

| South Australia | $938,100 | $45,425.50 | No established-home exemption | $0 for established homes |

| Western Australia | $1,014,200 | $43,346.80 | $500,000 | $0 (above threshold) |

| Queensland | $1,066,000 | $34,645.00 | $700,000 existing; uncapped new builds | $0 for existing homes |

| ACT | $973,800 | $32,412.20 | $1,020,000 (income tested) | $32,412 if eligible |

| Northern Territory | $580,000 | $28,710.00 | None (cash grant instead) | $0 |

| Tasmania | $703,800 | $26,909.00 | $750,000 (ends June 2026) | $26,909 |

First-home buyer stamp duty concessions

In six of eight states and territories, the mean dwelling price exceeds the full first-home buyer exemption cap. At those price points, the concession produces no saving. Only Tasmania and the ACT fall within the full exemption threshold at the mean dwelling price, subject to eligibility rules.

What are the conveyancing fees when buying a house?

Conveyancing costs for a standard residential purchase typically range from $1,180 to $2,150. This covers the professional fee, statutory searches and the mandatory PEXA electronic settlement charge. A licensed conveyancer or solicitor usually manages the title transfer, coordinates with the mortgage lender and handles settlement.

The fee has two main parts: the professional service fee and disbursements. Disbursements are third-party or government charges for title searches, planning certificates, council checks and water clearances.

Settlement adjustments are a separate cash cost due at settlement. Where the vendor has prepaid council rates, water charges or body corporate levies beyond the settlement date, the buyer reimburses the vendor for the unused portion. These adjustments typically add $1,500 to $3,500, with the higher end more common for strata properties where quarterly levies can be significant.

| Cost component | Typical range | Description |

|---|---|---|

| Professional legal fee | $800–$1,500 | Contract review, title transfer, and legal execution |

| Disbursements and searches | $250–$500 | Title searches, planning certificates, council and water clearances |

| Electronic settlement (PEXA) | $130–$150 | Mandatory fee for digital title and funds transfer |

| Total estimated cost | $1,180–$2,150 | Standard residential purchase |

How much do building and pest inspections cost?

Indicative market pricing puts a combined building and pest inspection at around $500 to $1,000 for a standard property, with Sydney and Melbourne usually at the higher end. Inspections are not legally required, but once a contract settles, structural and pest-related defects generally become the buyer's responsibility. A report usually covers the roof void, subfloor, retaining walls and load-bearing elements, as well as termites, timber borers and moisture damage.

Costs vary by property size and location. Lower-cost inspections of around $300 may involve less than an hour on site and use more standardised report templates, which may provide less detail for price discussions during the cooling-off period.

| Market | Apartment/unit | Standard 3–4 bed house | Large or complex home |

|---|---|---|---|

| Sydney metro | $400–$550 | $600–$750 | $800–$1,000+ |

| Melbourne metro | $400–$550 | $600–$750 | $800–$1,000+ |

| Brisbane / Gold Coast | $350–$500 | $550–$700 | $700–$800+ |

| Regional areas | $300–$450 | $500–$650 | $650–$900 |

Moving, utility connection and insurance setup costs

Moving and setup costs typically add around $2,400 to $4,900 for a standard three-bedroom home. The main costs are removalists ($1,200 to $2,500), building insurance ($1,000 to $2,000 per year), and utility connections for NBN, electricity and gas ($200 to $400). Building insurance may need to be in place before settlement, depending on the lender, contract and state rules, so the first premium can fall due before moving day.

| Cost item | Typical range |

|---|---|

| Professional removalists (3-bedroom move) | $1,200–$2,500 |

| Utility connections (NBN, electricity, gas) | $200–$400 |

| Building insurance (annual premium) | $1,000–$2,000 |

| Total estimated moving and setup | $2,400–$4,900+ |

What extra costs are paid at property settlement?

Bank fees, registration charges and settlement adjustments typically add $2,500 to $5,300 to the total cash needed at settlement. These three cost categories cover lender fees, government land registry charges and pro-rata reimbursements to the vendor. Unlike LMI, these costs are generally paid in cash at settlement rather than added to the mortgage.

Bank application and valuation fees

Most lenders charge an application or establishment fee to cover underwriting and loan setup. Some also require an independent property valuation to confirm that the property supports the loan amount. These fees are sometimes waived, particularly in competitive lending environments.

| Fee | Typical range | Notes |

|---|---|---|

| Application/establishment fee | $500–$1,000 | Covers loan underwriting and facility setup; sometimes waived |

| Property valuation fee | $200–$300 | Independent valuation to confirm security value; often absorbed by lender |

| Total estimated bank fees | $700–$1,300 |

Mortgage and title registration fees

Mortgage registration fees range from $125.70 in Victoria to $238.14 in Queensland for the 2025–26 financial year. Mortgage registration is a fixed government charge that records the lender's security interest against the property title. A separate title transfer fee records the change of ownership.

In most states, the title transfer fee varies by property value and is charged on top of the fixed mortgage registration fee. NSW is the exception in this comparison, with a flat $175.70 fee for both mortgage registration and title transfer.

| State/territory | Mortgage registration | Title transfer fee | Combined total |

|---|---|---|---|

| Queensland | $238.14 | Varies by value | $238.14+ |

| Western Australia | $216.60 | Varies by value | $216.60+ |

| South Australia | $198.00 | Varies by value | $198.00+ |

| ACT | $178.00 | Varies by value | $178.00+ |

| Northern Territory | $176.00 | Varies by value | $176.00+ |

| New South Wales | $175.70 | $175.70 | $351.40 |

| Tasmania | $163.30 | Varies by value | $163.30+ |

| Victoria | $125.70 | Varies by value | $125.70+ |

Settlement adjustments

Settlement adjustments are cash payments calculated at settlement. When a vendor has prepaid council rates, water charges or body corporate levies for a period that extends beyond settlement, the buyer reimburses the vendor for the unused days. The conveyancer calculates the amount based on the settlement date and the daily rate of each charge.

Like the other costs in this section, settlement adjustments are generally paid in cleared funds on settlement day and are not usually added to the mortgage.

| Adjustment type | Typical amount | Applies to |

|---|---|---|

| Council rates (pro-rata) | $400–$600 | All properties |

| Water availability charges (pro-rata) | $200–$300 | All properties |

| Body corporate/strata levies (pro-rata) | $1,000–$2,500 | Units and apartments only |

| Total estimated settlement adjustments | $600–$3,400 | Varies by property type and settlement timing |

Taken together, stamp duty, conveyancing, bank fees, registration charges and settlement adjustments can add tens of thousands of dollars to the cash required at settlement, depending on the state, purchase price and concession eligibility.

Worked example: upfront costs on an $800,000 NSW home

To purchase an $800,000 established home in New South Wales with a 10% deposit, a buyer would need an estimated $117,063 in cash at settlement. That is more than $37,000 above the deposit alone. Stamp duty accounts for $30,412 of that gap. The remaining $6,651 covers legal fees, inspections, bank fees, registration charges, settlement adjustments and moving costs. LMI at 90% LVR adds approximately $17,000 to the loan, but because it is capitalised, it is not included in the cash settlement total.

| Cost item | Amount | Notes |

|---|---|---|

| Deposit (10%) | $80,000 | Equity contribution toward the property |

| Stamp duty (NSW) | $30,412 | Standard progressive rate on $800,000 transfer |

| Conveyancing and legal fees | $1,600 | Professional fee, statutory searches, PEXA settlement |

| Building and pest inspection | $600 | Combined inspection for a standard Sydney property |

| Bank application and valuation fee | $800 | Establishment fee and independent property valuation |

| Mortgage registration fee (NSW) | $175.70 | NSW Land Registry charge for recording lender's security |

| Title transfer registration fee | $175.70 | NSW Land Registry charge for change of ownership |

| Settlement adjustments | $1,500 | Pro-rata reimbursement for prepaid council and water rates |

| Moving, utilities, and building insurance | $1,800 | Removalists, connections, first year of building insurance |

| Total cash required at settlement | $117,063 | Excludes approximately $17,000 LMI capitalised into the loan |

First-home buyer grants, concessions and guarantee schemes

Since October 2025, the Home Guarantee Scheme has had no income limits and no annual place cap. Eligible buyers, including first-home buyers and people who have not owned property in the past ten years, can use a 5% deposit while the government guarantees part of the loan. This removes the LMI that would otherwise apply at 95% LVR.

On an $800,000 property, the LMI cost that would otherwise apply at 95% LVR is estimated at $34,000 to $35,500. Property price caps still apply by state and region. In NSW capital cities, the cap is $1,500,000. In Queensland capital cities, the cap is $1,000,000. These caps are reviewed periodically.

| State | FHB exemption (established) | FHB exemption (new builds) | Cash grant |

|---|---|---|---|

| NSW | Up to $800,000; partial to $1,000,000 | Up to $800,000; partial to $1,000,000 | $10,000 (new builds to $600k) |

| VIC | Up to $600,000; partial to $750,000 | Up to $600,000; partial to $750,000 | $10,000 (new builds to $750k) |

| QLD | Up to $700,000; partial to $800,000 | Uncapped (from May 2025) | $15,000 or $30,000 |

| WA | Up to $500,000; partial to $700,000 metro | Up to $500,000; partial to $700,000 | $10,000 |

| SA | No established-home exemption | Uncapped | $15,000 (new builds, no cap) |

| TAS | Up to $750,000 (ends June 2026) | Up to $750,000 (permanent) | $30,000 (new builds, ends Jun 2026) |

| ACT | Up to $1,020,000 (income tested); partial to $1,455,000 | Up to $1,020,000 (income tested) | None |

| NT | None | None | $50,000 |

Estimate your total upfront buying costs

Enter a state, purchase price, and deposit size to estimate the total cash needed at settlement. Stamp duty is calculated using each state's standard progressive rate schedule, with first-home buyer concessions applied where the purchase price falls within the relevant threshold.

References

- 1.Australian Bureau of Statistics (ABS), Total Value of Dwellings, December Quarter 2025: Released March 2026. National mean dwelling price and state breakdowns.

- 2.ABS Total Value of Dwellings, Dec Quarter 2025: Median established house and attached dwelling transfer prices by state and territory, four-quarter median.

- 3.NHSAC, State of the Housing System 2025: Average time to save a home deposit.

- 4.ASIC Moneysmart, Buying a home: Deposit, upfront buying cost and lenders mortgage insurance context.

- 5.Revenue NSW, Transfer (stamp) duty rate schedules (2025–26): Standard progressive rates and first-home buyer thresholds.

- 6.State Revenue Office Victoria, Transfer duty rates and first-home buyer concessions (2025–26): Victorian transfer duty schedules.

- 7.Queensland Revenue Office, Transfer duty rates and first home concession (2025–26): Queensland concessional home rate and first-home concession.

- 8.RevenueSA, Stamp duty rates (2025–26): South Australia stamp duty schedules.

- 9.WA Department of Finance, Transfer duty schedules (2025–26): Western Australia transfer duty assessment.

- 10.State Revenue Office Tasmania, Duty rates and first home buyer exemption (2025–26): Tasmanian exemption ends June 2026.

- 11.ACT Revenue, Duty rates and Home Buyer Concession Scheme (2025–26): Income-tested concession thresholds.

- 12.Territory Revenue Office, Stamp duty and First Home Owner Grant (2025–26): Northern Territory stamp duty schedules and $50,000 grant.

- 13.Housing Australia, Home Guarantee Scheme: Expanded terms from October 2025.

- 14.Australian Institute of Conveyancers (AIC): Indicative conveyancing fee context.

- 15.State and territory land registry fee schedules, 2025–26: Mortgage registration and title transfer fee comparisons.

- 16.ASIC Moneysmart, Lenders mortgage insurance: LMI definition, lender-protection context and the 80% LVR threshold.

- 17.NSW Fair Trading and Consumer Affairs Victoria, Pre-purchase inspection reports: Pre-purchase inspection scope and provider variation.

Data Snapshots