Australian wealth statistics: net worth, assets and the wealth gap

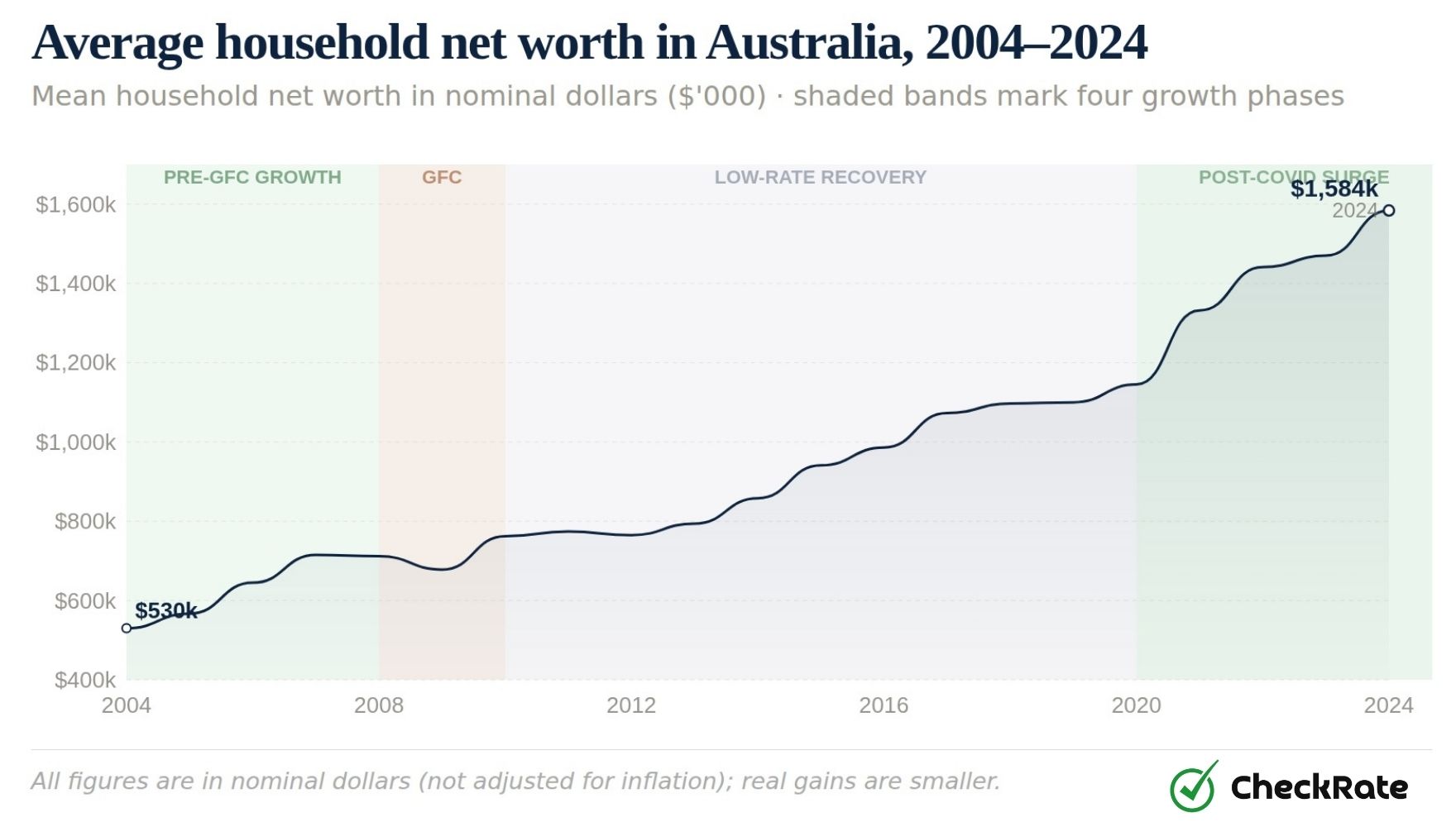

Australia's average household net worth reached about $1.58 million in 2024, nearly three times the $530,000 recorded in 2004. But the typical household holds far less: the latest detailed survey recorded a median net worth of $579,200. Explore wealth distribution, concentration, superannuation balances by age and gender, and the wealth gap.

14 min read 03 June 2026Updated 08 June 2026 Fact checked

Key figures

$1.58m

Mean household net worth, 2024 National Accounts

$579k

Median household net worth, most recent survey (2019–20)

44%

Share of national wealth, wealthiest 10% of households

0.611

Wealth Gini coefficient, nearly double the income Gini of 0.324

Section 01Average and median net worth

Average and median household net worth in Australia

What is the average household net worth in Australia?

Average (mean) household net worth was approximately $1.58 million in 2024, up from $530,000 in 2004. The median tells a different story: the latest detailed survey recorded median household net worth at $579,200 in 2019–20, less than 40% of the 2024 average. The gap between the mean and median shows how concentrated wealth is at the top of the distribution.

Household net worth is the value of everything a household owns, including property, superannuation, investments, vehicles and contents, minus what it owes, such as mortgages and personal debts.

Because the mean is pulled upward by a smaller number of very wealthy households, the median shows the midpoint of the household wealth distribution.

Mean (average)

2024 National Accounts estimate

$1.58m

Pulled upward by high-net-worth households

2.7×

apart

Median

2019–20 survey baseline

$579k

The midpoint of the distribution

That gap is not new. When both figures were last measured together in 2019–20, average household net worth was $1.04 million, while the median was $579,200. By 2024, the average had risen to $1.58 million.

The 2024 median cannot be measured directly without updated survey data, but the gap may have widened since then. Post-2020 wealth gains were driven largely by rising property values and financial asset prices, which mainly benefited households that already owned assets.

Growth has also been uneven over time. Average household net worth rose from $530,000 in 2004 to around $1.1 million by 2019, with only a brief setback during the 2008–09 global financial crisis. After 2020, growth accelerated. In four years, average net worth increased by approximately $440,000, driven by low interest rates, rising property values and higher financial asset returns.

Average household net worth in Australia, 2004–2024

Mean household net worth in nominal dollars ($'000). Shaded bands mark four growth phases.

All figures are in nominal dollars (not adjusted for inflation); real gains are smaller.

Source: ABS National Accounts: Finance and Wealth (Cat. 5232.0), Table 35; ABS Household and Family Projections (Series II). Nominal terms.

About data availability

The ABS cancelled the 2023–24 Survey of Income and Housing in late 2025, citing low response rates and significant under-representation of renter households. The 2019–20 survey remains the most recent source of detailed wealth data, including median net worth and breakdowns by age, gender, and household type. Updated figures are not expected before mid-2027.

Australian wealth is concentrated in the top 20% of households

The top 20% of Australian households hold approximately 63% of national household wealth, with an average net worth of $3.23 million. The bottom 60% collectively hold about 17%.

The gap is widest at the extremes. The wealthiest 10% of households hold around 44% of all household wealth, with an average wealth of $5.2 million. The bottom 20% hold less than 1%, with an average wealth of around $35,200.

Wealth in Australia is far more concentrated than income.

44%

Share of all Australian household wealth held by the top 10%

The top decile holds an average of $5.2 million per household, with a net worth threshold of more than $2.6 million to enter the group. At the other end, the bottom 20% of households average around $35,200 in net worth. Of all new wealth generated since 2003, approximately 45% has flowed to the top 10%.

Wealth held by Australian household wealth groups

Share of total national household wealth.

Quintile

Share of total wealth

Share

Avg net worth

Top 20%

62.8%

62.8%

$3,230,000

4th quintile

20.5%

20.5%

not reported

Middle 20%

11.3%

11.3%

$564,500

2nd quintile

4.8%

not reported

Bottom 20%

0.7%

$35,200

Note: Quintile shares are the ABS five-way distribution. ACOSS publishes average net worth only for the top, middle and bottom quintiles, so the 2nd and 4th are not separately stated.

Source: Shares from ABS Survey of Income and Housing 2019-20; average net worth from ACOSS and UNSW Sydney, Inequality in Australia 2024.

Using the 2019–20 ABS Survey of Income and Housing, the wealth Gini coefficient was 0.611, compared with an income Gini of 0.324. A Gini score of 0 means perfect equality, while 1 means all wealth is held by one household.

Australia's wealth Gini is almost double its income Gini, showing that wealth is distributed far less evenly than income. This reflects the way assets such as property, superannuation and investments accumulate over time, while income is spread more broadly through wages and salaries.

0.324

Income Gini

Income inequality is moderate by international standards. Progressive taxation, minimum wage settings and Australia's industrial award system help keep earnings more evenly distributed than in many comparable economies.

0.611

Wealth Gini

Wealth inequality is much higher than income inequality. Assets, especially property, can grow in value over time, allowing wealth to build faster than wages for households that already own them.

Of all new wealth generated in Australia since 2003, approximately 45% has flowed to the top 10% of households. That growth came mainly through rising asset values, especially property, alongside tax settings that provide concessions for some capital gains and investment losses.

Section 03The wealthiest 10%

What net worth puts a household in the top 10% in Australia?

What is the minimum net worth to be in Australia's top 10%?

To be in the wealthiest 10% of Australian households, a household needs net worth of around $2.6 million, or more than four times the latest measured median household net worth of $579,200. The average within the top decile is $5.2 million, which shows how wide the range is. Many households in this group hold considerably more than the entry threshold.

Household wealth by group: net worth thresholds and share of national wealth, 2022–23

Minimum entry threshold, average net worth, and share of total national wealth. The minimum threshold is published for the top 10% only.

Household group

Minimum net worth

Average net worth

Share of national wealth

Top 10% ★

$2,600,000

$5,200,000

44%

Top 20%

N/A

$3,230,000

62.8%

Middle 20%

N/A

$564,500

11.3%

Bottom 20%

N/A

$35,200

0.7%

The minimum net worth threshold is only published for the top 10%. N/A indicates figures not separately stated in the source data.

Source: ACOSS and UNSW Sydney, Inequality in Australia 2024.

Wealth in the top 10% is closely tied to asset ownership, including residential property, investment property, superannuation, shares and business assets. The gap between the group's entry threshold, around $2.6 million, and its average wealth of $5.2 million shows how wide the range is within the top decile.

A smaller number of very high-wealth households pulls the average above what many households in this group hold. The top decile's share of national wealth has grown over the past two decades, driven largely by rising asset values, especially property.

Section 04Property and wealth

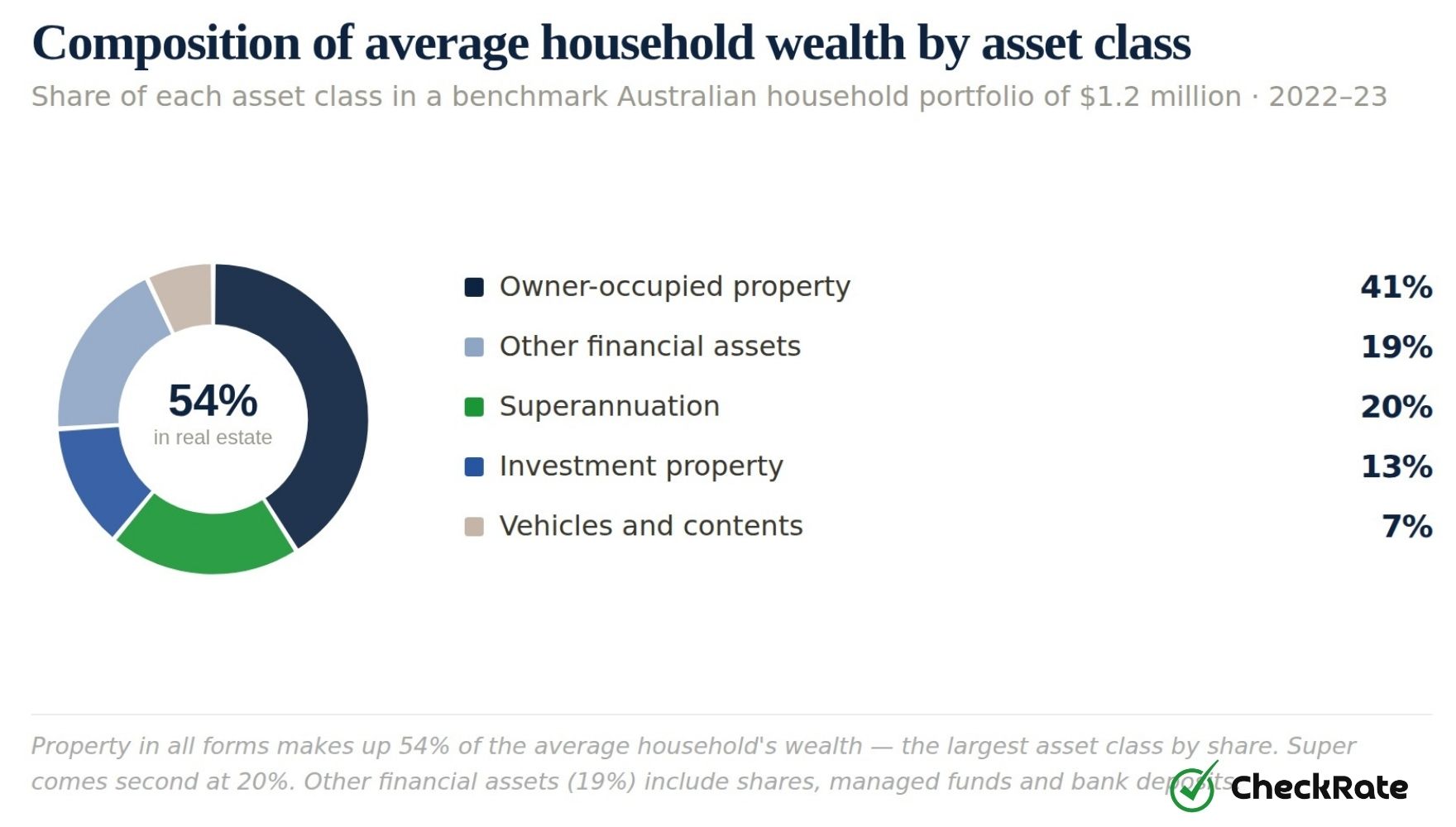

Property makes up more than half of average household wealth

What percentage of Australian household wealth is held in property?

Property accounts for approximately 54% of average household wealth in Australia. The family home makes up about 41%, while investment properties add another 13%. Superannuation is the second-largest asset class, accounting for around 20% of average household wealth.

Owner-occupied

41%

of average household wealth

Equivalent to approximately $492,000 in a $1.2 million portfolio. The largest asset class in the average household wealth mix.

Superannuation

20%

of average household wealth

Approximately $240,000 in a $1.2 million portfolio. The second-largest component reflecting decades of compulsory contributions since 1992.

Investment property

13%

of average household wealth

Approximately $156,000 in a $1.2 million portfolio. Concentrated among higher-net-worth households and older age groups.

Composition of average household wealth by asset class

Share of each asset class in a benchmark Australian household portfolio of $1.2 million. 2022–23 estimates.

Property in all forms makes up 54% of the average household's wealth, the largest asset class by share. Super comes second at 20%. Other financial assets (19%) include shares, managed funds, and bank deposits. The 7% in vehicles and household contents is largely illiquid and loses value over time; it is counted in total wealth but contributes little to long-term financial security.

Source: ACOSS and UNSW Sydney, Inequality in Australia 2024; McKell Institute, Funding Fairer Housing, 2026.

Between 1999 and 2024, Australian house prices rose by approximately 142% in real terms, while wages grew by around 44%. Property prices grew more than three times faster than wages, increasing the value of existing housing assets and widening the gap between house prices and earnings.

142%

house prices

Real house price growth vs wage growth, 1999–2024

Over the same 25 years, wages grew by approximately 44% in real terms, less than a third of the house price gain. For households that bought property during this period, most of the wealth gain came from the rising value of that property, not from their wages.

House prices

+142%

Wages

+44%

Those gains have not been spread evenly. The top 20% of households hold approximately 73% of net land wealth nationally, while the bottom 40% collectively hold negative net land wealth. This means their outstanding mortgage debt is higher than the current land value they own.

Renters have faced different pressures. Real rents have risen by approximately 50% over two decades, without the wealth-building effect that can come from owning property.

Tax settings also shape the divide between asset owners and non-owners. The 50% capital gains tax discount reduces the taxable portion of gains on assets held for more than 12 months. Negative gearing allows investment property losses to be offset against other taxable income when rental costs exceed rental income.

Around 82% of the total financial benefit from the capital gains tax discount flows to the top 10% of taxpayers. More than 2,500 investors hold 10 or more rental properties each, collectively controlling more than 33,000 dwellings.

Section 05Superannuation: balances by age and gender

The superannuation gender gap peaks before retirement

What is the average superannuation balance in Australia by age?

Super balances vary by age and gender. For Australians aged 60 to 64, the average balance was $395,852 for men and $313,360 for women at June 2023. That is a difference of $82,492, or 20.8%. The gender gap starts at less than $1,000 for younger workers and reaches its widest point in the 60 to 64 age group, just before retirement. Both average balances remain below the Association of Superannuation Funds of Australia (ASFA)'s $595,000 benchmark for a comfortable single-person retirement.

Men aged 60–64

$395,852

Average balance, June 2023

Women aged 60–64

$313,360

Average balance, June 2023

Peak gender gap

$82,492

At ages 60–64, 20.8% lower for women

The super gender gap starts small and widens with age. At ages 18 to 24, the difference between male and female average balances is under $1,000. By ages 50 to 54, it has grown to nearly $64,000. It reaches its widest point at ages 60 to 64, at $82,492.

The gap does not close before retirement. It builds over decades as differences in earnings, hours worked, and time out of paid work affect super contributions.

Average superannuation balances by age group and gender

Mean account balances for non-nil accounts, June 2023. The dashed line marks the ASFA comfortable retirement standard ($595,000 for a single person).

MenWomenASFA comfortable standard ($595k)

The gap between male and female balances widens through the 30s to 50s, when career interruptions for caring responsibilities are most common. For women aged 60 to 64, an average balance of $313,360 is $281,640 below the ASFA benchmark. Men's average balance at that age ($395,852) also falls short by approximately $199,000.

Source: ATO Taxation Statistics 2022–23, Superannuation balances by age and gender, June 2023. ASFA Retirement Standard 2025–26.

The gap is shaped by the way the super system is linked to paid work. Super is calculated as a percentage of ordinary time earnings, meaning base wages for standard hours and excluding overtime. Periods of part-time work, unpaid work or time out of the workforce can therefore reduce the amount of super accumulated over time.

Women are more likely to take career breaks for caring responsibilities, work part-time, or be employed in lower-paid industries. Because super builds through regular contributions and investment returns, these differences can compound across a working life.

The super system has historically been built around continuous full-time employment, which does not reflect the working patterns experienced by many women.

ASFA comfortable retirement standard

To retire comfortably as a single person, the current benchmark is approximately $595,000 in super. Women aged 60 to 64 had an average non-nil superannuation balance of $313,360, a shortfall of roughly $281,640.

Recent changes increase the coverage or rate of superannuation contributions for some workers. These include extending Superannuation Guarantee payments to Paid Parental Leave, and removing the former $450 monthly earnings threshold. These changes apply prospectively and do not change balances already accumulated by women approaching retirement.

Women's avg at 60–64: $313,360ASFA target: $595,000

Full data: superannuation balances by age group and gender

Mean and median account balances for non-nil accounts, June 2023. The 60–64 row marks the peak gap between male and female averages.

Age group

Male avg

Male median

Female avg

Female median

Avg gap (M–F)

Under 18

$7,687

$350

$4,699

$220

$2,988

18–24

$9,062

$5,394

$8,163

$4,963

$899

25–29

$27,021

$19,220

$24,821

$19,162

$2,200

30–34

$55,690

$41,268

$46,586

$36,016

$9,104

35–39

$96,122

$74,130

$76,020

$57,566

$20,102

40–44

$140,680

$108,344

$109,209

$79,445

$31,471

45–49

$193,501

$144,272

$147,146

$101,888

$46,355

50–54

$254,071

$177,194

$190,175

$122,150

$63,896

55–59

$319,743

$202,583

$242,945

$140,662

$76,798

60–64 ★

$395,852

$219,773

$313,360

$163,218

$82,492

65–69

$448,518

$217,954

$392,274

$199,006

$56,244

70–74

$501,785

$214,749

$449,540

$215,202

$52,245

75+

$525,627

$185,228

$454,333

$179,928

$71,294

Covers non-nil accounts only (accounts with a balance greater than zero). The gap column shows average male balance minus average female balance. Medians are below averages at all ages, reflecting a skewed distribution with many low-balance accounts.

Source: ATO Taxation Statistics 2022–23, Superannuation balances by age and gender, June 2023.

Section 06Wealth across age groups

Older Australians hold the highest household wealth

How does household net worth vary by age in Australia?

Net worth rises with age. Households aged 65 and over had a median net worth of $1,083,300, compared with $272,000 for those aged 25 to 34 and $78,900 for those under 25. This is a 14-fold difference between the oldest and youngest groups.

Median household net worth by age group

Median net worth by age group, 2019–20. Figures are in nominal dollars (not adjusted for inflation). Values shown at end of each bar.

The median net worth of households aged 65 and over is approximately 14 times that of under-25 households and four times that of 25 to 34-year-olds. The largest increase is between the 55–64 and 65+ cohorts, a difference of $297,900, which broadly reflects households that bought property in the 1980s and 1990s and accumulated several decades of capital growth.

Source: ABS Survey of Income and Housing 2019–20, Table 9.2: Household assets and liabilities by household composition.

Much of older households' wealth is held in mortgage-free property. On average, households aged 65 and over hold approximately $734,000 in fully paid-off net land wealth, built up over decades of property ownership and price growth.

Property is a major driver of the age-based wealth divide. In 1999, the median house price was roughly 4.4 times median income. By 2024, it had risen to approximately 8.6 times. This means the main wealth-building asset of the past 25 years has become harder for younger households to access.

For younger households on average wages in major cities, higher price-to-income ratios indicate greater barriers to entering the property market. Households that remain outside the property market may continue facing rental costs without building housing equity.

Section 07Income versus wealth

Wealth is distributed less evenly than income in Australia

Does earning a high income lead to high net worth in Australia?

Using the 2019–20 ABS Survey of Income and Housing, Australia's wealth Gini was 0.611, compared with an income Gini of 0.324. This means wealth is distributed much less evenly than income. A high-income household without significant assets may have a lower net worth than a lower-income household that bought property years earlier. In Australia, asset ownership, especially property, plays a major role in determining household wealth.

Income inequality in Australia is moderate by international standards. Progressive tax rates, minimum wage settings and the industrial award system help keep earnings more evenly distributed than in many comparable countries.

Why wealth grows differently from income

Wealth inequality works differently. Capital gains on assets held for more than 12 months receive a tax discount, and investment property losses can be offset against other income. Asset values can also compound over time, allowing wealth to grow faster than wages for households that already own property or other investments.

This means two households with similar incomes can end up in very different positions by retirement. A household that bought a home in a major city in 2005 and held it to 2025 may have accumulated substantial capital gains. A household that did not buy property will not have built that housing equity.

Income data on its own gives an incomplete picture. A high earner who rents, recently entered the workforce or carries student debt may have good income but limited wealth. Someone on more modest wages who bought a home earlier may have built substantial wealth despite earning less.

Section 08Interactive explorer

Explore Australian wealth data

Interactive explorer

Explore Australian wealth data

Use the tabs to look up an estimated wealth position, explore superannuation balances by age and gender, or compare net worth across age groups.

Estimated net worth: total assets minus total debts (in dollars)

$

General information only

This article presents publicly available statistical data for general information purposes only. It does not constitute financial, tax, legal, or investment advice. Wealth and income figures reflect population-level data at specific points in time and may not represent individual circumstances. Before making any financial decisions, consider seeking independent professional advice.

McKell Institute: Funding Fairer Housing (2026) — property investor concentration data sourced via ATO FOI disclosure; net land wealth distribution by quintile; real house price, wage and rent growth; price-to-income ratio trends; and household net land wealth by age cohort.