Average credit card debt in Australia was $2,217 per active account in February 2026, based on balances accruing interest divided by active accounts. Total credit and charge card balances were $44.2 billion.

9 min read 08 June 2026Updated 08 June 2026 Fact checked

Key figures at a glance

$2,217

Average interest-bearing balance per active account, calculated as balances accruing interest ÷ active accounts

$44.2B

Total credit and charge card balances across 12.2 million accounts

$21.7B

Balances accruing interest, down 41% from the $36.6B peak in 2012

16.6M

Cards on issue, down 32% from the 24.3M peak in 2016

Section 01What Australians owe in aggregate

Total credit and charge card balances in Australia

Australians had $44.2 billion owing on credit and charge card accounts in February 2026, spread across 12.2 million accounts. That puts the country 16.6% below the all-time peak of $52.9 billion in November 2017, but still 27% above the COVID-era low of $34.7 billion hit in September 2021.

The total covers everything currently sitting on credit and charge card accounts: recent purchases that haven't yet been paid off, plus revolving debt being carried month to month.

After peaking in late 2017, balances drifted down through 2018 and 2019. They fell sharply during the COVID period, with total balances declining by roughly $18 billion in under four years. The recovery since has brought balances back to around 2008 levels in dollar terms, but after inflation, the real figure remains below where it was a decade ago.

Current total

$44.2B

February 2026 across 12.2 million accounts

All-time peak

$52.9B

November 2017, before the long decline

COVID low

$34.7B

September 2021, after stimulus paydowns

Vs peak

−16.6%

Total balances remain below the 2017 high

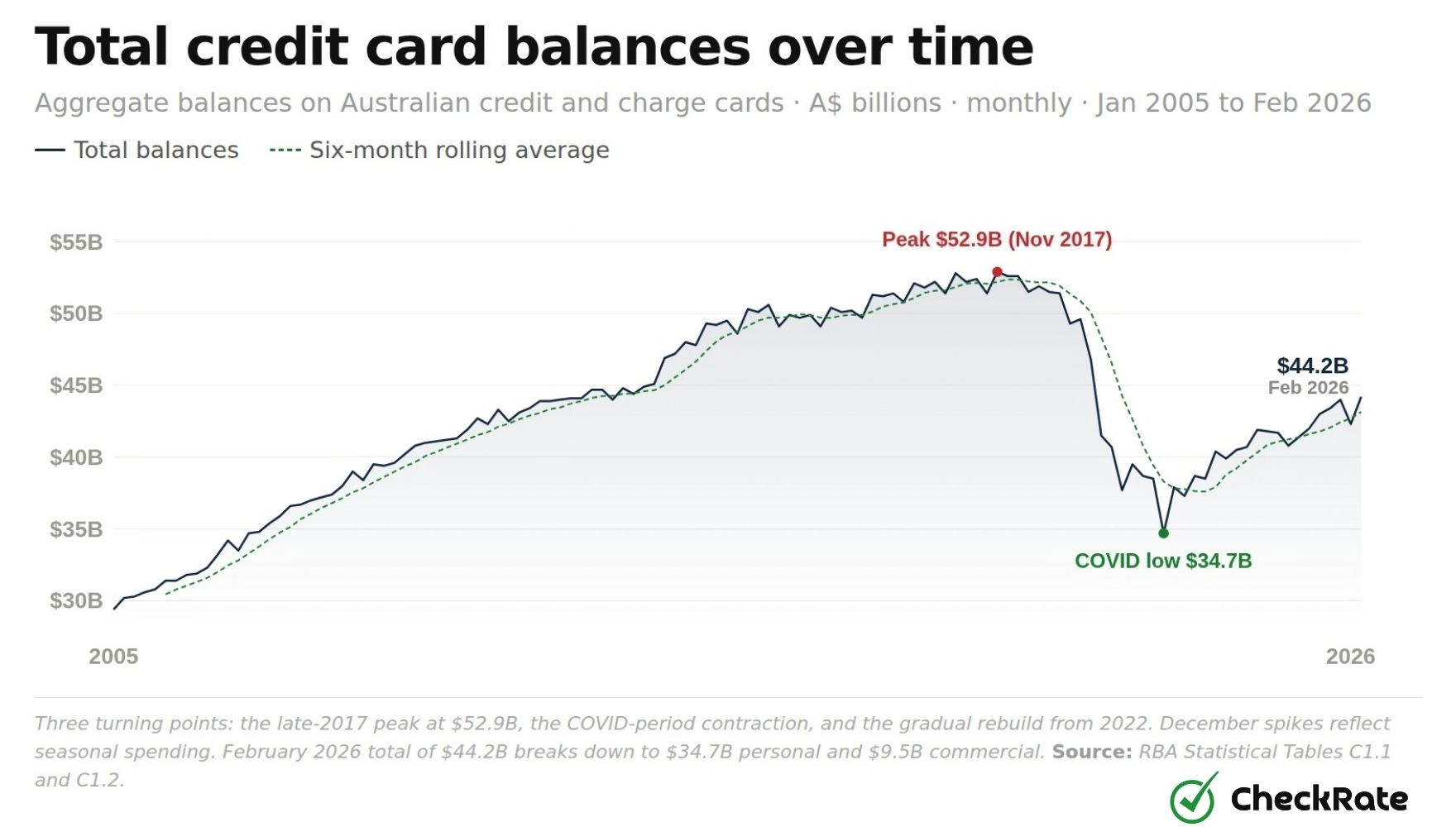

Total credit card balances over time

Aggregate balances on Australian credit and charge cards, $ billions · December snapshots 2005–2025, plus February 2026

Total balances

Three turning points stand out: the late-2017 peak at $52.9 billion, the sharp COVID-period contraction, and the gradual rebuild from 2022 onwards. The February 2026 total of $44.2 billion breaks down to $34.7 billion on personal cards and $9.5 billion on commercial cards.

Source: RBA Statistical Tables C1.1 and C1.2.

Useful context

The $44.2 billion total covers both credit cards and charge cards, which the RBA tracks together. Credit cards make up the bulk of accounts and most balances accruing interest. Charge cards, around 1.6 million accounts in February 2026, usually need to be paid in full each statement period.

Section 02Average debt per active account

How average credit card debt is calculated

The average active credit card account carries $2,217 in interest-bearing debt as of February 2026, down roughly 38% from the 2012 peak of $3,550. The headline number depends heavily on how you do the maths, though. Different combinations of numerator and denominator give very different answers, ranging from about $2,200 to around $4,500 per account or card measure. The clearest account-based measure strips out dormant accounts and recent purchases not yet accruing interest.

$2,217

Per active account

Average credit card debt · Feb 2026

The average active credit card account carried $2,217 in interest-bearing debt. The figure is calculated as balances accruing interest ($21.74 billion) divided by active accounts (9.81 million), so it excludes dormant accounts and recent purchases sitting inside the interest-free period. The peak under this measure was $3,550 in mid-2012, meaning the average interest-bearing debt per active account is now about 38% lower than it was then.

How the $2,217 figure is calculated

The $2,217 figure is an article-calculated measure based on official RBA data. It divides balances accruing interest by active accounts. This excludes recent purchases that are not yet accruing interest and excludes accounts that were not active in the most recent quarter. Both credit cards and charge cards are included, in line with the RBA series.

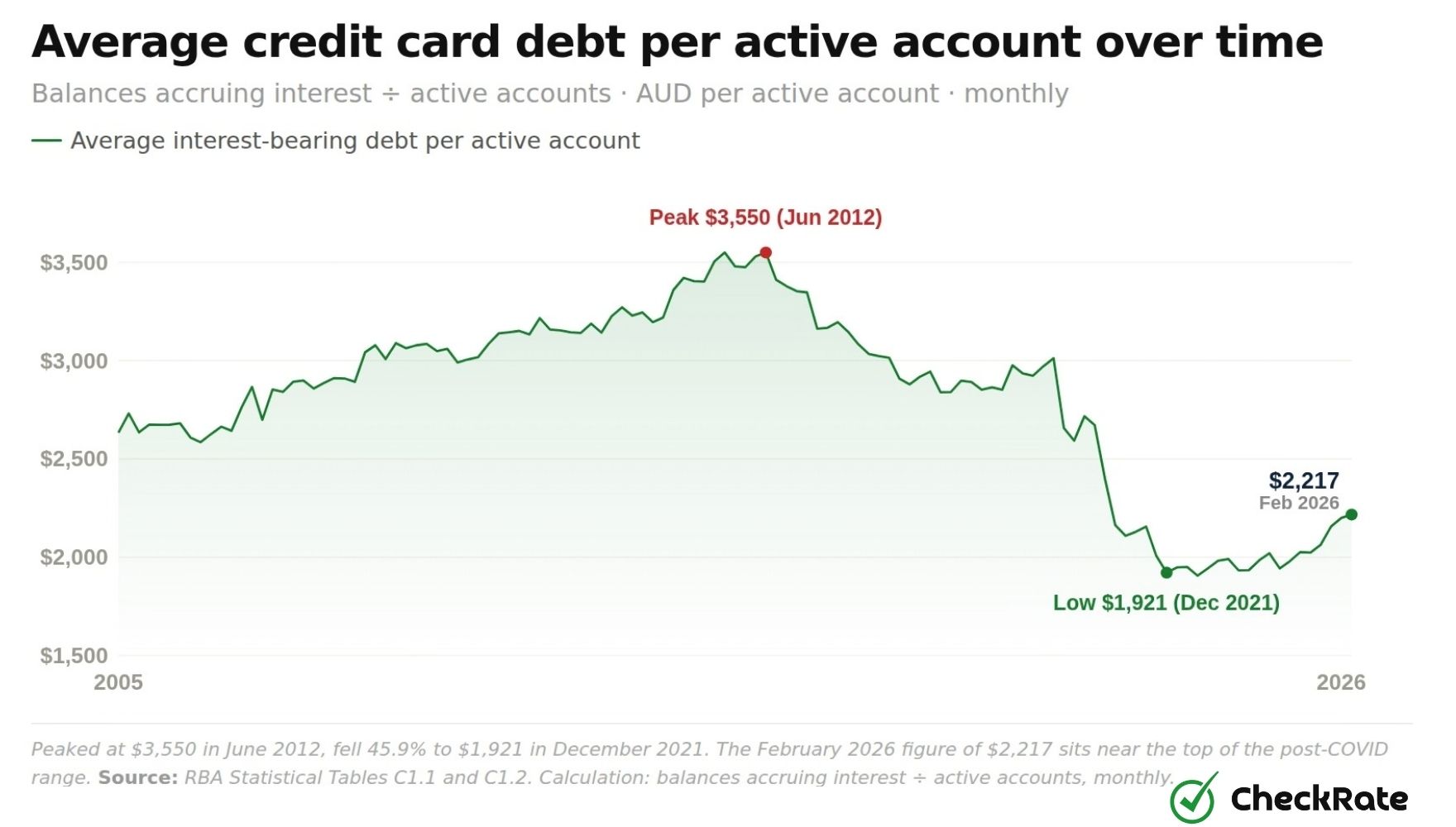

Average credit card debt per active account over time

Balances accruing interest ÷ active accounts, $ AUD per active account

Avg interest-bearing debt per active account

Average interest-bearing debt per active account peaked at $3,550 in June 2012 and fell to $1,921 in December 2021, a peak-to-trough decline of 45.9%. The figure has since stabilised in the $1,900 to $2,200 range. The February 2026 figure of $2,217 sits near the top of that post-COVID range.

Source: RBA Statistical Tables C1.1 and C1.2. Calculation: balances accruing interest ÷ active accounts.

−$1,629

Peak-to-trough fall in average interest-bearing debt

Average interest-bearing debt per active account fell from $3,550 at the June 2012 peak to $1,921 in December 2021. That was a peak-to-trough fall of $1,629, or 45.9%. By February 2026, the figure had risen to $2,217, leaving average interest-bearing debt per active account $1,333 below the 2012 peak.

Average credit card debt by year

Looking year by year, average interest-bearing debt per active account peaked at $3,475 in December 2011 and bottomed at $1,921 in December 2021, a peak-to-trough fall of 44.7%. The biggest single-year drop came in 2020, when the figure fell 18.7% over 12 months. After stabilising in the $1,920 to $1,980 range from 2021 to 2024, the average rose to $2,156 by December 2025 and $2,217 by February 2026.

Average credit card debt by year · 2005 to 2026

Calendar year

Avg debt per active account

YoY change

Avg total ÷ accounts

2005

$2,643

n/a

$2,745

2006

$2,892

+9.4%

$2,949

2007

$3,018

+4.4%

$3,068

2008

$3,142

+4.1%

$3,146

2009

$3,219

+2.4%

$3,251

2010

$3,402

+5.7%

$3,328

2011 · peak

$3,475

+2.1%

$3,356

2012

$3,379

-2.8%

$3,283

2013

$3,167

-6.3%

$3,242

2014

$3,034

-4.2%

$3,255

2015

$2,879

-5.1%

$3,172

2016

$2,840

-1.3%

$3,166

2017

$2,864

+0.8%

$3,170

2018

$2,923

+2.1%

$3,269

2019

$2,593

-11.3%

$3,392

2020

$2,109

-18.7%

$2,901

2021 · low

$1,921

-8.9%

$2,877

2022

$1,943

+1.1%

$3,047

2023

$1,934

-0.4%

$3,102

2024

$1,980

+2.4%

$3,424

2025

$2,156

+8.9%

$3,582

2026 · Feb · latest

$2,217

+2.8%

$3,618

Each row is a December snapshot, except 2026, which uses February, the latest month available. The middle column is the headline measure: balances accruing interest ÷ active accounts. The right-hand column shows total balances ÷ total accounts for comparison. Source: RBA Statistical Tables C1.1 and C1.2.

Section 03Credit card balances by category

The three types of credit card debt in Australia

Of the $44.2 billion owing on credit and charge card accounts in February 2026, personal accounts made up roughly 79%, or $34.7 billion. Commercial accounts accounted for the remaining 21%, or $9.5 billion. The RBA also tracks cash advances separately as a transaction measure, rather than a balance category.

Personal credit and charge card debt

Personal accounts held $34.7 billion in total balances, with $19.6 billion of that accruing interest in February 2026. Personal cards accounted for around 79% of total credit and charge card balances and almost 90% of balances accruing interest.

Personal accounts have accounted for most of the long-run decline in Australian credit and charge card balances. The number of personal accounts fell from a peak of around 15.5 million in mid-2017 to 11.5 million in February 2026, a drop of approximately 26%.

Commercial credit and charge card debt

Commercial accounts had $9.5 billion in balances on commercial cards, with $2.1 billion of that accruing interest in February 2026. Commercial cards made up roughly 21% of total balances but only 10% of balances accruing interest, showing that a smaller share of commercial card balances was interest-bearing than personal card balances.

Commercial balances have been broadly steady since 2018, moving between $7 billion and $10 billion. The long-run decline in total card balances has been concentrated more heavily in personal accounts than commercial accounts.

Cash advances

Australians took out $343 million in cash advances across 801,000 transactions in February 2026. Both figures are down roughly 70% from their late-2008 peaks. A cash advance is money withdrawn from a credit card account as cash, usually through an ATM or over the counter at a bank.

Monthly cash advances peaked at $1.09 billion in late 2008, when Australians made 2.85 million such transactions in a single month. The decline since then occurred alongside the rise of debit cards, greater use of everyday transaction accounts, and the broader move away from cash for daily spending.

The three types of credit card debt, side by side

Latest figures · February 2026

Personal balances

Stock — owed on personal cards

$34.7B

Commercial balances

Stock — owed on business cards

$9.5B

Cash advances (Feb '26)

Flow — value of withdrawals

$343M

Personal and commercial balances are stocks, meaning amounts owed at a point in time. Cash advances are a flow, meaning the value of withdrawals during the latest month. Personal and commercial balances add up to the $44.2 billion total.

Source: RBA Statistical Tables C1.1 and C1.2 (Feb 2026).

Credit card debt by type, year by year

A yearly view shows that 2021 was the first year in which non-interest-bearing balances were higher than interest-bearing balances. They have remained higher in each year since. Total balances peaked in 2017 at $52.9 billion before declining, while commercial balances more than doubled from $4.2 billion in 2015 to $9.2 billion in 2025, even as personal balances fell.

Credit card debt by type · 2015 to Feb 2026

December snapshots, $ billions

Accruing interest

Non-interest-bearing

Bar height = total balances. Green = balances accruing interest. Navy = non-interest-bearing balances. The crossover year was 2021, when navy first exceeded green.

Source: RBA Statistical Tables C1.1 and C1.2.

Section 04The size of the card system

Credit card statistics in Australia

Beyond balances, the number of credit and charge card accounts has also fallen over the past decade. The four headline figures below describe the overall size and structure of the card system in Australia.

Accounts on issue

12.2M

All credit and charge card accounts · −27% from 2017 peak

Active accounts

9.81M

Used in the most recent quarter · −13% from 2016 peak

Cards on issue

16.6M

Including supplementary cards · −32% from 2016 peak

Credit limits

$126B

Total credit available · −18% from 2018 peak

Three relationships between these numbers stand out:

About 20% of credit and charge card accounts on issue were not active in the most recent quarter.

The ratio of cards to accounts was roughly 1.4, reflecting supplementary cards issued on some accounts.

Credit-limit utilisation, measured as total balances divided by total credit limits, was about 35%. Interest-bearing balances were equal to about 17% of total credit limits.

Headline utilisation

How much of available credit is being used

35%

0%30% healthy100%

$44.2 billion in total balances against $125.5 billion in available credit. Sits just above the 30% threshold often used as a "healthy" signal in consumer credit analysis.

"Real" utilisation

How much is actually being borrowed

17%

0%30% healthy100%

Strips out balances inside the interest-free period, leaving only the borrowed money actually accruing interest. Comfortably below the 30% threshold.

Useful context

The utilisation figures show that total balances remain well below total available credit limits. Interest-bearing balances account for a smaller share again, at about 17% of total limits. Together with lower balances accruing interest than a decade ago and a repayments-to-purchases ratio near 100%, this suggests credit cards are being used less as a revolving debt product than they were in earlier periods.

Section 05Payment activity

Credit card repayments and purchases in Australia

Repayments to credit card accounts came to $35.9 billion in February 2026, against $36.8 billion in purchases over the same month. That puts the repayments-to-purchases ratio at roughly 97%. December 2025 set the all-time monthly repayment record at $45.9 billion, reflecting the seasonal clearing of Christmas spending.

A repayments-to-purchases ratio close to 100% shows that, in aggregate, Australians are paying off about as much as they spend on credit and charge cards each month. It does not show whether individual cardholders paid off their full balance each cycle. At the system level, the data shows repayments were close to purchases in February 2026.

Repayments (Feb 2026)

$35.9B

Monthly value of repayments to credit card accounts

Purchases (Feb 2026)

$36.8B

Monthly value of purchases on credit cards

Repayments / purchases

97%

Close to break-even on a monthly basis

Record month

$45.9B

December 2025 monthly repayments, all-time high

Annual credit card repayments and purchases

$ billions per month · December snapshots 2005–2025, plus February 2026

Repayments

Purchases

Repayments and purchases now move almost in lockstep. The two lines have tracked closely since around 2017, the period when total balances also stopped growing. December months show seasonal spikes for Christmas spending.

Source: RBA Statistical Tables C1.1 and C1.2.

$45.9B

Highest monthly repayment value on record

December 2025 recorded $45.9 billion in credit card repayments, the highest monthly value in the RBA series. That was more than 27% above December 2023, when repayments were $35.6 billion. Monthly repayments often rise around the end of the year, reflecting the seasonal pattern in card activity.

Credit card spending and purchase trends

Beyond the headline totals, three spending patterns stand out in the data:

Mobile wallet payments have grown quickly since 2018. In February 2026, they made up $6.8 billion of $36.8 billion in total purchases, or about 18%, up from near zero a decade earlier.

Overseas purchases have rebounded since COVID, reaching $2.1 billion in February 2026. That was the second-largest monthly figure on record, behind late 2025.

Cash advances have continued to decline. They now account for less than 1% of total credit card transaction value, down from roughly 5% in the late 2000s.

Key moments in two decades of credit card data

Five dates stand out across the full series. Together, they show how credit and charge card balances, account numbers and repayments have changed over time.

Jun 2012

Balances accruing interest peak at $36.6 billion

Balances accruing interest reached their highest point in June 2012. Average interest-bearing debt per active account also peaked that month at $3,550. This measure has remained below that level since.

Oct 2016

Cards on issue peaked at 24.3 million

Cards on issue reached their highest point in October 2016. By February 2026, the number of cards on issue had fallen to 16.6 million, a decline of around 32%.

Nov 2017

Total balances peaked at $52.9 billion

Total credit and charge card balances reached $52.9 billion in November 2017. By February 2026, total balances were $44.2 billion, or 16.6% below that peak.

Late 2021

COVID low and the interest-bearing crossover

Total balances fell to $34.7 billion in September 2021. By the end of 2021, non-interest-bearing balances were also higher than interest-bearing balances for the first time in the annual December snapshot, and they have remained higher in each year since.

Dec 2025

Record $45.9 billion in monthly repayments

Monthly credit card repayments reached $45.9 billion in December 2025, the highest monthly value in the RBA series. In recent years, repayments have often been close to, or above, monthly purchases.

Section 06Pulling the picture together

What the data shows about credit card debt in Australia

Five clear patterns emerge across the full RBA series. Together, they show how credit card balances, account numbers, repayments and cash advances have changed over the past two decades.

Key terms used in this section

Balances accruing interest: the part of a credit card bill being carried over from previous months and charged interest. Utilisation: how much of a card's credit limit is actually being used. Revolving debt: a balance that rolls over from month to month rather than being paid off in full. Nominal terms: dollar figures that haven't been adjusted for inflation.

📉

01.Total credit card debt has fallen 17% from its 2017 peak

Total balances dropped from $52.9 billion in late 2017 to a COVID-era low of $34.7 billion in September 2021, before rebuilding to $44.2 billion by early 2026. The recovery is partial rather than complete. After adjusting for inflation, total balances are still well below where they were a decade ago.

💳

02.Interest-bearing credit card debt has fallen further and faster

The amount of debt being charged interest peaked at $36.6 billion in 2012 and now sits at $21.7 billion, a 41% drop in dollar terms. The share of total balances being charged interest has fallen from 72% in 2008 to about 49% today.

🏠

03.The decline is concentrated in personal accounts

Business and corporate card balances have been broadly flat since 2018. Personal accounts, on the other hand, have fallen from a peak of 15.5 million to 11.5 million. The long retreat from credit cards in Australia has been more visible in personal accounts than in commercial accounts.

🧮

04.Remaining card accounts carry less interest-bearing debt

Average interest-bearing debt per active account has settled at around $2,200 since COVID, well below the 2012 peak of $3,550. Monthly repayments have closely matched monthly purchases for years. Interest-bearing balances are equal to about 17% of total credit limits.

🏧

05.Credit cards are rarely used for cash withdrawals

Cash advances have fallen by about 70% since 2008 and now make up less than 1% of total credit card transaction value. Cash advances have become a much smaller part of credit card activity.

The Australian credit card has not disappeared. It has been narrowed: used by a smaller, more concentrated group of cardholders, more often as a payment tool and less often as a borrowing tool. That is the most useful summary the data offers across two decades.

General information only

This article is based on publicly available data from the Reserve Bank of Australia. It is general information only and does not constitute financial or consumer advice. It does not consider individual financial circumstances.

ReferencesSources & methodology

Reserve Bank of Australia. Statistical Tables C1.1 (Credit and Charge Cards: Aggregate) and C1.2 (Personal and Commercial breakdowns), monthly series Jan 2005 to Feb 2026.

Methodology: Average debt per active account is calculated as balances accruing interest ÷ active accounts. Total balance averages are calculated as total balances ÷ accounts, active accounts or cards on issue, depending on the comparison. The repayments-to-purchases ratio is calculated as monthly repayments ÷ monthly purchases. Credit-limit utilisation is calculated as total balances ÷ credit limits.

"Active account" follows the RBA's published definition: a credit or charge card account that has had at least one transaction in the most recent quarter.

All dollar figures are in nominal AUD unless explicitly described as inflation-adjusted. Inflation-adjusted comparisons referenced in the text use ABS CPI as the deflator.

For February 2026, aggregate totals were calculated from the RBA C1.2 personal and commercial card breakdowns. Earlier months use the RBA C1.1 aggregate series.

Data Snapshots

Average Credit Card Debt per Active Account Over TimeTotal Credit Card Balances Over Time